SMU Price Ranges: Sheet, plate slip as lift from S232 ebbs

Sheet and plate prices slipped this week on so-so demand, sideways scrap prices, and chatter that certain mills were making unsolicited calls looking for tons.

Sheet and plate prices slipped this week on so-so demand, sideways scrap prices, and chatter that certain mills were making unsolicited calls looking for tons.

Following one of the lowest levels seen in more than two years, US steel imports rebounded from April to May. However, trade remains low relative to recent years. Preliminary license data suggests another fall in June.

The US ferrous scrap market settled sideways in July.

Industry veteran and longtime steel advocate Thomas A. Danjczek announced he will “finally fully retire” as senior advisor of Headwall Partners.

CRU analysts Thais Terzian and Frank Nikolic will be the featured guests on the next SMU Community Chat on Wednesday, July 9, at 11 am ET.

Domestic steel mill output inched higher last week, according to the American Iron and Steel Institute (AISI). Raw production remains historically strong and has been growing steadily since April.

I’m not sure how many different ways I can write that it’s been a quiet market ahead of Independence Day. There are variations on that theme. I’ve heard everything from the ominous “eerily quiet” to "getting better" and even the occasional “blissfully unaware” (because I’m enjoying my vacation).

It will be a shorter week as the United States celebrates Independence Day on Friday. But we won’t leave you high and dry.

US mills shipped slightly less steel in May than in April, according to the latest figures from the American Iron and Steel Institute (AISI).

The United Steelworkers (USW) labor union celebrated recent news of the signed agreement between Atlas Holdings and Evraz NA in which the Connecticut-based private equity company said it plans to acquire North America’s Evraz facilities.

The rig count declined for the 10th consecutive week in the US, while Canadian count rose for the fifth straight week, according to Baker Hughes.

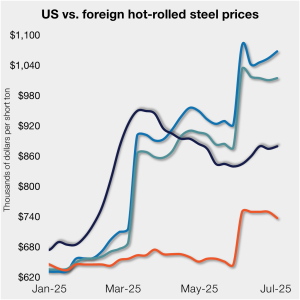

David Schollaert presents this week's analysis of hot-rolled coil prices, foreign vs. domestic.

Steel buyers this week are lamenting weak demand, cautious buying, and So. Much. Uncertainty. I'm no doctor, but I suggest a dual diagnosis of extreme tariff fatigue and early-onset summer doldrums.

Steel sheet buyers report feeling bogged down by the ongoing stresses of stagnant demand, news fatigue, tariff negotiations or implementation timelines, and persistent macroeconomic uncertainty.

A look at SMU data for the month of June.

What's going to be the next big thing in steel?

Sheet and plate prices were little changed in the shortened week ahead of Independence Day, according to SMU’s latest check of the market.

The Steel Manufacturers Association and the American Iron and Steel Institute applauded the tax provisions included in the Senate's tax and budget reconciliation bill.

The owner of Liberty Steel and his family were among the six victims of a plane crash in Ohio on Sunday, according to local media reports.

Will more DRI investment come to the US?

Nucor aims to keep plate prices flat again with the opening of its August order book.

Nucor has raised its weekly spot price on hot-rolled coil by $10 per short ton after holding it steady last week.

Based on the amount of ‘out of office’ replies we’ve been receiving and the results of this week’s steel buyers’ survey, those pesky summer doldrums have arrived for the steel industry.

CRU analysts Thais Terzian and Frank Nikolic will be the featured guests on the next SMU Community Chat on Wednesday, July 9, at 11 am ET. The live webinar is free for anyone to attend. A recording will be available to SMU subscribers.

A roundup of trade news, what's up with Brazilian pig iron, SMU's latest survey results and more to keep you up to date.

Oil and gas drilling activity declined for the ninth-consecutive week in the US, while Canadian counts rose for the fourth straight week, according to Baker Hughes.

Both of SMU’s Steel Buyers’ Sentiment Indices edged higher this week. Current Sentiment rebounded from a near five-year low, while Future Sentiment rose to a two-month high

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

Maybe some of this uncertainty will get ironed out ahead of Liberation Day tariffs resetting higher rates on July 9. But if I had to place a wager, it would be on more drama and last-minute brinksmanship - whether it comes to the Liberation Day tariffs or the various Section 232s that are in the works.

Following the uptick seen two weeks ago, lead times eased this week for all four sheet products tracked by SMU, while plate lead times held steady, according to this week’s market survey.