SMU Survey: Buyers continue to report mills holding firm on price

Most steel buyers responding to our market survey this week said domestic mills remain unwilling to negotiate lower prices for new spot orders.

Most steel buyers responding to our market survey this week said domestic mills remain unwilling to negotiate lower prices for new spot orders.

The US domestic ferrous scrap buying for March shipment is wrapping up this week, with many sources reporting a sideways outcome.

Let’s say the going price for HR is around $1,000/st. Want to place a 1,000-ton spot order at that price? Good luck. It probably won’t be easy.

SMU's sheet and plate prices increased this week to new multi-month highs.

Grupo Acerero SA de CV (GASA) reported increasing shipments at the end of 2025 as the steel producer ramps up a new slab mill in north-central Mexico.

Domestic raw steel production has strengthened since the start of the year and reached a four-year high in mid-February.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $1,005 per short ton (st), up $15/st from last week.

I grew up in Belo Horizonte, the capital of Minas Gerais in southeastern Brazil, surrounded by the Serra do Curral mountains, and a culture steeped in mining and vast iron ore reserves.

Tariff-related litigation in the US and around the world reflects the willingness of the president to act without consulting Congress or our trading partners. We're seeing the impulse to act without congressional approval in international relations too.

Sources in the domestic hot- and cold-rolled coil market said they are beginning to feel prices creeping up this week.

December supply increased 7% from November to the third-lowest monthly rate of the year.

The US scrap market is looking to emerge from a bad winter that has affected both inbound and outbound flows of material since December.

Graphite electrodes are critical to electric-arc furnace steelmaking and the production of other non-ferrous metals.

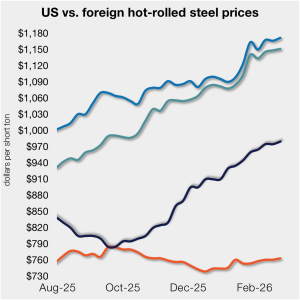

The price gap between US hot-rolled coil (HR/HRC) and landed offshore product remained largely flat again this week, as price movements stateside and abroad mirrored each other.

Plate industry sources said the market has been characterized by three factors lately: fewer domestic mills willing to fulfill spot buys, inconsistent lead times, and erratic demand.

U.S. Steel marked its 125th anniversary yesterday. When you look at the massive changes that have occurred in the country over that time, perhaps it puts the current unpredictability in the steel industry into perspective.

SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

Trade for many of the sheet and plate products we follow has fallen to multi-year lows through December.

The total amount of raw steel produced around the world recovered 5.5% from December to an estimated 147.3 million metric tons in January, according worldsteel.

US hot-rolled coil prices are set to rise year on year in 2026, but the market will face heightened volatility as import flows recover and new domestic capacity comes online, CRU Research Principal Josh Spoores said at this year's Tampa Steel Conference.

SMU has confirmed the US sale of 55,000 metric tons (mt) of pig iron at a price of $440/mt FOB South Brazil, according to an executive in the Brazilian trade.

With domestic steel prices rising steadily and mill lead times pushing out, import offers are becoming more attractive to US buyers.

Total construction starts edged up 0.7% in January to an annualized rate of $1.24 trillion, according to Dodge Construction Network.

Even folks who had been firmly in what I’ll call the “February peak” camp now seem to agree that sheet and plate prices could move higher for longer than they anticipated.

Sheet prices continue to grind higher on tight supply and 'okay' demand. Plate finally saw some movement after weeks of stability as price increases begin to stick.

Steel imports slowed further in December and January to some of the lowest volumes recorded in recent years.

Leaders of the Steel Manufacturers Association (SMA) and the Canadian Steel Producers Association (CSPA) used this year's Tampa Steel Conference to outline the North American steel industry's central challenges: growing pressures, tariff realignments, and the upcoming USMCA review.

The main discussions surrounding pig iron is the ruling by the US Supreme Courts that “reciprocal tariffs” are illegal.

SMU’s Steel Demand Index slipped from earlier in the month, but remains above expansion territory, according to late-February indicators.

North American auto assemblies recovered in January, up nearly 12% vs. December, though down more than 2% year on year (y/y), according to GlobalData.