Prices

August 20, 2017

Steel Service Center Inventories Impact on Steel Prices

Written by John Packard

During the week of Aug. 14, 2017, the U.S. steel mills advised their flat rolled and steel plate customers of their intention to increase spot prices on hot rolled, cold rolled, galvanized and Galvalume steels, as well as plate. The flat rolled mills announced $30 per ton base price increases on new spot business. For plate, we saw Nucor take prices up by $30 per ton, while SSAB advised their prices would rise by $40 per ton.

Steel prices had been flat to trending lower leading up to these price increase announcements. The mills are using the increase in commodity prices, especially scrap which rose $10 to $30 per gross ton for August delivery, as the justification of higher prices.

The steel mills have also been pointing at low inventory levels at their flat rolled customers, especially service centers, as a reason to increase prices. The main distributor association is the Metals Service Center Institute (MSCI), and they have been reporting low inventories for many months. Recently, the MSCI announced carbon flat rolled service centers were carrying 2.3 months’ supply as of the end of July. Prior to July, the MSCI was reporting distributors at only 1.9 months of inventory on hand as of the end of May and June 2017.

Steel inventory levels are a key component when considering if price increases will be able to be collected or what may happen with prices looking out into the future.

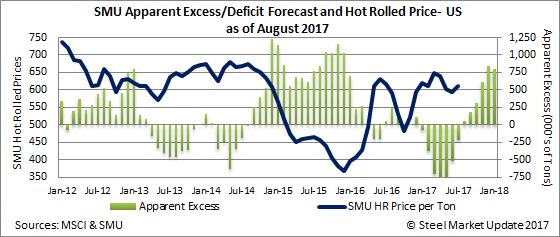

Steel Market Update (SMU) has a proprietary model where we take the MSCI numbers and through our analysis identify whether the distributors are over inventoried (excess) or under inventoried (deficit). Looking back at May and June, our model told us the service centers were 800,000 tons and 525,000 tons short from being in a balanced inventory situation (inventory deficit).

One of our services to our Premium clients is to forecast where we see shipments and inventories and how that will affect where we see distributor inventories as they relate to being balanced at the end of each month. Our forecast is based on historical rates of change from month to month.

Here is what we reported to our Premium subscribers regarding where we saw flat rolled inventories as of the end of July based on our analysis of the MSCI data:

The Steel Market Update (SMU) Service Center Inventories Apparent Excess/Deficit forecast provided in early July for end of July showed that the deficit in inventories being held by flat rolled distributors would be significantly reduced. We have worked with the MSCI carbon flat rolled shipment and inventory data just released for July and our model indicates the deficit did indeed shrink and is very close to our forecast of -232,000 tons.

The MSCI reported carbon flat rolled shipments at 1,991,000 tons. This is 20,000 tons more than our early July forecast of 1,971,000 tons.

Inventories at the U.S. flat rolled service centers ended the month of July at 4,646,000 tons, which was slightly higher than our forecast of 4,589,000 tons.

Using our model, we show the distributors as having shrunk the inventory deficit from -525,000 tons down to -218,000 tons.

August 2017 Distributor Shipments/Inventories Forecast

Steel Market Update is forecasting flat rolled shipments out of the U.S. service centers to be 2,352,000 tons for the month of August. Our forecast is based on the average monthly change for August over the past four years. In this case, the average change was +2.7 percent.

We are also forecasting that the flat rolled steel distributors will hold 4,862,000 tons of inventory at the end of the month.

If our shipment and inventory forecasts are correct, the service centers will have eliminated their inventory deficit for the first time this calendar year and will be in a “balanced” position with +50,000 tons.

As we take our forecast out into the future using the same formula, we expect September through January to see a jump in inventories and, in the process, a jump in the amount of excess steel that will be on the distributors floors every month through January.

If the MSCI data is correct and if our model is anywhere near accurate, the inventories at steel distributors will be rising through the end of the year. As the inventories grow, the pressure will also grow for steel prices to weaken. This can be seen in the historical Apparent Excess/Deficit graphic provided. As inventories decline, steel prices trend higher. When the green bars are indicating an excess (bars are above the zero line), prices tend to drop. The growth in the green bars above zero in the months after July is what our forecast is suggesting will happen.

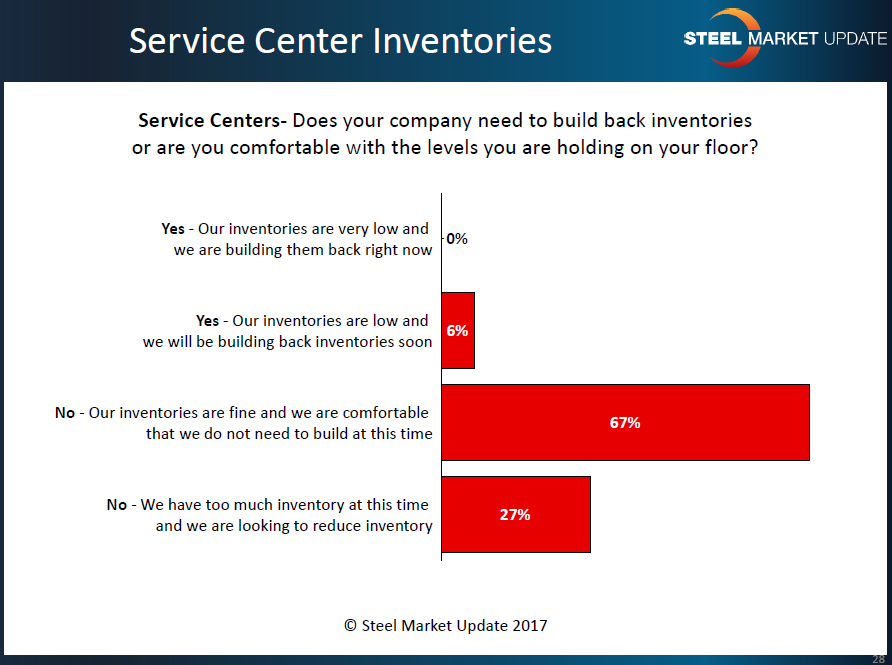

Complementing the data pulled from our MSCI analysis/model are the results we have been gathering during the twice monthly surveys we conduct throughout the year. One of the areas of questioning posed to service centers is if their inventory levels are balanced or if they need to either build or lower inventory levels.

In the survey conducted during the week of Aug. 14, service centers were reporting inventories that were balanced or higher than what they considered comfortable. Only 6 percent of our distributor respondents reported inventories as being too low or in need of replenishment.

So, our data is suggesting that the price increases being announced in mid-August are going to be hard-pressed to be collected.

There is a possible “Black Swan” event that could change inventory flows dramatically and play with our model. That would be the flow of foreign steel. Due to threats of the Section 232 investigation, the amount of foreign steel being imported has increased as buyers look to beat any punitive action by the Trump administration.

There is a question as to whether flows will drop dramatically in September, October and November of this year. During our survey process, trading companies were unanimous in their opinion that imports of cold rolled, galvanized and Galvalume steels will slow in the coming months.

Steel buyers need to remain vigilant to any changes in flows of steel, both domestically and internationally, as interruptions in the norm can have a dramatic impact on steel prices going forward.