CRU

February 16, 2024

CRU: Scrap prices hit by weak demand offsetting tight supply

Written by Puneet Paliwal

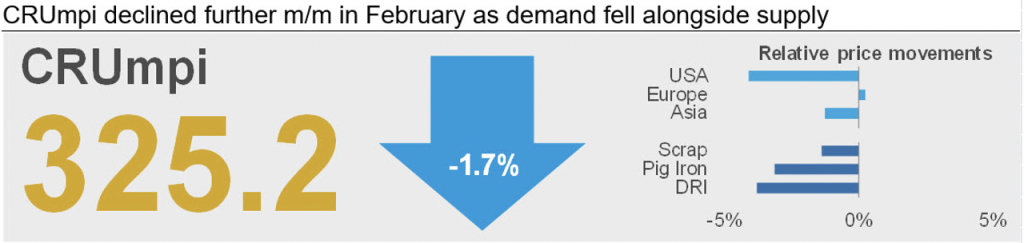

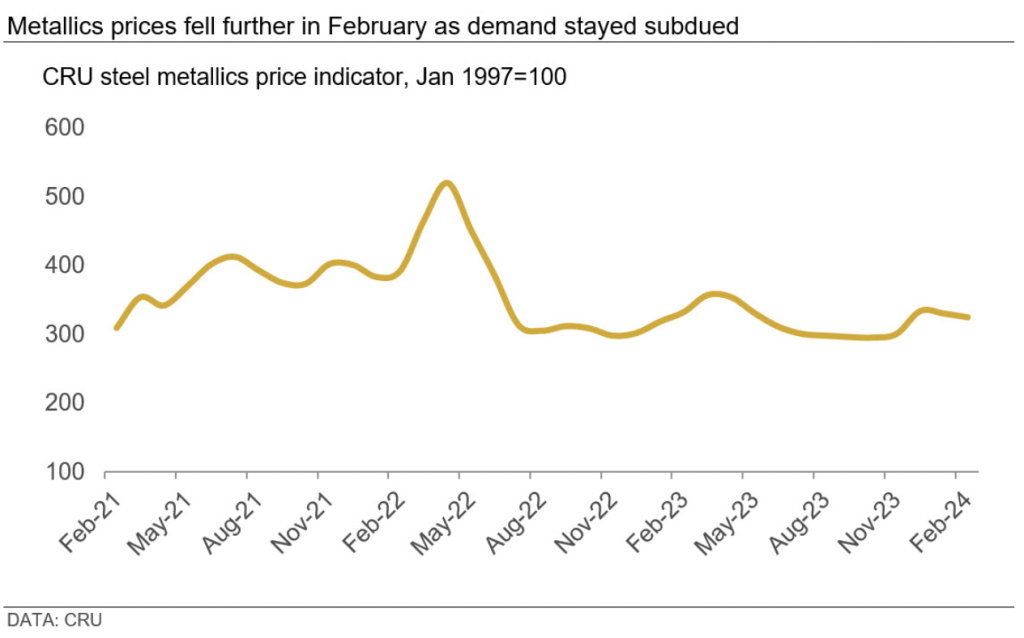

The CRUmpi declined by 1.7% month over month (m/m) to 325.2 in February, compared to a 4.3% m/m increase in February 2023. This is the CRU metallics price indicator, and is derived from steel scrap, pig iron and DRI/HBI price assessments.

Supply decreased for both scrap and pig iron due to seasonal factors, but availability remained ample amid tepid demand in a challenging steel market. Metallics prices showed more resilience in the European market compared to the US and Asia as suppliers resisted price reduction citing higher cost pressure. Meanwhile, ongoing shipping disruptions in the Red Sea continue to impact scrap trade between Europe and Asia.

In the US, scrap prices fell to the tune of $20–30/long ton m/m for busheling and HMS scrap, while remained stable m/m for shredded scrap. Steelmakers in most regional markets within the US were able to complete their purchases with ease despite winter weather hindering flows to scrapyards. This is because scrap availability remained ample due to reduced export sales to Turkey and weaker buy programs of domestic mills, most of which were well stocked heading into February.

Similar to the US, scrap prices were flat to down m/m across major Asian markets as buyers resisted fresh purchases ahead of holidays in China and Southeast Asia and as steel mill utilization rates remain reduced. Chinese EAF steelmaking utilization rates dropped to 35% in early February compared to 63% in early January in response to labor shortages and weaker margins. Accordingly, mills lowered their scrap bids to procure much lesser volumes. In Japan, the recent depreciation of the yen had an unusual effect on their scrap export prices, which rose in yen terms but dropped by $5–10 per metric ton (mt) in USD terms.

Meanwhile, scrap buyers in Bangladesh were able to negotiate $10/mt m/m lower scrap import prices due to low demand in the seaborne market by Indian and Turkish buyers. This price reduction happened at a time when liquidity conditions improved in Bangladesh and scrap demand rose due to an increase in steel mill run rates.

Unlike the US and Asian markets, the scrap market in the European Union was better balanced as weak demand was offset by limited supply. Steelmakers in the region were slow to ramp up operations to keep steel prices supported amid subdued finished steel demand. Consequently, their scrap orders remained slow. However, scrap supply in the region fell sharply due to poor weather combined with holidays in December and January. Some scrap sellers also chose to hold off on sales in the past month, discouraged by weaker margins amid rising costs – particularly that of transportation. Industrial origin scrap supply also reduced, specifically from automakers in Germany. Thus, a combination of weak demand and weaker supply kept scrap prices supported in the EU.

Meanwhile, pig iron prices in the US fell in line with downward revisions to local scrap prices while remaining stable m/m in other major regions. Reduced supply from Brazil was offset by softened demand in the US, as steel mills carried forward sufficient inventories from the end-2023 restocking cycle. Moreover, although Ukrainian-origin pig iron became more accessible to US buyers, buying interest remained low due to the risk-averse behavior of buyers. European pig iron price was unchanged m/m despite availability of competitive price offers from Russian suppliers, as buyers intend to limit their exposure to Russia. Italian HBI import price dropped $15/mt m/m due to rising supplies from Libya.

This article was first published by CRU. Learn more about CRU’s services at www.crugroup.com/analysis.