Market Data

September 12, 2023

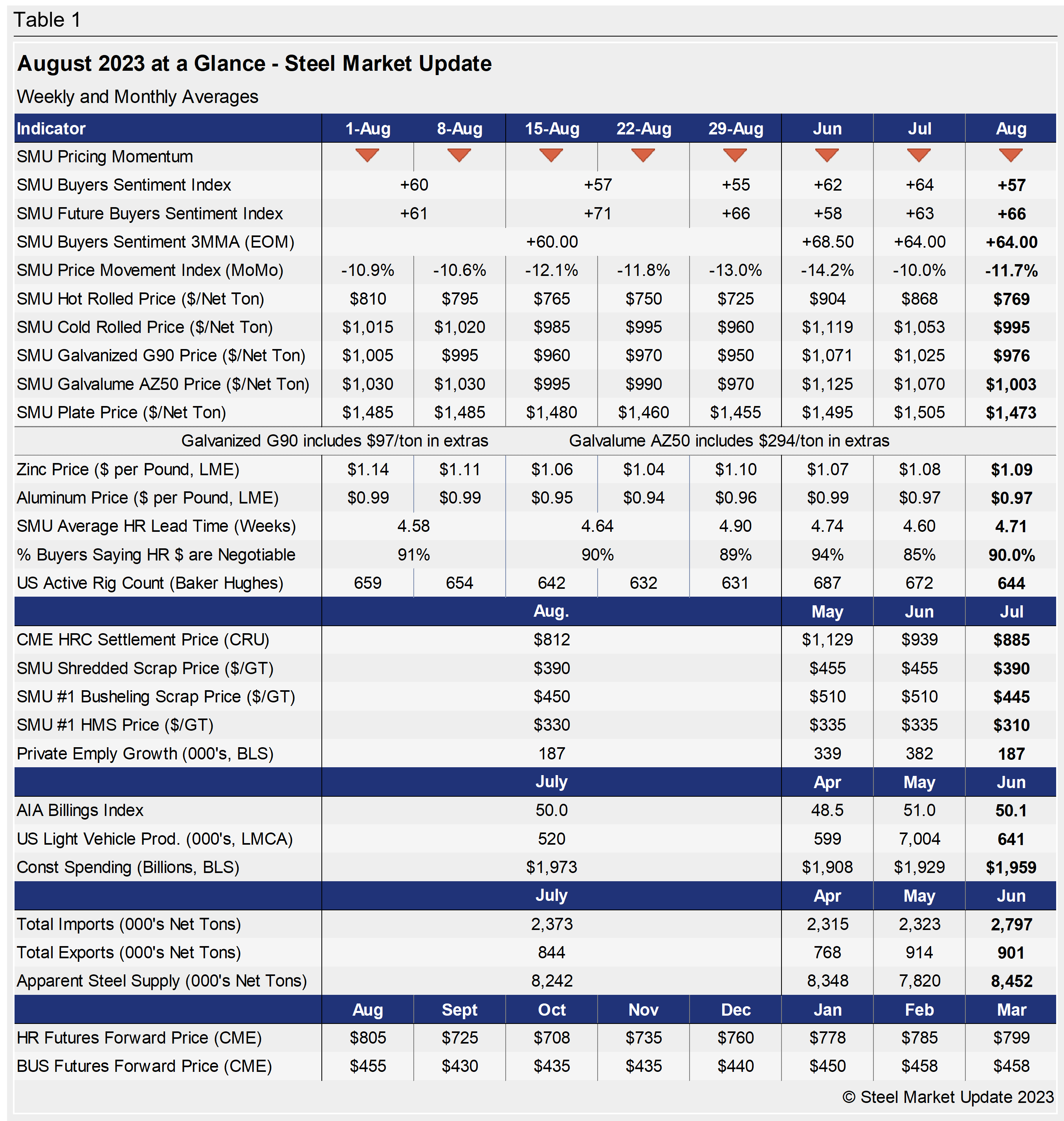

SMU's August at a Glance

Written by David Schollaert

Steel prices kept falling throughout last month. Hot-rolled coil (HRC) prices ended August at $725 per ton ($36.25 per cwt) on average, having fallen by $105 per ton during the month.

The SMU Price Momentum Indicator for sheet products remained pointing Lower as tags continued to slip due to declining demand. The Price Momentum on plate shifted to Neutral at the end of April and has remained there since. While prices have edged lower, the market has yet to determine a clear direction.

Raw material prices were largely sideways last month, temporarily pausing a downtrend that had been in place since April. Scrap prices were flat on average in August. Despite some movement earlier in the month, zinc and aluminum spot prices were largely stable, remaining within historic levels. You can view and chart multiple products in greater detail using our interactive pricing tool here.

The SMU Steel Buyers Sentiment Index remained positive but edged down during the month. Current Buyers Sentiment slipped from +64 in July to +55 in August, while Future Sentiment hovered at an average of roughly +66. Our Buyers Sentiment 3MMA Index (measured as a three-month moving average), has been eroding over the past two months, to +60 in August from +64 the month prior.

Hot rolled lead times averaged 4.71 weeks in August, up marginally from 4.60 weeks the month prior. SMU expects lead times to hover around current levels, but ease slightly in September as some summer seasonality may bleed into the latter part of Q3. A history of HRC lead times can be found in our interactive pricing tool.

Roughly 90% of hot-rolled buyers reported in August that mills were willing to negotiate on prices, up from about 85% in July.

Key indicators of steel demand are showing some signs of weakness overall, and nowhere near the bullish levels some had earlier in the year. While there are some backlogs in the energy and construction sectors, labor contract negotiations between the United Auto Workers (UAW) union and Detroit’s Big Three automakers remain in question, and a strike looking more and more likely.

See the chart below for other key metrics for the month of August: