Prices

April 9, 2015

February Apparent Steel Supply at 14 Month Low

Written by Brett Linton

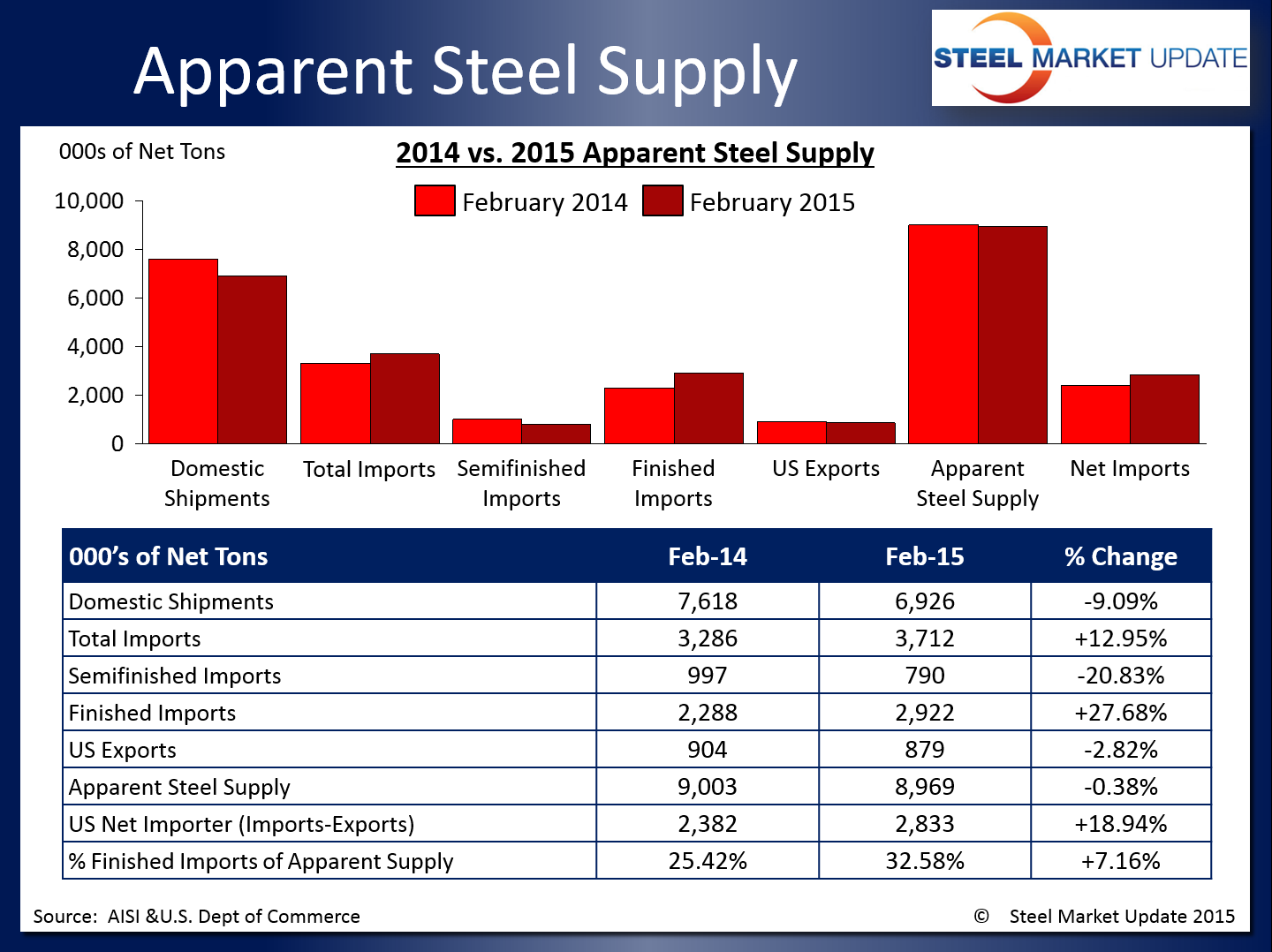

According to the latest data released from the US Department of Commerce and the American Iron and Steel Institute, apparent steel supply for the month of February 2015 is 8,968,831 net tons. Apparent steel supply is calculated by adding domestic steel shipments and finished US steel imports and subtracting total US steel exports.

February supply represents a 33,870 ton or 0.4 percent decrease compared to the same month one year ago. Although finished imports increased 633,441 tons (27.7 percent) and exports declined 25,472 tons (2.8 percent) during this period, it was all negated by a 692,784 ton (9.1 percent) drop in domestic shipments. The net trade balance between imports and exports was a surplus of 2,832,882 tons in February, an increase of 18.9 percent from the same month last year.

SMU Note: Our Premium Level apparent steel supply analysis goes into more detail as we provide data on apparent steel supply for flat and long products. We plan to publish this analysis in the next few days.

When compared to last month when apparent steel supply was at 10,422,485 tons, February supply decreased by 1,453,654 tons or 13.9 percent. The month over month decline is mostly attributed to a 837,146 ton or 10.8 percent decline in domestic shipments and a 663,276 ton or 18.5 percent drop in finished imports.

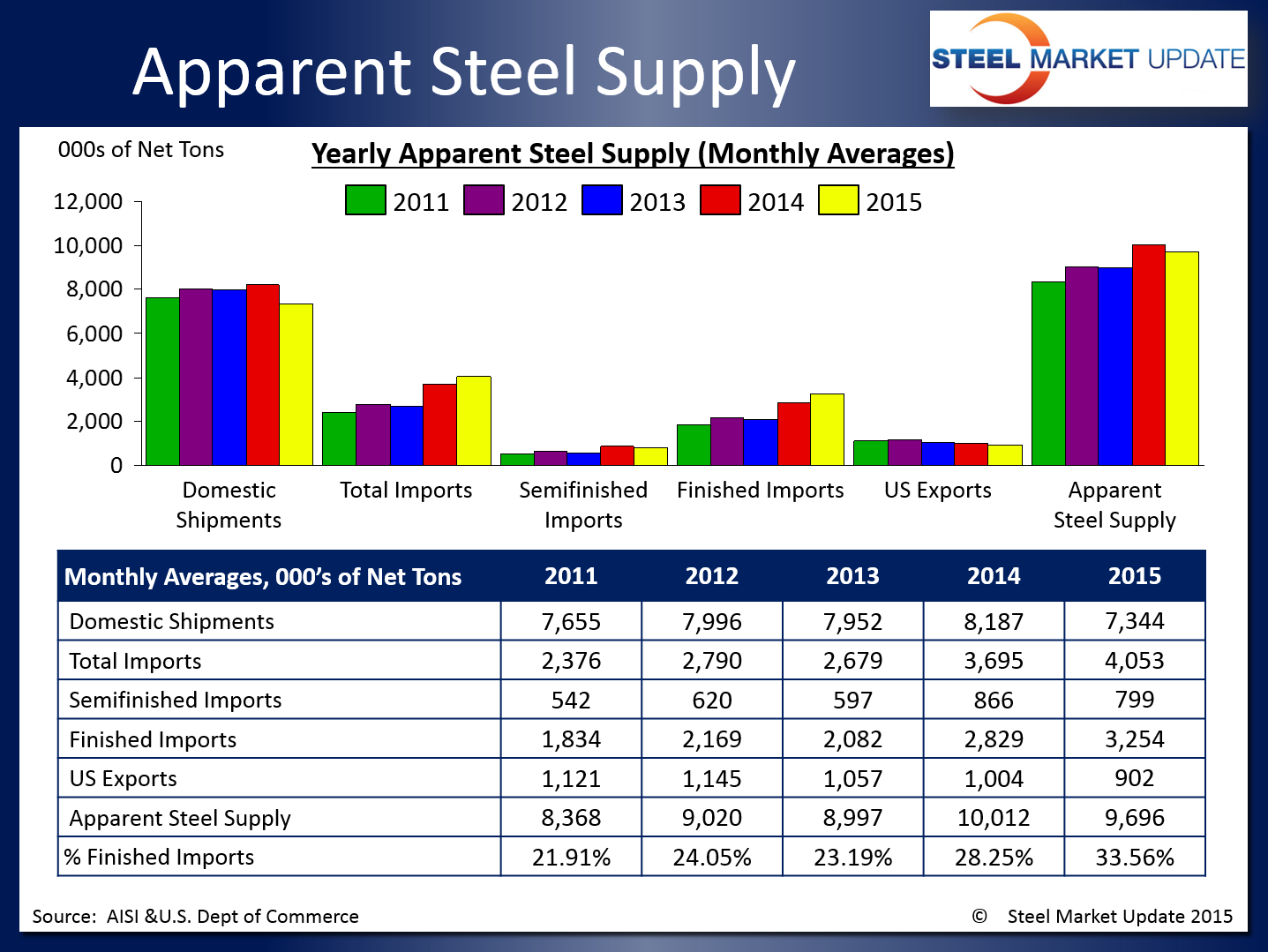

On a year-to-date basis, the 2015 averages are mixed in comparison to previous years. Since the 2015 averages are only based off of two months, and the previous years are over the entire year, the graphic below should be take with a grain of salt.

You can view the interactive graphic of our Apparent Steel Supply history below when you are logged into the website and reading the newsletter online. If you need help accessing or navigating the website, don’t hesitate to contact us at info@SteelMarketUpdate.com or 800-432-3475.

{amchart id=”120″ Apparent Steel Supply- Domestic Shipments, Semi-Fin Imports, Exports}