Price gap between US CR, most imports narrows

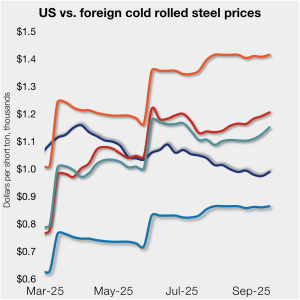

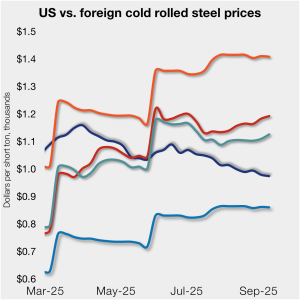

Cold-rolled (CR) coil prices ticked up in the US this week, matching a similar trend seen in offshore markets as well.

Cold-rolled (CR) coil prices ticked up in the US this week, matching a similar trend seen in offshore markets as well.

A recap of the week in steel.

For the next month, CRU forecasts that global demand for steelmaking raw materials will increase month on month (m/m).

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

SMU’s Steel Buyers’ Sentiment Indices diverged this week. The Current Steel Buyers’ Sentiment Index continued its recovery from the five-year low seen one month ago. Meanwhile, Future Buyers’ Sentiment gave back some of the ground gained in recent surveys.

We’ve been talking about a potential inflection point for the past couple of weeks. And the market does appear to be nearing one.

Participants in the US carbon and steel plate market are frustrated by the lack of activity following the Labor Day holiday weekend.

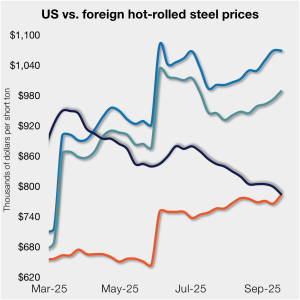

With only a modest decline in US prices, HR imports, on a landed basis, remain much more expensive than domestic hot band.

Sheet times ticked higher but remain within days of multi-year lows, territory they have been in since May. Plate lead times have shifted lower in the past month but remain about a week longer than they were at this time last year.

The American Iron and Steel Institute (AISI) has added Worthington Steel to its membership roster and elected Geoff Gilmore, president and chief executive officer of the steel processor, to its board of directors.

Housing starts slowed in the US in August as affordability challenges and cautious builder sentiment weighed on new construction activity.

Sheet and plate buyers say mills remain open to negotiating spot prices this week, though less so than in recent weeks, according to SMU’s latest market survey.

The premium galvanized coil carries over hot-rolled coil (HRC) coil has marginally widened in recent months. As of Sept. 16, the spread between these two products reached a three-month high of $175 per short ton (st), though it is still low by historical standards.

US service centers flat-rolled steel supply in August declined month-over-month (m/m) and year-over-year (y/y), according to SMU data.

SMU uses ferrous scrap survey data to take AI out on a test drive.

SMU’s price ranges were mixed again this week as the market continues to seek a floor amid industry hopes for a Q4 rebound.

Half of the participants on this month's Air-Conditioning & Refrigeration Distributors International (HARDI) Sheet Metal/Air Handling Council call expect galvanized steel base prices to remain flat at ~$48 per hundredweight ($960/short ton) for the next 30 days.

Geneva-based global commodities trader Mercuria is set to acquire a majority stake in Tata International, according to a report in India's Economic Times.

Domestic mill output declined last week, according to the latest data released by the American Iron and Steel Institute (AISI). While down, production remains historically strong, holding near multi-year highs since June.

Nucor held its hot-rolled coil list price flat again this week, according to its Monday, Sept. 15 consumer spot price (CSP) notice.

Will a US-UK meeting next week prove a harbinger of tariff deals to come, or will it be just another case of having the rug pulled from under us?

Cold-rolled (CR) coil prices ticked lower in the US this week, while prices in offshore markets mostly diverged and ticked higher.

Glenfarne Alaska LNG and POSCO signed a preliminary strategic agreement during the GasTech Conference in Milan on Thursday.

The pig iron market in Brazil is currently in flux and there have been few, if any, confirmed cargoes transacted for the US.

A recap of this week's steel industry news...

U.S. Steel has revised its Galvalume coating extras higher effective Nov. 2, 2025. The steelmaker released new extras to customers on Friday, Sept. 12.

Apparent supply totaled 8.88 million short tons (st) in July, down 38,000 st from June and 6% higher than the same month last year

Sheet prices are expected to increase in the coming weeks in most markets. However, rising domestic capacity in the US, subdued demand in Europe, and high inventory levels in China and India will limit price near-term uptrend.

Active rig counts increased in both the US and Canada last week, according to figures released by Baker Hughes. Although rising, US counts continue to hover just above historic lows. Canadian figures remain comparatively healthy, rising to a six-month high this week. Total US rig counts climbed by two week over week (w/w) to 539. […]

When will we see prime scrap become scarce as the worldwide transition to EAF melting increases, especially for HRC production? It's a question I've been asked a lot.