Market Data

December 2, 2021

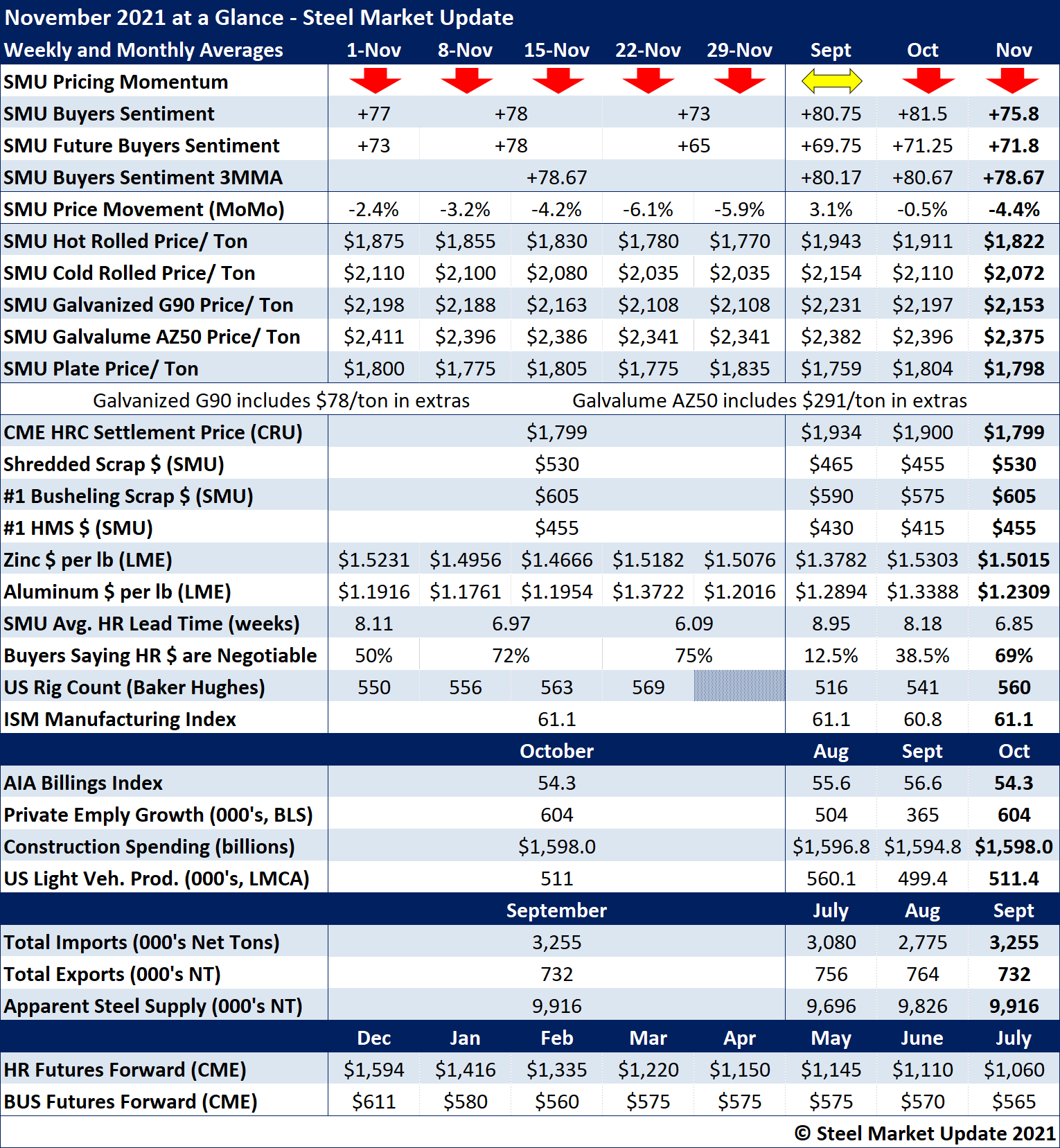

SMU's November at a Glance

Written by Brett Linton

Steel prices declined for the third consecutive month in November, following a 12-month streak of continuous price increases. Hot-rolled coil prices declined $105 per ton throughout the month, with the SMU index averaging $1,770 per ton ($88.50 per cwt) as of Tuesday, Nov. 30. The SMU Price Momentum Indicator for hot-rolled coil was adjusted from Neutral to Lower in mid-October. It was adjusted to Lower for all other sheet products on Nov. 23.

November scrap prices were up $30-75 per ton from the month prior, climbing back towards the historically high prices seen in July. Click here to view and compare prices using our interactive pricing tool.

Zinc spot prices declined following an October surge. They hovered around $1.50 per pound in November and ended the month at $1.5066. Aluminum spot prices also declined from the multi-year high seen in October (excluding the occasional 2-5 day surges commonly seen in aluminum spot prices). They were down to $1.1963 per pound as of Nov. 30.

The SMU Buyers Sentiment Index continues to show a high level of optimism, ending the month at +73. Recall that the early-October reading of +84 was the highest ever recorded. Viewed as a three-month moving average, buyers’ sentiment declined slightly to +78.67 in late-November.

Hot-rolled coil lead times continue to shrink. They were down to an average of 6.09 weeks as of last week, their lowest level since October 2020. The percentage of buyers reporting that mills are willing to negotiate on hot-rolled coil prices continues to rise. It reached 75% in late November. A history of HRC lead times can also been viewed within our interactive pricing tool.

Key indicators of steel demand continue to remain positive, as has been the case for months. The ISM Manufacturing Index indicated further economic expansion for the 18th consecutive month, and the AIA Billings Index indicated that construction activity has recovered for the 10th month in a row. In the energy sector, the active drill rig count was up week after week – and it reached a 20-month high last Friday. Total U.S. steel imports, exports and apparent steel supply continue to improve each month, with each at a much healthier level than this time last year.

See the chart below for other key metrics in the month of November:

By Brett Linton, Brett@SteelMarketUpdate.com