US steel imports fall through September and October

September steel imports were 10% less than August levels, marking the lowest monthly import rate seen this year

September steel imports were 10% less than August levels, marking the lowest monthly import rate seen this year

Most steel buyers polled in our market poll this week continue to report mills are open to negotiation on new order pricing. In fact, negotiation rates have been strong for the majority of 2024, trending higher since September.

Luxembourg-based Ternium achieved record-high sales volumes in Mexico in the third quarter, reaching key milestones at its Pesqueria industrial center, the largest project in the Latin American steelmaker's history.

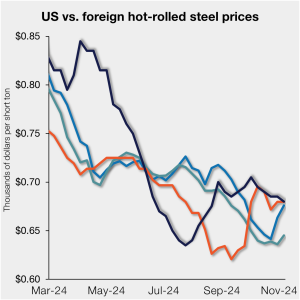

US hot-rolled (HR) coil prices moved lower this past week while tags in offshore markets were largely higher. Domestic tags are again nearly level with imports on a landed basis.

Donald Trump has won the US presidential election. The Republican party has re-taken control of the Senate. Votes are still being counted in many tight congressional races. But based on results so far, the Republicans seem likely to maintain control of the House of Representatives. If confirmed, this will give Trump considerable scope to pass legislation pursuing his agenda. What this means for US policy is not immediately obvious. Trump will not be inaugurated until Jan. 20. In the coming weeks and months, he will begin to assemble his cabinet, which may give a clearer signal on his policy priorities and approaches. Based on statements he made during the presidential campaign, we have set out the likely direction of his economic policy here and green policy here.

Timna Tanners, managing director of equity research for Wolfe Research, will be the featured speaker on the next SMU Community Chat. The webinar will be on Wednesday, Nov. 13, at 11 am ET. It’s free to attend. You can register here. Timna – who has coined Sheet Storm, Scrap Squeeze, and Galv Galore – is one of the most popular guests on our Community Chats. Her insights and forecasts are always thought-provoking.

SMU price indices edged lower this week for all products but one, marking the fifth consecutive week of overall declining prices.

Last week’s Community Chat with international trade attorney and regular SMU columnist Lewis Leibowitz was packed full of valuable perspectives on trade topics near and dear to the steel industry.

The negative impact of high interest rates on consumer behavior, particularly in the automotive and housing sectors, was the primary driver of the demand weakness seen across the third quarter, according to Cleveland-Cliffs executives.

Cleveland-Cliffs swung to a steep loss in the third quarter. However, it touted the recent closing of its acquisition of Stelco in its quarterly earnings report released on Monday and said steel demand should bounce back early next year.

The domestic steel tube industry is applauding a federal appeals court decision upholding a ruling that confirms at least one importer misclassified steel conduit imported into the US.

Timna Tanners, managing director of equity research for Wolfe Research, will be the featured speaker on the next SMU Community Chat. Tanners – who has coined Sheet Storm, Scrap Squeeze, and Galv Galore – is one of the most popular guests on our Community Chats. Her insights and forecasts are always thought provoking.

I joined in a Steel Market Update community chat last week. Predictably, many of the questions concerned the likely results of a Trump or Harris victory in the election. Like most people, I don’t know who will win. But by next week I probably will know. Here is my take, with an emphasis on steel policy. There are a surprising number of similarities between the Democratic and Republican candidates’ positions on steel policy. In part, that is because both candidates are going after the same voters—steel workers, whether unionized or not.

Canada’s Stelco Holdings Inc. is now officially owned by Cleveland-Cliffs Inc.

A spill of liquid steel at a Grupo Simec facility in central Mexico has killed at least 12 workers.

Domestic manufacturing contracted for the seventh straight month in October, according to the latest report from the Institute for Supply Management (ISM). This marks the 23rd time in the last 24 months that it has been in contraction.

US rig activity has been historically weak since June, hovering just above multi-year lows for four months. Canadian counts have ticked lower in recent weeks but remain strong.

A roundup of this week's CRU aluminum news.

The Chicago Business Barometer fell to a five-month low in October and continues to indicate deteriorating business conditions, according to Market News International (MNI) and the Institute for Supply Management (ISM).

Cleveland-Cliffs has received all the required approvals to finalize its $2.5-billion acquisition of Canadian steelmaker Stelco Holdings Inc.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

Primetals Technologies renewed two long-term maintenance service contracts with steel producers in the Americas.

We all know the American news cycle moves pretty fast. Viral today, cached tomorrow. So it is with the US presidential election on Tuesday, Nov. 5. People have election fatigue. They've moved on to other things like planning holiday parties, debating Super Bowl hopefuls, or even starting to look forward to our Tampa Steel Conference in February.

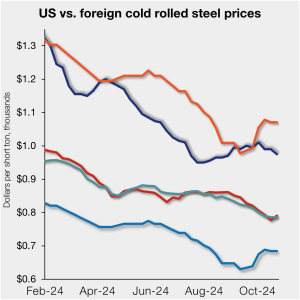

The price spread between US-produced cold-rolled (CR) coil and offshore products was negligibly tighter in the week ended Oct. 25, on a landed basis.

US drill rig activity remains near multi-year lows, hovering within a narrow range over the last five months. Canadian counts have stabilized in recent weeks but remain near some the highest levels recorded in the past seven months.

SMU’s Current Sentiment Index suggests steel buyers are still optimistic about their businesses’ ability to succeed in today’s market, though their confidence has significantly declined compared to recent months.

In this Insight piece, CRU economists explore the possible economic effects of Trump's and Harris' agendas.

Architecture firms continued to experience soft business conditions through September, according to the latest Architecture Billings Index (ABI) release by the American Institute of Architects (AIA) and Deltek.

More than nine out of every 10 steel buyers polled by SMU this week reported that mills are flexible on prices for new orders. Negotiation rates have been strong since April and on the rise since early September.

The construction sector added 25,000 jobs in September, driven by labor shortages and improved wages, according to data released by the US Bureau of Labor Statistics.