Market Data

July 18, 2024

SMU survey: Lead times remain historically low

Written by Brett Linton

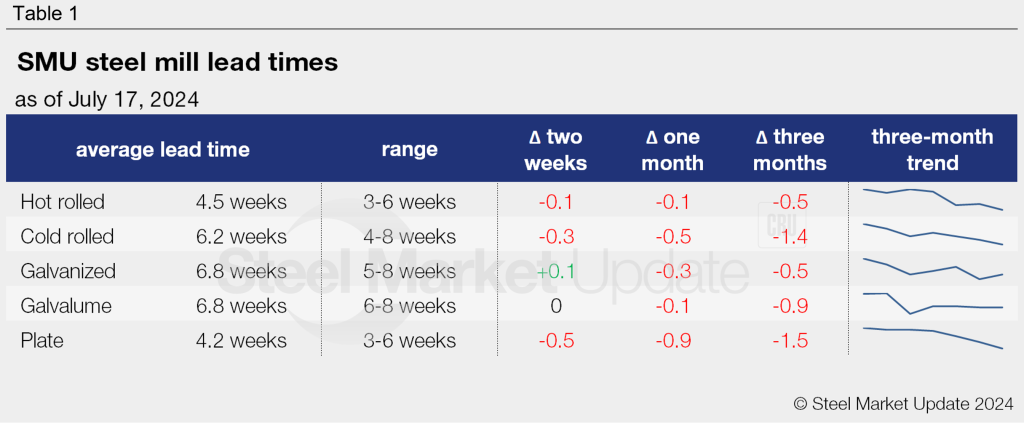

Steel mill lead times remain short and relatively flat from two weeks earlier, according to SMU’s latest market survey. Of the sheet and plate products SMU tracks, production times for all materials are nearing historical lows, some at record lows not seen in years.

Survey respondents reported a reduction in lead times for hot-rolled, cold-rolled, and plate steel compared to our previous check on the market in early-July. The last time we saw hot rolled lead times this low was exactly one year ago. We have to look all the way back to late 2022 to find plate and cold rolled production times as short those today.

Lead times for coated products were steady to slightly extended this week compared to two weeks prior, but remain significantly short, both near lows not seen since last August.

Table 1 below summarizes current lead times and recent trends.

Survey results

Over two-thirds of the companies we surveyed this week categorized current mill production times as shorter than normal. The majority of the remainder reported lead times were within typical levels.

When asked where they expect lead times to be two months into the future, 32% of this week’s respondents believe lead times will longer at that time (down from 21% when polled earlier this month); 62% forecast production times will remain stable (down from 67% previously); and 6% think they could shrink further (vs 12% previously).

Here’s what respondents are saying:

“I don’t think extending lead times will force people to buy at this point.”

“They are already very low… so would be hard to go much lower.”

“Unless capacity comes offline somewhere (anywhere?), I don’t expect any sort of real stretching out of lead times.”

“I think they will extend over the next month but then flatten.”

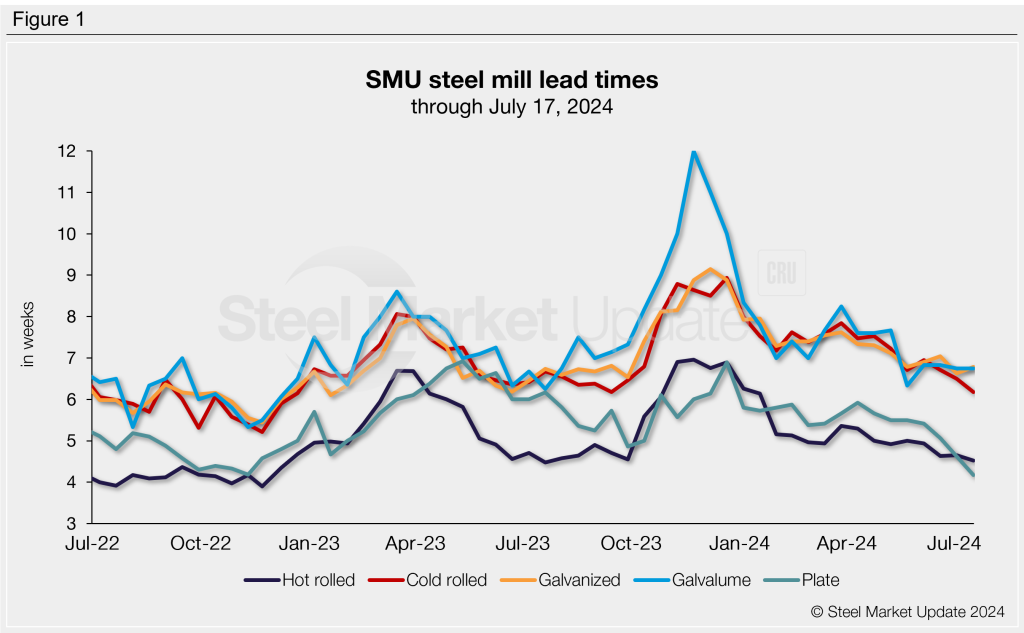

Figure 1 below tracks lead times for each product over the past two years.

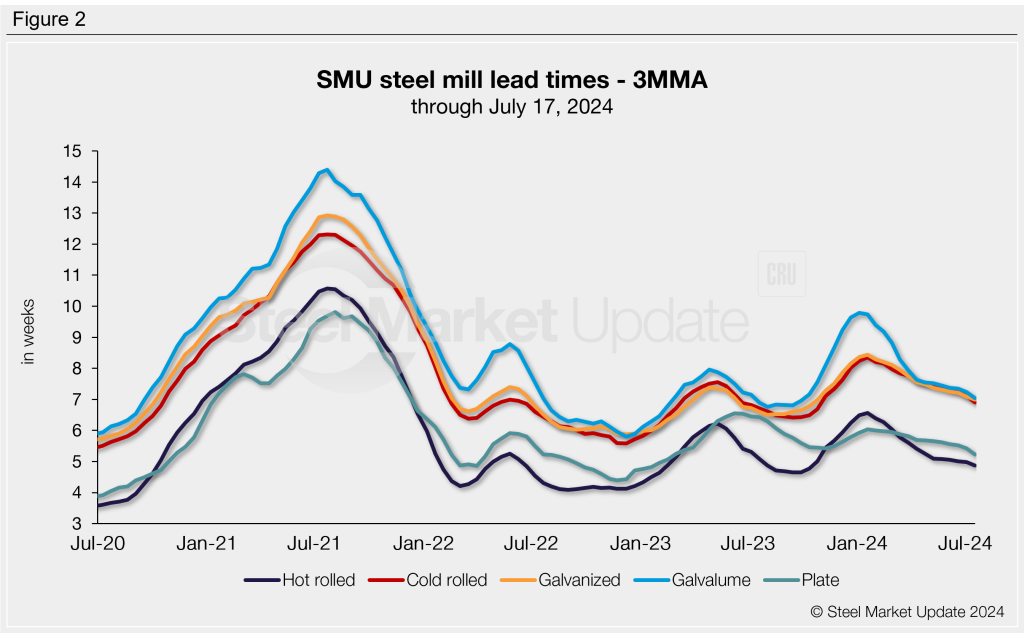

3MMA lead times

Looking at lead times on a three-month moving average (3MMA) basis smooths out the variability seen in our biweekly readings. The 3MMA lead times have continued to ease across the board this week, remaining at some of the lowest levels seen since late 2023.

The hot rolled 3MMA is now down to 4.87 weeks, cold rolled at 6.91 weeks, galvanized at 6.99 weeks, Galvalume at 7.05 weeks, and plate at 5.23 weeks.

Figure 2 highlights lead time movements across the past four years.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.