Plate

July 18, 2019

CRU: U.S. Plate Prices Play Catchup to the Downtrend in Other Steel Markets

Written by Tim Triplett

By CRU Principal Analyst Josh Spoores and CRU North America Analyst Ryan McKinley

U.S. domestic scrap prices fell by $10 /l.ton m/m in the Great Lakes and Ohio Valley for most grades prior to the Independence Day holiday, but dealers the following week pushed back on the price decline, with some successfully securing little to no change in prices. On the supply side, inbound flows have fallen off by 20 percent or more in many areas, and this has led to some larger dealers resisting the $10 /l.ton price decrease, particularly after mills in the South accepted unchanged prices.

The past several weeks have shown notable volatility and primarily declines in finished steel prices. HR coil prices have fallen by as much as 22 percent, or $145 /s.ton, after the U.S. lifted Section 232 tariffs on Canada and Mexico in mid-May, reaching a recent low of $505 /s.ton in late-June and early-July. This is the lowest price assessed since November 2016. Long product prices declined by roughly 4 percent on average m/m, while scrap prices fell by an average of 3 percent m/m.

Attempting to halt the price decline, Nucor raised flat-roll prices by $40 /s.ton at the end of June and again just last week. These increases come after two weeks of heavy volume trading, which drove CRU’s index prices lower. CRU’s July 10 price assessment showed an end to this falling trend with prices rising even as overall volume has fallen to levels well below the prior two weeks. This is expected as mills will often fill order books at low prices in order to announce a price increase and wait out the market. While transaction volume has fallen back towards more normalized levels, it continues to remain significant and our latest price assessment has HR coil up by $20 /s.ton w/w to $548 /s.ton.

In the long products market, U.S. buyers largely stayed away from purchasing material in June amid relatively high inventory levels, leading to yet more downward pressure on prices. This demand-side weakness led prices to drop for the third month in a row for most long product categories, and prices are now at their lowest levels since Section 232 tariffs were implemented. Import prices have proven uncompetitive, too, which has driven a relatively large m/m decline in import levels. Inventory levels are still relatively high and will likely take more than a month to work through. As a result, even with prices returning to pre-Section 232 levels, it is unlikely that buyers are going to buy large amounts of material in the very near term.

As for the plate market, the declining price trend has led to rapidly lower prices. Indeed, plate prices fell $91 /s.ton since the June 19 assessment and at $724 /s.ton, they are at their lowest level since January 2018. More importantly, at this price, they are $176 /s.ton higher than HR coil, the lowest spread seen since last November. While plate prices are $260 /s.ton lower today from highs reached this past January, these prices are now more in line with flat rolled sheet. Based on the latest service center inventory data collected by Steel Market Update and CRU, plate inventories have remained stable in June, yet they are not being replenished and a shortfall may be coming. With the sheet price hike gaining traction and the expectation that scrap prices have reached a bottom, it should not be unexpected for a plate price hike to soon emerge.

Outlook: Price Hikes May Signal Bottom

U.S. domestic scrap prices have likely bottomed for the time being, and prices appear poised to increase m/m in August. The spike in iron ore prices should help keep pig iron prices elevated, and a 60-day outage at Nucor’s DRI plant in Louisiana will both be tailwinds for prime prices.

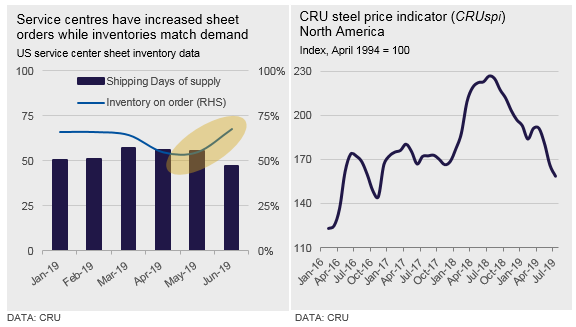

While the need for a later-summer inventory build may now be somewhat diminished for sheet products (see chart), domestic supply is lower due to U.S. Steel’s production cuts. However, we do expect this to allow producers in Canada and Mexico to regain some market share as they are now able to export without S232 tariffs. Demand, meanwhile, may not provide as much support as we previously expected. Industrial growth is slowing or in some cases has been neutral at best. Indeed, the latest manufacturing PMI report for June shows new orders, imports and new export orders all at a neutral level. Some of this weakness is due to the business cycle slowing, yet more blame is being placed on non-steel tariffs. Regardless, industrial economic activity in 2019 H2 does not appear to be supportive of a sustained up-cycle for steel prices.

Latent construction demand may still drive long product price increases in late summer and into fall as companies look to make up for time lost on projects due to adverse weather conditions earlier this year. As such, we expect downward price pressure to dissipate moving into August and September.