Final Thoughts

While decarbonization has fallen out of the headlines a bit, that doesn't mean it's gone away. Tariffs, geopolitical instability, outright war... there has been a lot to write about in the last year.

While decarbonization has fallen out of the headlines a bit, that doesn't mean it's gone away. Tariffs, geopolitical instability, outright war... there has been a lot to write about in the last year.

Heating and cooling equipment shipments declined in January to the second-lowest rate recorded over the past nine years.

The weather is still influencing the recycled metals market as we head into spring, sources say.

US steel exports jumped 33% in January but remain historically low, according to recently released US Department of Commerce data.

The US steel market is already characterized by high prices and tight supplies, and I wouldn't be surprised if prices move higher and supplies get even tighter – at least in the short term.

SA Recycling's CEO George Adams couldn't be more upbeat about American industry.

Steel imports remained close to multi-year lows in January and February, according to US Commerce Department data released this week.

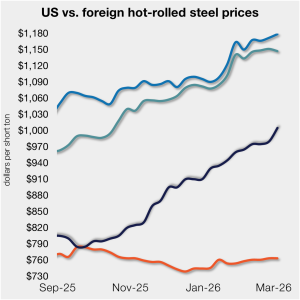

This week sources said spot prices on hot-rolled coils increased modestly.

The latest tally of active oil and gas rigs increased in the US this week but declined in Canada, according to figures recently released from Baker Hughes.

It's been just two weeks since the US and Israel launched a joint attack on Iran. And markets are still in flux as we wade through conflicting messages from the administration on what the goals are when it could be over.

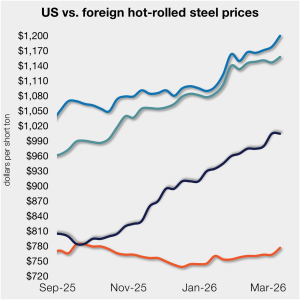

The price gap between US hot-rolled coil (HR) and landed offshore product widened this week, as stateside tags were little changed.

Domestic plate market participants expressed confidence in the overall improvement of market conditions this week.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

The pig iron market in the Brazil-to-US trade flow is showing strength as supply concerns and increased logistical costs impact recent sales negotiations.

The spread between domestic hot-rolled coil and prime scrap prices widened in March, marking a six-month trend.

Sometimes it feels like current events are like a fireworks show that got set off all at once by mistake. In all the commotion, it's hard to know where to look... or where to run.

SMU's sheet and plate prices were flat or higher this week in a US market that remains characterized by extended lead times and limited spot availability.

Raw production has trended upwards since the start of the year, reaching a four-year high in February.

Prices are moving up and lead times moving. And most people expect them to continue to do so for a little while longer, according to our latest survey results. But there is one big wildcard: the Iran war.

Plate sources say they’re welcoming imports as domestic mill delivery delays, extended lead times, and climbing prices make fully adopting US-produced plate products unrealistic.

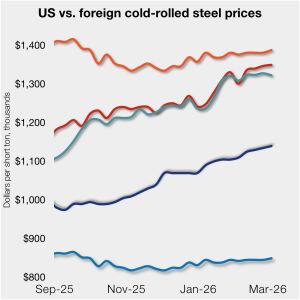

Cold-rolled (CR) coil prices ticked up in the US this week, matching a similar trend seen in most offshore markets as well.

Market participant comments from this month's SMU Ferrous Scrap Survey.

Oregon Steel Mills and SSAB Americas announced higher plate prices to close out the week.

SMU’s Current Sentiment Index for scrap inched up in March, according to the latest data from our ferrous scrap survey. Meanwhile, the Future Sentiment Index remained locked at the same level for the fourth consecutive month.

Steel buyers remain optimistic for their current and future business prospects, though not as strong as they did one year ago.

SMU’s March ferrous scrap market survey results are now available on our website to all premium members.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

Following extensions in February, steel mill lead times held steady or extended further for both sheet and plate products this week, according to buyers responding to our latest market survey.

Broadly speaking, there should be enough scrap to go around. The question we should consider more urgently: Do regional dislocations - whether caused by tariffs, carbon regulations, weather, or conflict - allow scrap to go where mills need it most at a price they can afford?

The price gap between US hot-rolled coil (HR) and landed offshore product tightened this week, as stateside tags continue to rise.