Beige Book: Most districts report flat economic activity

Economic activity across the US was largely static with some modest activity unfolding at a sluggish pace, according to the US Federal Reserve’s (The Fed) latest Beige Book report.

Economic activity across the US was largely static with some modest activity unfolding at a sluggish pace, according to the US Federal Reserve’s (The Fed) latest Beige Book report.

The volume of raw steel produced by US mills eased last week, according to the latest figures released by the American Iron and Steel Institute (AISI).

Deere & Company's latest earnings report put a spotlight on the mounting costs of tariffs across the agricultural and heavy machinery sectors.

The Chicago Business Barometer tumbled to an 18-month low in November, according to Market News International (MNI) and the Institute for Supply Management (ISM)

Oregon Steel Mills has joined other producers, announcing a price increase of at least $40 per short ton for steel plate.

The Institute for Supply Management’s (ISM) latest report reflects the dim market conditions reported by US manufacturing executives in November.

Nucor increased its weekly hot-rolled coil spot list price by $5 per short ton (st) on Monday, Dec. 1. This was its sixth increase in as many weeks, moving up $45/st over that span.

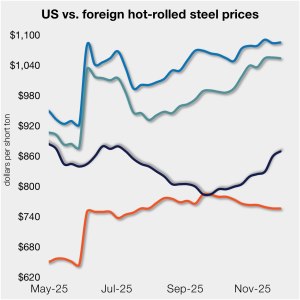

The price gap between stateside hot band and landed offshore product tightened further this week, as the average price for domestic hot-rolled was $10/st higher w/w.

US and Canadian rig counts both declined this week, according to the latest Baker Hughes data released on Wednesday, Nov. 26.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

Steel mill lead times extended this week on all sheet and plate products tracked, according to responses from SMU’s latest market survey.

All five of SMU’s sheet and plate price indices increased this week for the second week in a row, with all products inching up to new multi-month highs. Prices are now up by $30-70/st compared to those seen four weeks ago.

US steel imports declined considerably in September and October, with trade falling to reduced levels not seen in nearly five years.

Republic Steel’s shuttered facilities in Lorain, Ohio, could find new life as international steelmakers, citing US tariffs, explore restarting operations there.

German Economy Minister Katherina Reiche expressed frustration with US levies on steel and aluminum products. The US contends the EU is unfairly targeting its big tech firms.

SSAB Americas aims to increase prices on all its products by at least $40 per short ton (st).

Nucor plans to increase prices for steel plate by $30 per short ton (st). The move coincides with Charlotte, N.C.-based steelmaker opening its plate orderbook for January.

Domestic steel production improved last week, according to the latest figures from the American Iron and Steel Institute (AISI).

Toyota says its $912‑million investment in the US will boost production capacity for hybrids and introduce hybrid‑electric Corollas.

General Motors (GM) is planning a ~$250 million investment to upgrade its Parma Metal Center. The outlay is part of GM's plans to invest ~$4 billion in its US-based manufacturing operations over the next two years. Its 2025 reshoring commitments currently total over $5 billion.

Nucor increased its weekly hot-rolled coil spot list price by $5 per short ton (st) on Monday, Nov. 24. This was its fifth increase in as many weeks.

Wiley attorneys Alan Price and Ted Brackmeyer argue that significant changes to the USMCA and continued Section 232 tariffs on Canada and Mexico are needed to support American steelmaking.

Across BlueScope as a whole, it was the North Star operations in Delta, Ohio, that shone brightest in the Australian company's first-half fiscal 2026 trading update.

Sources say domestic mill lead times and consumer spot prices have increased this week.

Most steelmaking raw material prices remained stable over the past month. Prices are mixed in comparison to this time last year.

Domestic plate market participants anticipate strong economic growth in the first quarter of 2026, which they say is the perfect reason for spot market price hikes now.

Steel market chatter from our most recent survey.

SMU sits down with Barry Zekelman to talk North American trade and the state of the US and Canadian steel industries.

Architecture firms reported a modest improvement in billings in October, though business conditions remained soft, according to the latest ABI report.

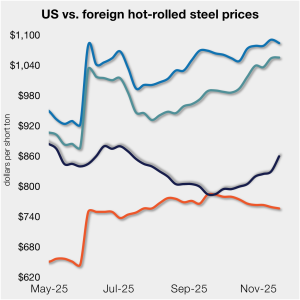

The price gap between stateside hot band and landed offshore product shrank week over week (w/w).