Market Data

May 6, 2025

SMU price ranges: Steel's slow slide into summer continues

Written by Brett Linton & Michael Cowden

Sheet prices were flat or down again this week as market participants brace for what some said could be a slow summer for steel.

The declines came after Nucor lowered its list price for hot-rolled coil by $20 per short ton (st) and as certain newer capacity continued to offer steep discounts to third-party pricing indices.

Steel buyers said Nucor’s price decrease was a public acknowledgement of what most of the market had already known – that sheet prices were moving lower in a more significant way. The question now is whether mills and service centers will manage the decline or whether prices might fall rapidly, they said.

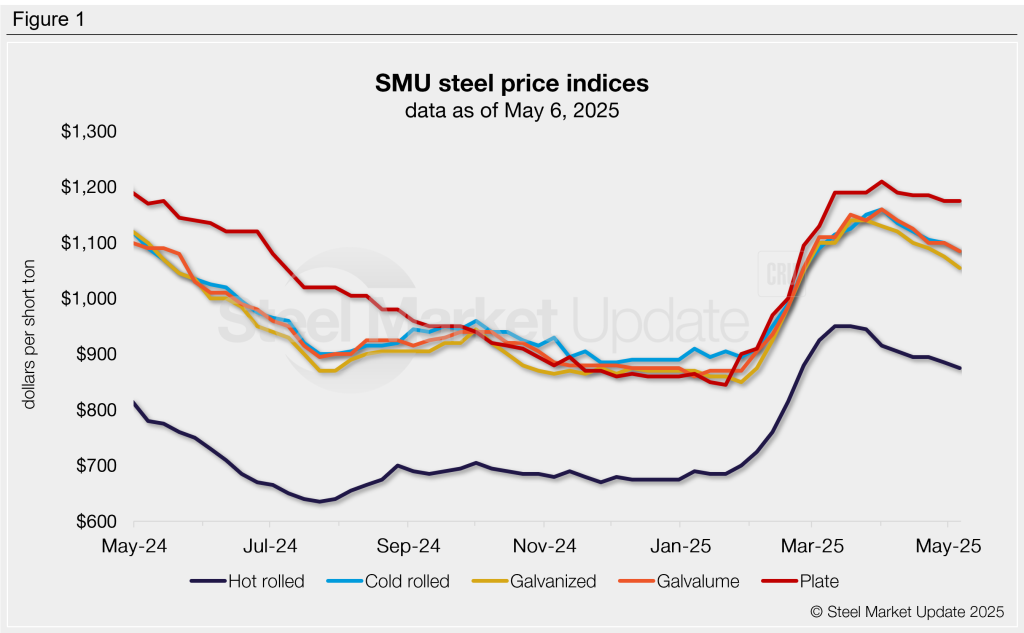

Prices and momentum

SMU’s hot-rolled coil price stands at $875 per ton on average, down $10/st from last week. Tons from new capacity were reported to be approximately $100/st below that figure.

Our cold-rolled (CR) base price dropped to $1,085/st on average, down $15/st from a week ago. Galvanized base prices slipped to $1,055/st on average (down $20/t), and Galvaume prices slipped to $1,085/st on average (down $15/st). SMU’s plate price was unchanged at $1,175/st.

SMU’s price momentum indicators remains at lower for both sheet and plate products, signaling that we expect prices to trend lower over the next 30 days.

Market commentary

Few market participants see upside to prices with scrap expected to slip again in May. Most sources said day-to-day business remained intact. But some said activity was disappointing compared to what they had expected earlier in the year. Some blamed tariff uncertainty. Others said it was more an issue of increased domestic capacity colliding with softer demand.

Steel consumers said they are generally out of the spot market, with some noting that they continue to buy only to their contract minimums. The resulting thin spot market has perhaps kept prices from falling more significantly. Simply put, mills don’t think that lowering prices would bring in much new business, they said.

Meanwhile, mill lead times appear poised to move lower again. Case in point: Steel Dynamics typically keeps lead times short. But other mills that typically have longer lead times now are on par with or shorter than SDI. In other words, some producers continue to have May availability not only HR but also CR and coated products.

Sources continued to debate whether tariffs might help or hurt business over the longer term. Some pointed to a rumored trade deal with the UK – one that could feature steel quotas – as a potential template for trade pacts with other countries. And others said that Section 232 tariffs on downstream goods could eventually provide a significant boost to demand. But more immediate concerns centered around potential supply chain disruptions stemming from President Trump’s tariffs.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $820-930/st, averaging $875/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $20/st. Our overall average is down $10/st w/w. Our price momentum indicator for hot-rolled steel remains at lower, meaning we expect prices to decline over the next 30 days.

Hot rolled lead times range from 3-6 weeks, averaging 5.1 weeks as of our April 30 market survey. We will publish updated lead times this Thursday.

Cold-rolled coil

The SMU price range is $1,020–1,150/st, averaging $1,085/st FOB mill, east of the Rockies. The lower end of our range is down $10/st w/w, while the top end is down $20/st. Our overall average is down $15/st w/w. Our price momentum indicator for cold-rolled steel remains at lower, meaning we expect prices to decline over the next 30 days.

Cold rolled lead times range from 5-8 weeks, averaging 6.6 weeks through our latest survey.

Galvanized coil

The SMU price range is $990–1,120/st, averaging $1,055/st FOB mill, east of the Rockies. The lower end of our range is down $40/st w/w, while the top end is unchanged. Our overall average is down $20st w/w. Our price momentum indicator for galvanized steel remains at lower, meaning we expect prices to decline over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,087–1,217/st, averaging $1,152/st FOB mill, east of the Rockies.

Galvanized lead times range from 4-8 weeks, averaging 6.7 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,020–1,150/st, averaging $1,085/st FOB mill, east of the Rockies. The lower end of our range is down $30/st w/w, while the top end is unchanged. Our overall average is down $15/st w/w. Our price momentum indicator for Galvalume steel remains at lower, meaning we expect prices to decline over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,314–1,444/st, averaging $1,379/st FOB mill, east of the Rockies.

Galvalume lead times range from 6-8 weeks, averaging 7.0 weeks through our latest survey.

Plate

The SMU price range is $1,080–1,270/st, averaging $1,175/st FOB mill. Our range was unchanged this week. Our price momentum indicator for plate remains at lower, meaning we expect prices to decline over the next 30 days.

Plate lead times range from 4-7 weeks, averaging 5.9 weeks through our latest survey.

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton