Market Data

April 29, 2025

SMU price ranges: Sheet and plate prices slip

Written by Brett Linton

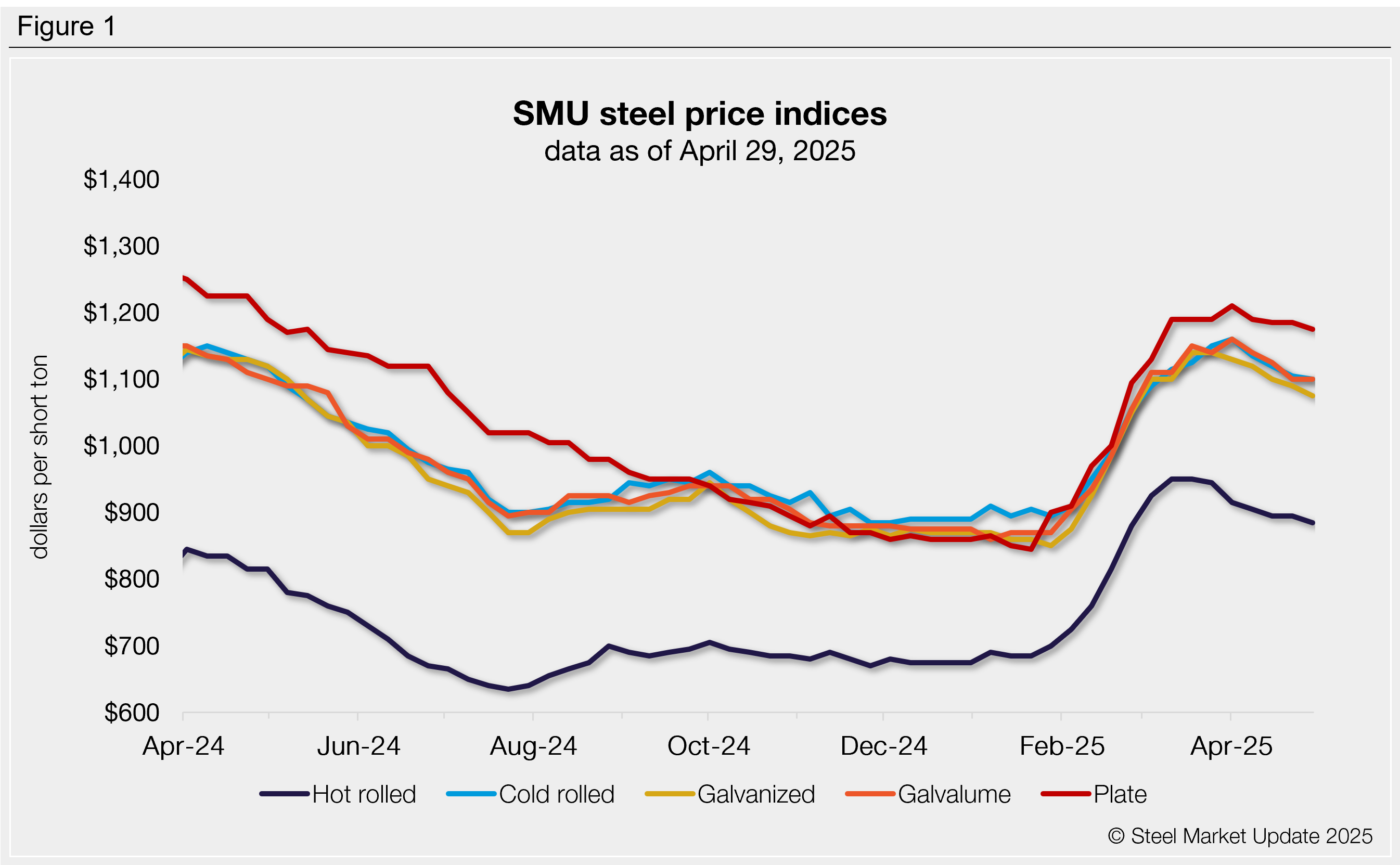

Most sheet and plate steel prices declined yet again this week, with four of SMU’s five indices moving lower. The market continues to ease as buyers stay on the sidelines, wary of further declines. Even with tariff noise quieting down, May scrap is showing weakness. Demand is still soft, with most buyers sticking to contract minimums as prices trend downward.

After last week’s pause, hot-rolled coil prices resumed their downward movement this week, easing $10 per short ton (st) to $885/st. Hot rolled prices have fallen $30/st in the past month.

Our cold rolled index declined for the fourth consecutive week, slipping $5/st week over week (w/w) to $1,100/st. Galvanized prices also ticked lower for the fifth week in a row, easing $15/st, while Galvalume prices held steady. Tandem product prices are all $55-60/st less than those seen one month ago.

Plate prices declined $10/st w/w, now $35/st lower than the one-year high seen at the start of the month.

SMU’s price momentum indicator is now at lower for both sheet and plate products, signaling that we expect prices to trend lower over the next 30 days. Plate momentum was adjusted from neutral to lower this week, while sheet momentum was adjusted the same last week.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $820-950/st, averaging $885/st FOB mill, east of the Rockies. The lower end of our range is down $20/st w/w, while the top end is unchanged. Our overall average is down $10/st w/w. Our price momentum indicator for hot-rolled steel remains at lower, meaning we expect prices to decline over the next 30 days.

Hot rolled lead times range from 3-6 weeks, averaging 5.0 weeks as of our April 16 market survey. We will publish updated lead times this Thursday.

Cold-rolled coil

The SMU price range is $1,030–1,170/st, averaging $1,100/st FOB mill, east of the Rockies. The lower end of our range is down $10/st w/w, while the top end is unchanged. Our overall average is down $5/st w/w. Our price momentum indicator for cold-rolled steel remains at lower, meaning we expect prices to decline over the next 30 days.

Cold rolled lead times range from 5-8 weeks, averaging 6.6 weeks through our latest survey.

Galvanized coil

The SMU price range is $1,030–1,120/st, averaging $1,075/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $30/st. Our overall average is down $15/st w/w. Our price momentum indicator for galvanized steel remains at lower, meaning we expect prices to decline over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,127–1,217/st, averaging $1,172/st FOB mill, east of the Rockies.

Galvanized lead times range from 4-8 weeks, averaging 6.8 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,050–1,150/st, averaging $1,100/st FOB mill, east of the Rockies. Our range is unchanged w/w. Our price momentum indicator for Galvalume steel remains at lower, meaning we expect prices to decline over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,344–1,444/st, averaging $1,394/st FOB mill, east of the Rockies.

Galvalume lead times range from 7-9 weeks, averaging 7.5 weeks through our latest survey.

Plate

The SMU price range is $1,080–1,270/st, averaging $1,175/st FOB mill. The lower end of our range is down $20/st w/w, while the top end is unchanged. Our overall average is down $10/st w/w. Our price momentum indicator for plate has been adjusted to lower, meaning we expect prices to decline over the next 30 days.

Plate lead times range from 4-7 weeks, averaging 5.9 weeks through our latest survey.

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.