BlueScope receives $8.8BN takeover bid from SDI and SGH

Australia's BlueScope Steel confirmed it has received a takeover bid from a two-party international consortium that includes Fort Wayne, Ind.-based Steel Dynamics Inc. (SDI).

Australia's BlueScope Steel confirmed it has received a takeover bid from a two-party international consortium that includes Fort Wayne, Ind.-based Steel Dynamics Inc. (SDI).

The Mississauga, Ontario-based metals distributor is now the owner of Kloeckner's facilities in Dubuque, Iowa; Charlotte, N.C.; Suwanee, Ga.; Houston; Austin, Texas; Jacksonville, Fla.; and Pompano Beach, Fla.

Demand for heavy steel plate used in offshore wind farms faces renewed uncertainty after President Trump paused leases for five offshore wind projects.

Members of the United Steelworkers (USW) Local 1123 labor union voted against ratifying a second proposed deal with Metallus on Dec. 18.

The number of oil and gas rigs operating in the US ticked higher this week, while Canadian activity tumbled, according to the latest data released from Baker Hughes.

Nucor Plate Group notified customers it was aiming to increase all plate product prices by $40 per short ton (st).

Domestic raw steel production edged lower last week, according to the latest data released by the American Iron and Steel Institute (AISI).

U.S. Steel’s board of directors has approved the funding for the full $350-million Gary Works blast furnace (BF) reline project.

SMA's Philip Bell looks back at 2025 and ahead to next year.

The US Department of Commerce has officially published the anti-dumping and countervailing duty orders on corrosion-resistant steel sheet imports, the final step in the trade case originally filed more than a year ago. At the same time, Commerce also revealed it is allowing some CORE imports into the country without paying the AD or CVDs.

Metalforming manufacturers are more upbeat on the prospect of improved near-term economic activity despite lower shipping levels in December, according to the Precision Metalforming Association’s (PMA) December report.

Nucor raised its weekly hot-rolled coil spot list price by $10 per short ton (st) this week, marking the company's ninth consecutive increase.

The US and Canadian rig counts both fell this week, according to the latest Baker Hughes data released on Friday, Dec. 19.

An SMU Community Chat with Timna Tanners.

US Midwest sheet prices continued to rise alongside continued mill prices increases as lead times remained extended.

Canadian Prime Minister Mark Carney said the US probably won't reduce tariffs on steel, aluminum, and other goods from Canada anytime soon.

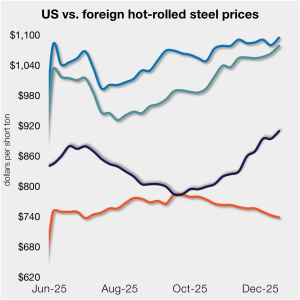

The price gap between stateside hot band and landed offshore product continues to narrow, inching closer toward parity. The premium is now, on average, at its lowest level since July.

Worthington Steel executives emphasized on an earnings conference call on Thursday that the company’s standout fiscal Q2 performance came from capturing new automotive business, with direct automotive shipments rising 26% year over year.

Architecture firms across the United States continued to grapple with weak billings in November, amid uncertain economic conditions, according to the AIA.

Steel Dynamics Inc. expects its fourth-quarter earnings to be weaker than in the previous quarter, albeit still higher than last year. Longer-than-expected mill outages impacted flat-rolled steel volumes in the quarter.

Posco has confirmed a 20% stake in a joint EAF mill in Louisiana with fellow South Korean firm Hyundai, an investment valued at $582 million.

Nucor has guided to lower earnings sequentially in the fourth quarter but higher on-year.

Apparent steel supply rose to 8.64 million short tons in September, driven primarily by higher domestic mill shipments despite a sharp drop in finished imports.

In this Premium analysis we examine North American oil and natural gas prices, drill rig activity, and crude oil stock levels through December

Following last week’s pause, SMU’s price indices were overall steady to higher this week, holding at or near multi-month highs.

Martin Baker is joining Hybar as its strategic metallics manager, responsible for further developing the metallics procurement and global strategic initiatives for the Osceola, Ark.-based steelmaker.

US shipments of heating and cooling equipment fell 11% in October from September to the lowest monthly rate of the year, and an eight-year low, according to AHRI.

SMU and AMU are pleased to announce that Wells Fargo Managing Director Timna Tanners will be joining us for a Community Chat webinar on Wednesday, Dec. 17, at 11 am ET.

Following August’s modest 4% uptick, the volume of steel shipped outside of the country slipped 8% in September to 594,000 short tons, according to recently released data from the US Department of Commerce.

SSAB has tapped Tom Cox to lead its Americas division. Currently GM of SSAB Iowa, he'll assume the position of Head of SSAB Americas as of Feb. 1, 2026.