Prices

December 12, 2019

CRU: Seasonal Supply Constraints and Firm Demand Lift Prices

Written by Ryan McKinley

By CRU North America Senior Analyst Ryan McKinley, from CRU’s Steel Metallics Monitor

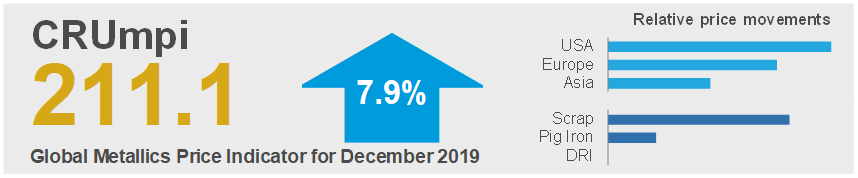

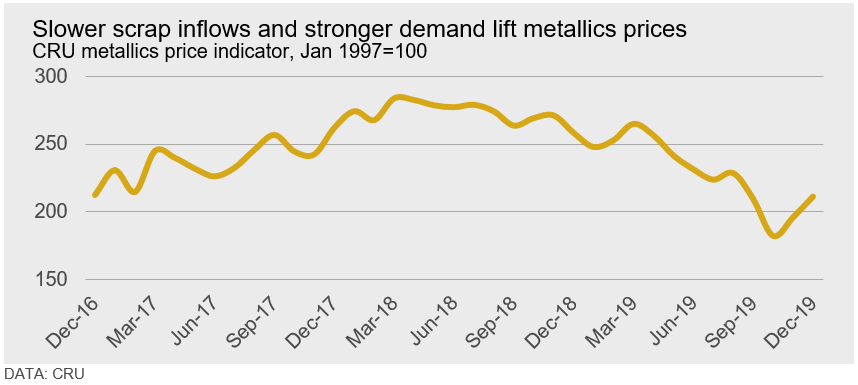

The CRU metallics price indicator (CRUmpi) rose by 7.9 percent m/m to 211.1 (see chart) following price increases in nearly every market. Pervasive market tightness caused by adverse weather and higher domestic demand in major exporting markets forced buyers in import-reliant markets to accept higher prices. We expect these upward price pressures to continue for the short-term.

Metallics markets around the world tightened as restricted supply in exporting regions due to seasonally adverse weather conditions coincided with higher demand. In the U.S., colder weather conditions and relatively low scale prices slowed scrap collection, and mills had to raise prices in order to secure sufficient volumes for December melting programs. The supply squeeze was particularly acute for shredded scrap and, in some regions, this grade traded at a higher price than #1 busheling. A similar squeeze on the premium of prime over obsolete grade scrap occurred in Europe, although this was caused by stronger demand for obsolete-intensive long products relative to prime-intensive automotive steel. Further east, winter weather conditions caused collection and transportation issues in Russia, and mills increased prices to draw out more supply. Mills closer to ports also raised prices to pull material away from exporters.

With their primary source markets tightening, including their own domestic market, Turkish mills have had to pay higher prices to secure scrap supply. From Nov. 8 through Dec. 6, our assessment for HMS 1/2 80:20 CFR Turkey rose by $18 /t to $277 /t. The most recent deal confirmed from the U.S. was done at $295 /t CFR. While these higher prices have reduced or eliminated profitability for rebar exporters, Turkish HR coil exporters are still maintaining a margin. As such, we expect these higher price levels to continue in the near-term until scrap becomes more available internationally.

Prices in most of Asia rose m/m after Vietnamese importers increased bids and mills in Japan increased domestic prices. In Indonesia, meanwhile, government trade action has effectively banned scrap imports. Although market participants expect the ban to be temporary, there is much ambiguity surrounding how long it will last and how new purity restrictions will be enforced.

In China, improved manufacturing activity during November generated a higher volume of prompt scrap arisings. At the same time, winter heating season restrictions have been less strict this year and iron ore and coking coal costs were lower on average compared to scrap. This improved availability of hot metal and scrap resulted in little change m/m in prices.

China has also remained in the merchant pig iron market. This has limited availability for more traditional imports of the material (i.e. the U.S., Italy and Turkey) and has supported increasing prices. Even so, increased availability out of the CIS and weaker-than-average demand from the U.S. and Europe have been factors mitigating even more upward price pressure.

Outlook: Persistent Tightness to Support Higher Prices

In the short term, scrap prices will continue to find support as collection in exporting markets slows seasonally. We expect prices to come under downward pressure once supply becomes more available as the weather warms or the recent steel restocking cycle ends. There are also potential downside risks for certain markets where either mills overbought or where higher scale prices generate more supply than expected.

Pig iron prices will continue to rise in the near term given China’s most recent buying spree. We expect additional price support to come from returning demand from the U.S. and Europe. Still, Chinese purchases will likely slow medium term and increase merchant pig iron availability.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com