Market Data

September 12, 2024

SMU survey: Buyers report mills still willing to negotiate prices

Written by Brett Linton

Almost three out of every four steel buyers who participated in our market survey this week reported mills are willing to negotiate new order prices. While negotiation opportunities still favor buyers, rates have edged lower from our previous market check, a downward trend witnessed since July.

Every other week, SMU polls hundreds of steel market executives asking if domestic mills are willing to negotiate lower spot pricing on new orders. As shown in Figure 1, 72% of all buyers we surveyed this week reported mills were willing to talk price. This is five percentage points lower than our late-August rate, and down from the 80-92% range seen across June and July.

Negotiation rates by product

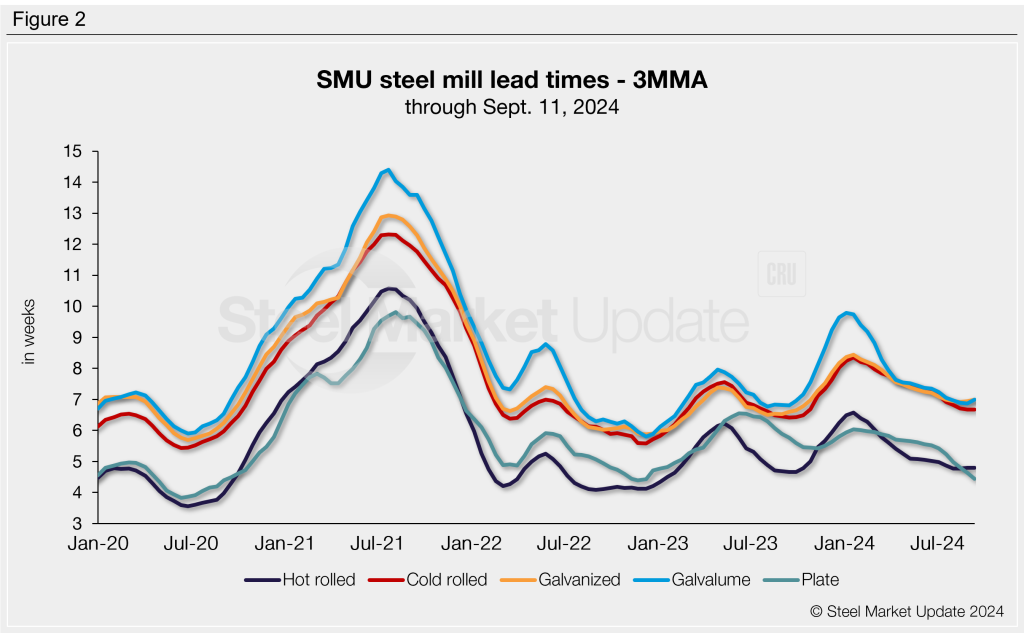

As seen in Figure 2, negotiation rates are mixed between sheet and plate products, ranging from 61-89%. Aside from Galvalume, negotiation rates on all sheet products are at some of the lowest levels seen since March/April of this year. Negotiation rates on plate products continue to be the strongest. Rates by product are:

- Hot rolled: 71%, unchanged from late-August.

- Cold rolled: 61%, down 10 percentage points.

- Galvanized: 72%, down 11 percentage points.

- Galvalume: 86%, up four percentage points.

- Plate: 89%, up one percentage point.

Here’s what some survey respondents had to say:

“Depending on mill, more volume can do better, but not by much.”

“Curious to see if the trade case strengthens galvanized.”

“Some hesitancy with the announcement of the new [galvanized] tariffs.”

“With tons yes [plate].”

Note: SMU surveys active steel buyers every other week to gauge their steel suppliers’ willingness to negotiate new order prices. The results reflect current steel demand and changing spot pricing trends. Visit our website to see an interactive history of our steel mill negotiations data.