Spread between US HRC and imports tightens marginally

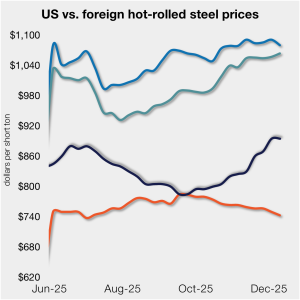

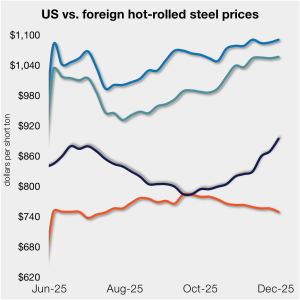

The price gap between stateside hot band and landed offshore product continues to narrow toward parity, now at its lowest level in five months.

The price gap between stateside hot band and landed offshore product continues to narrow toward parity, now at its lowest level in five months.

Nucor has announced new base prices for galvanized steel products as of Wednesday, Dec. 10.

Triple-S Steel Holdings and a European partner have taken a major equity stake in Zimmer Staal, a steel distributor based at the Port of Antwerp in Belgium.

SMU’s sheet and plate prices took a breather this week, holding relatively steady at multi-month highs.

The Dodge Momentum Index (DMI) decreased 1% from October to November. However, it's up 36% year-to-date from the average reading over the same period in 2024, according to the latest data released by Dodge Construction Network.

Domestic raw steel production marginally declined last week, according to the latest data released by the American Iron and Steel Institute (AISI).

The United Steelworkers (USW) Local 1123 union and Metallus have reached a new tentative agreement for a four-year contract.

Worthington Steel is in talks to possibly take over German-based service center chain Klöckner & Co. SE, both companies have confirmed.

Canadian service center Varsteel Ltd. has acquired Victoria Steel (also known as Acier Victoria) of Victoriaville, Quebec.

NEMO Industries CEO Daniel Liss has already made waves with his bold plan to bring pig iron production back to US soil. In an SMU Community Chat on Wednesday, he shifted the conversation from inspiration to execution, laying out timelines, financing strategies, and customer demand that could reshape the steel supply chain by the end of the decade.

The Pennsylvania Commonwealth Court has sided with Wheatland Tube, a Zekelman Industries company, in a landmark trade ruling that bars public agencies and contractors in the state from using Mexican-made steel conduit in state-funded projects.

The American Iron and Steel Institute’s (AISI's) Kevin Dempsey gave a series of policy proposals ahead of the review of the USMCA trade agreement next year.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

The Coalition for a Prosperous America (CPA) is urging the Trump administration to keep Section 232 steel and aluminum measures focused on rebuilding US capacity, rather than using them as bargaining chips in unrelated negotiations.

Nippon Steel hopes to pare down a list of sites by next summer and make a final decision by the end of 2026 for a new U.S. Steel plant in the United States.

NLMK has revised their galvanized and galvanneal coating extras effective January 2026.

Sources expect the recent spot market price hikes on domestically produced plate products to be accepted by the market.

The price gap between stateside hot band and landed offshore product has inched closer to parity, now at its lowest level since the summer.

All of SMU’s sheet price indices rose this week, climbing to new multi-month highs. At the same time, our plate index held steady.

A steelmaker in the Southeast has entered the market for shredded, P&S, and HMS at prices of $20/gt over November.

Economic activity across the US was largely static with some modest activity unfolding at a sluggish pace, according to the US Federal Reserve’s (The Fed) latest Beige Book report.

The volume of raw steel produced by US mills eased last week, according to the latest figures released by the American Iron and Steel Institute (AISI).

Deere & Company's latest earnings report put a spotlight on the mounting costs of tariffs across the agricultural and heavy machinery sectors.

The Chicago Business Barometer tumbled to an 18-month low in November, according to Market News International (MNI) and the Institute for Supply Management (ISM)

Canada’s Algoma Steel announced ~1,000 layoffs on Monday as a result of disruptions from the US tariff situation.

Oregon Steel Mills has joined other producers, announcing a price increase of at least $40 per short ton for steel plate.

The Institute for Supply Management’s (ISM) latest report reflects the dim market conditions reported by US manufacturing executives in November.

ArcelorMittal Dofasco and Stelco are aiming to increase spot market base prices by a minimum of CA$100 per short ton (US$72/st), effective immediately.

Nucor increased its weekly hot-rolled coil spot list price by $5 per short ton (st) on Monday, Dec. 1. This was its sixth increase in as many weeks, moving up $45/st over that span.

Canadian Prime Minister Mark Carney announced new measures on Wednesday to strengthen the country’s domestic steel industry, which include a tariff on some downstream steel-intensive goods.