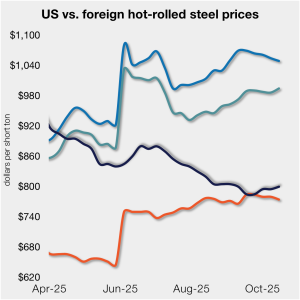

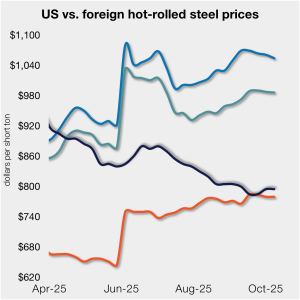

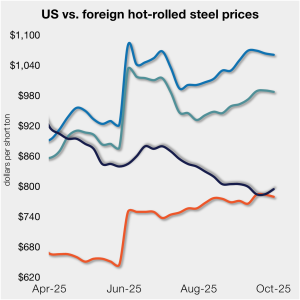

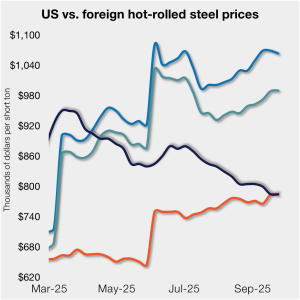

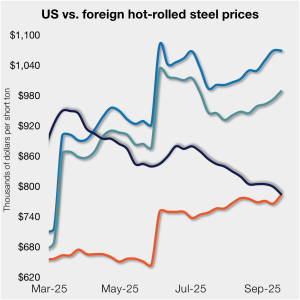

Gap between US HR prices, imports narrows

SMU’s average price for domestic hot-rolled (HR) coil was $800 per short ton (st) this week, up $5/st week on week (w/w). In offshore markets last week, prices were varied.

SMU’s average price for domestic hot-rolled (HR) coil was $800 per short ton (st) this week, up $5/st week on week (w/w). In offshore markets last week, prices were varied.

US scrap prices fell on busheling and shredded in October, while HMS remained flat, market sources told SMU.

Participants in the domestic plate market say spot prices appear to have hit the floor, and they continue to linger there. They say demand for steel remains thin, with plate products no exception.

SMU’s HR price stands at $800/st on average, up $5/st from last week. The modest gain came as the low end of our range firmed, and despite the high end of our range declining slightly.

SMU has successfully completed an external review of all our prices. The review has concluded that they algin with principles set by the International Organization of Securities Commissions (IOSCO).

Nucor has left its consumer spot price for hot-rolled coil at $875 per short ton for the eighth straight week.

Some sources also speculated that plate could see further price increases thanks to modest but steady demand, lower imports, mill maintenance outages, and end markets less immediately affected by tariff-related disruptions.

SMU’s average price for domestic hot-rolled (HR) coil was $795 per short ton (st) this week, sideways week on week (w/w). The move was different in offshore markets last week, as prices eased marginally.

The US hot-rolled coil (HRC) market feels steadier as the 4th quarter begins - not strong, but no longer slipping either.

Most mills sought a drop of $20-40 per gross ton (gt) in busheling prices and a $20/gt dip for shredded and HMS. Despite efforts to buy cheaper, the busheling price settled at down only $20/gt.

SMU’s sheet and plate prices see-sawed this week as hot-rolled (HR) coil prices held their ground while prices for galvanized product slipped.

Nucor is keeping hot-rolled (HR) coil prices unchanged again this week, according to its latest consumer spot price (CSP) notice issued on Monday, Oct. 6

The price gap between stateside hot band and landed offshore product narrowed this week. Still, with the 50% Section 232 tariff, most imports remain much more expensive than domestic material.

Market participants predicted that prices should be at or near a bottom. But while most seemed to agree on that point, many also said they saw little upside given a quiet spot market and ongoing concerns about demand.

Nucor aims to increase prices for steel plate by $60 per short ton with the opening of its November order book.

Nucor is keeping hot-rolled (HR) coil prices unchanged again this week, according to its latest consumer spot price (CSP) notice issued on Monday, Sept. 29.

SSAB Americas sent a price increase notification to customers announcing that transaction prices on all its products are increasing by a minimum of $60 per short ton (st).

Most steelmaking raw material prices held steady or ticked higher over the past month

SMU’s average price for domestic hot-rolled (HR) coil held at $785 per short ton (st) this week, unchanged week on week (w/w). A similar dynamic was seen in offshore markets last week as well.

Sheet and plate prices were flat or lower this week as less discounting from domestic mills was offset by few signs of an anticipated rebound in demand.

A compromise has been reached in the pig iron market, sources told SMU. Recall we reported US buyers were bidding $390 per metric ton (mt) FOB or less while sellers were holding sideways at about $400/mt.

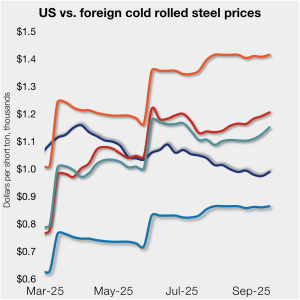

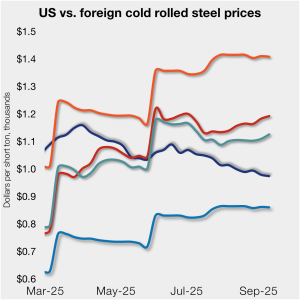

Cold-rolled (CR) coil prices ticked up in the US this week, matching a similar trend seen in offshore markets as well.

Participants in the US carbon and steel plate market are frustrated by the lack of activity following the Labor Day holiday weekend.

With only a modest decline in US prices, HR imports, on a landed basis, remain much more expensive than domestic hot band.

The premium galvanized coil carries over hot-rolled coil (HRC) coil has marginally widened in recent months. As of Sept. 16, the spread between these two products reached a three-month high of $175 per short ton (st), though it is still low by historical standards.

SMU’s price ranges were mixed again this week as the market continues to seek a floor amid industry hopes for a Q4 rebound.

Half of the participants on this month's Air-Conditioning & Refrigeration Distributors International (HARDI) Sheet Metal/Air Handling Council call expect galvanized steel base prices to remain flat at ~$48 per hundredweight ($960/short ton) for the next 30 days.

Nucor held its hot-rolled coil list price flat again this week, according to its Monday, Sept. 15 consumer spot price (CSP) notice.

Cold-rolled (CR) coil prices ticked lower in the US this week, while prices in offshore markets mostly diverged and ticked higher.

The pig iron market in Brazil is currently in flux and there have been few, if any, confirmed cargoes transacted for the US.