Plate

October 1, 2024

SMU price ranges: Sheet sideways to up, plate slips

Written by Brett Linton

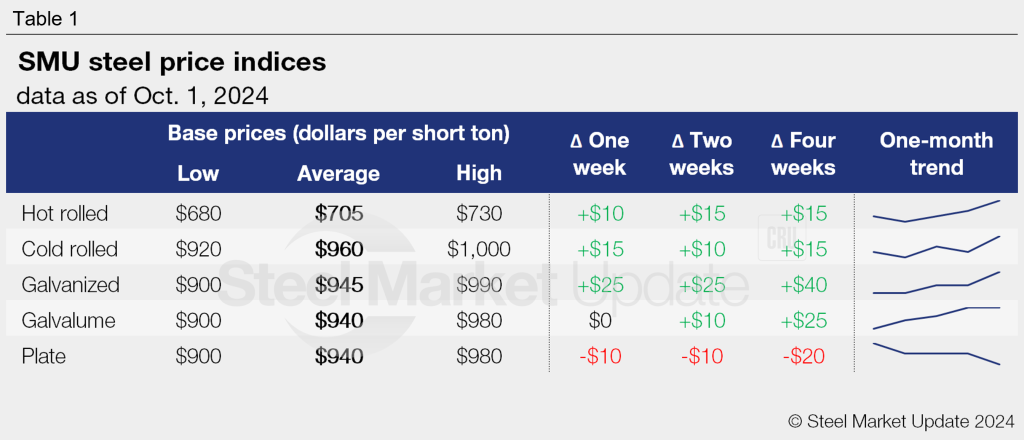

Steel prices ticked higher this week for most of the sheet products SMU tracks. Meanwhile, plate prices edged lower following three weeks of stability.

SMU price indices for hot-rolled, cold-rolled, and galvanized steel all increased this week. Our Galvalume index remained unchanged week over week (w/w), while plate prices eased. Prior to this week, each of our indices had fluctuated within a relatively narrow range throughout September.

A few factors could be driving this upward movement in sheet prices. Notably, mill price increases, declining domestic production, and the coated trade case. There has been no noticeable impact yet from the port strike.

Our hot-rolled steel index increased $10 per short ton (st) w/w to $705/st. It is now up to levels last seen in June. Cold-rolled steel prices recovered $15/st from last week to $960/st, the highest average recorded since early July.

Our galvanized index jumped to a 14-week high of $945/st this week, up $25/st w/w. Galvalume base prices held steady from last week at $940/st, the highest rate recorded in the past 12 weeks.

Following a brief pause, plate prices resumed their downward movement this week, declining $10/st w/w to $940/st on average. Plate prices have overall trended downward since their mid-2022 peak. The last time plate prices were in this territory was the first week of 2021.

SMU’s sheet price momentum indicator remains at neutral following our Sept. 10 adjustment. Our plate price momentum indicator remains at lower.

Hot-rolled coil

The SMU price range is $680-730/st, averaging $705/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is unchanged w/w. Our overall average is up $10/st w/w. Our price momentum indicator for hot-rolled steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Hot rolled lead times range from 3-6 weeks, averaging 4.9 weeks as of our Sept. 25 market survey.

Cold-rolled coil

The SMU price range is $920–1,000/st, averaging $960/st FOB mill, east of the Rockies. The lower end of our range is up $30/st w/w, while the top end is unchanged w/w. Our overall average is up $15/st w/w. Our price momentum indicator for cold-rolled steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Cold rolled lead times range from 5-9 weeks, averaging 6.9 weeks through our latest survey.

Galvanized coil

The SMU price range is $900–990/st, averaging $945/st FOB mill, east of the Rockies. The lower end of our range is up $40/st w/w, while the top end is up $10/st w/w. Our overall average is up $25/st w/w. Our price momentum indicator for galvanized steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $997–1,087/st, averaging $1,042/st FOB mill, east of the Rockies.

Galvanized lead times range from 5-9 weeks, averaging 7.3 weeks through our latest survey.

Galvalume coil

The SMU price range is $900–980/st, averaging $940/st FOB mill, east of the Rockies. Our range is unchanged w/w. Our price momentum indicator for Galvalume steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,194–1,274/st, averaging $1,234/st FOB mill, east of the Rockies.

Galvalume lead times range from 6-9 weeks, averaging 7.3 weeks through our latest survey.

Plate

The SMU price range is $900–980/st, averaging $940/st FOB mill. The lower end of our range is unchanged w/w, while the top end is down $20/st w/w. Our overall average is down $10/st w/w. Our price momentum indicator for plate remains at lower, meaning we expect prices to decline over the next 30 days.

Plate lead times range from 2-6 weeks, averaging 4.0 weeks through our latest survey.

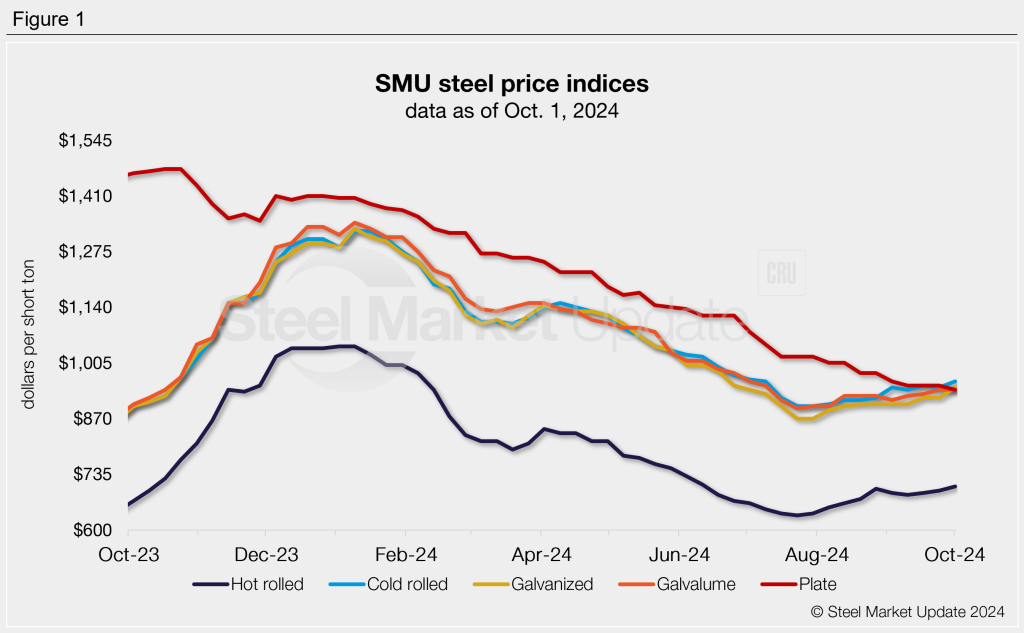

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.