Doubled S232 tariff holds US HR prices below EU

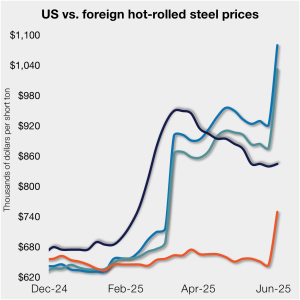

David Schollaert presents this week's analysis of hot-rolled coil prices, foreign vs. domestic.

David Schollaert presents this week's analysis of hot-rolled coil prices, foreign vs. domestic.

Sheet and plate prices were little changed in the shortened week ahead of Independence Day, according to SMU’s latest check of the market.

Will more DRI investment come to the US?

Nucor aims to keep plate prices flat again with the opening of its August order book.

Nucor has raised its weekly spot price on hot-rolled coil by $10 per short ton after holding it steady last week.

After a hot start to June, the CME ferrous derivatives complex has cooled down.

As of June 24, the premium galvanized coil carries over hot-rolled coil is just $5 per short ton (st) above the lowest level recorded in almost two years.

Prices for steel sheet slipped this week despite Section 232 tariffs remaining at 50% and a US strike on nuclear facilities in Iran over the weekend.

The resistance Brazilian pig iron sellers had shown to accepting lower prices has proved short-lived, sources told SMU.

Nucor maintained its weekly list price for hot-rolled (HR) coil this week, following two consecutive increases.

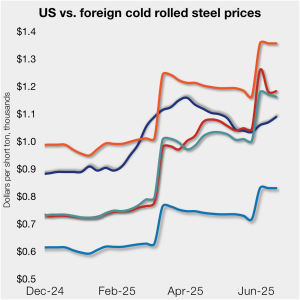

US cold-rolled (CR) coil prices continued to tick higher this week, while offshore markets were mixed.

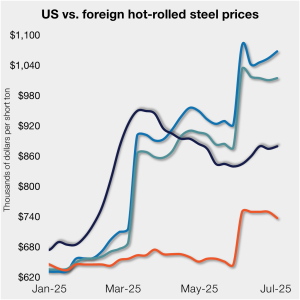

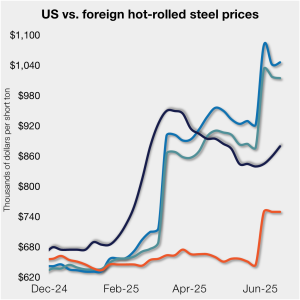

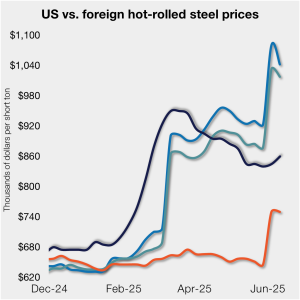

US hot-rolled coil prices crept up again this week but still trail imports from Europe.

Could we see an abrupt shift now that oil prices have spiked higher? Will we see a rebound in the rig count? Will this create a snap-loading effect (think waterski rope), where the industry suddenly does a 180-degree turn? If so, will that bring with it increased demand for steel products used by the energy industry?

Steel prices inched higher again this week across most of the sheet and plate products tracked by SMU.

Cleveland-Cliffs plans to increase prices for hot-rolled (HR) coil to $950 per short ton (st) with the opening of its July spot order book. The Cleveland-based steelmaker said the price hike was effective immediately in a letter to customers dated Monday.

Nucor raised its published weekly spot price for hot-rolled (HR) coil by $10 per short ton (st) on Monday.

US cold-rolled (CR) coil prices edged up again this week, and most offshore markets moved in the opposite direction. But the diverging price moves stateside vs. abroad did little to impact pricing trends. The bigger impact was from Section 232, which were doubled to 50% as of June 3. The higher tariffs have resulted in […]

Subdued demand has continued to weigh on steel sheet prices globally.

Never a dull moment in today's HR futures market.

Domestic hot-rolled (HR) coil prices edged up marginally again this week, while offshore prices ticked down.

The price spread between HRC and prime scrap widened in June.

Steel prices climbed for a second straight week across all five sheet and plate products tracked by SMU.

Brazilian pig iron prices fail to rise after ferrous scrap market settle.

Ferrous scrap prices in the US have remained stable from May to June.

The $20/short ton increase applies to all of the steelmaker’s sheet mills, including West Coast joint-venture subsidiary CSI.

Domestic hot-rolled coil prices edged up marginally this week, while offshore prices ticked down.

The increases are effective June 6.

This CRU Insight examines how the increase in Section 232 tariffs on steel to challenging levels will lead to significatively higher prices for end consumers in the US market.

US manufacturers brace for the implications spurred by the latest round of Section 232 tariffs.

A fierce flat price rally started this week that saw the nearby months rally by over $120/ short tons, exceeding the contract highs seen in February ahead of the first batch of tariffs.