Prices

October 24, 2023

SMU Price Ranges: Sheet Up as Price Hikes Gain Traction

Written by David Schollaert & Michael Cowden

Sheet prices rose for a fourth consecutive week following a second wave of price hikes announced by domestic mills.

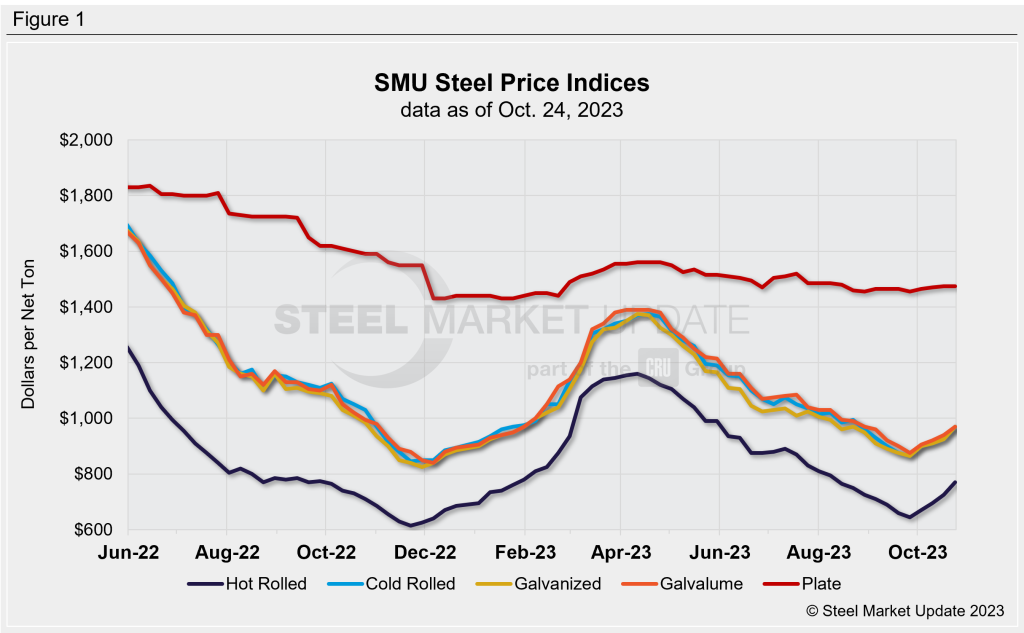

SMU’s average hot-rolled coil price now stands at $770 per ton ($38.50 per cwt), up $45 per ton from a week ago and up $125 per ton from a 2023 low of $645 per ton in late September.

Cold-rolled and coated products (both up $45 per ton to $970 per ton) saw similar gains. Plate prices were unchanged.

Recall that late September was when the sheet price rally began, sparked by a price hike from Cleveland-Cliffs that was quietly followed by other mills.

Most major US sheet mills, including Cliffs, publicly announced a second wave of price hikes last Thursday.

Nucor, Cliffs, and ArcelorMittal specified minimum base prices of $800 per ton for HRC. U.S. Steel, in contrast, specified an increase amount (up $100 per ton) but not a target price.

The price hikes have succeeded in moving some buyers off the sidelines. Market participants said the gains were also supported by long lead times, low customer inventories, and resilient demand – despite the expanding UAW strike.

Indeed, some said that lead times, especially for coated products, were already into 2024. And several predicted that mills would continue to raise prices.

Our sheet pricing momentum indicators, therefore, remain pointed upward. Our plate momentum indicator remains at neutral.

Hot-Rolled Coil

The SMU price range is $740–800 per net ton ($37.00–40.00 per cwt), with an average of $770 per ton ($38.50 per cwt) FOB mill, east of the Rockies. The bottom end of our range increased $40 per ton vs. one week ago, while the top end of the range moved up $50 per ton compared to the prior week. Our overall average is up $45 per ton WoW. Our price momentum indicator for HRC continues to point higher, meaning SMU expects prices will increase over the next 30 days.

Hot Rolled Lead Times: 4–7 weeks

Cold-Rolled Coil

The SMU price range is $940–1,000 per net ton ($47.00–50.00 per cwt), with an average of $970 per ton ($48.50 per cwt) FOB mill, east of the Rockies. The lower end of our range was up $40 per ton WoW, while the top end was $50 per ton higher compared to a week ago. Our overall average is up $45 per ton WoW. Our price momentum indicator for CRC continues to point higher, meaning SMU expects prices will increase over the next 30 days.

Cold Rolled Lead Times: 5–8 weeks

Galvanized Coil

The SMU price range is $940–1,000 per net ton ($47.00–50.00 per cwt), with an average of $970 per ton ($48.50 per cwt) FOB mill, east of the Rockies. The lower end of our range was up $40 per ton vs. last week, while the top end of our range was also up $50 per ton WoW. Thus, our overall average is up $45 per ton vs. the prior week. Our price momentum indicator on galvanized steel continues to point higher, meaning SMU expects prices will increase over the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $1,037–1,097 per ton with an average of $1,067 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 5-8 weeks

Galvalume Coil

The SMU price range is $940–1,000 per net ton ($47.00–50.00 per cwt), with an average of $970 per ton ($48.50 per cwt) FOB mill, east of the Rockies. The lower end of our range was up $20 per ton vs. last week, while the top end of the range was $40 per ton higher WoW. Our overall average was up $30 per ton compared to one week ago. Our price momentum indicator on Galvalume steel continues to point higher, meaning SMU expects prices will increase over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,234–1,294 per ton with an average of $1,264 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-10 weeks

Plate

The SMU price range is $1,450–1,500 per net ton ($72.50–75.00 per cwt), with an average of $1,475 per ton ($73.75 per cwt) FOB mill. Both the lower end of our range and the top end of our range were unchanged compared to the week prior. Thus, our overall average is sideways vs. one week ago. Our price momentum indicator on steel plate remains neutral, meaning there is no clear indication where prices will head over the next 30 days.

Plate Lead Times: 4-7 weeks

SMU Note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert