Prices

May 13, 2025

HRC vs. prime spread narrows further in May

Written by Ethan Bernard & Stephen Miller

The price spread between hot-rolled coil (HRC) and prime scrap narrowed again in May, according to SMU’s most recent pricing data.

SMU’s average HRC price fell week over week (w/w) and month over month. The May price for busheling also dropped from April.

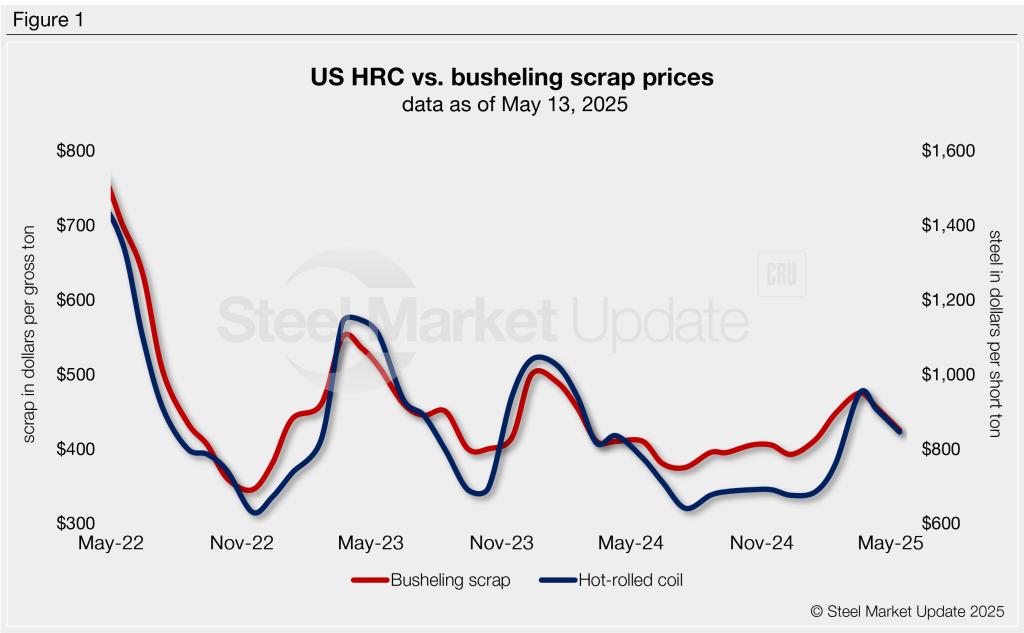

Our average HRC price as of May 13 stands at $845 per short ton (st) FOB mill, east of the Rockies. That’s down $30/st from the previous week and a drop of $50/st m/m.

Meanwhile, busheling tags also fell m/m in May. They are off $30.00 per gross ton (gt) from last month, with an average of $425/gt. Figure 1 shows price histories for each product.

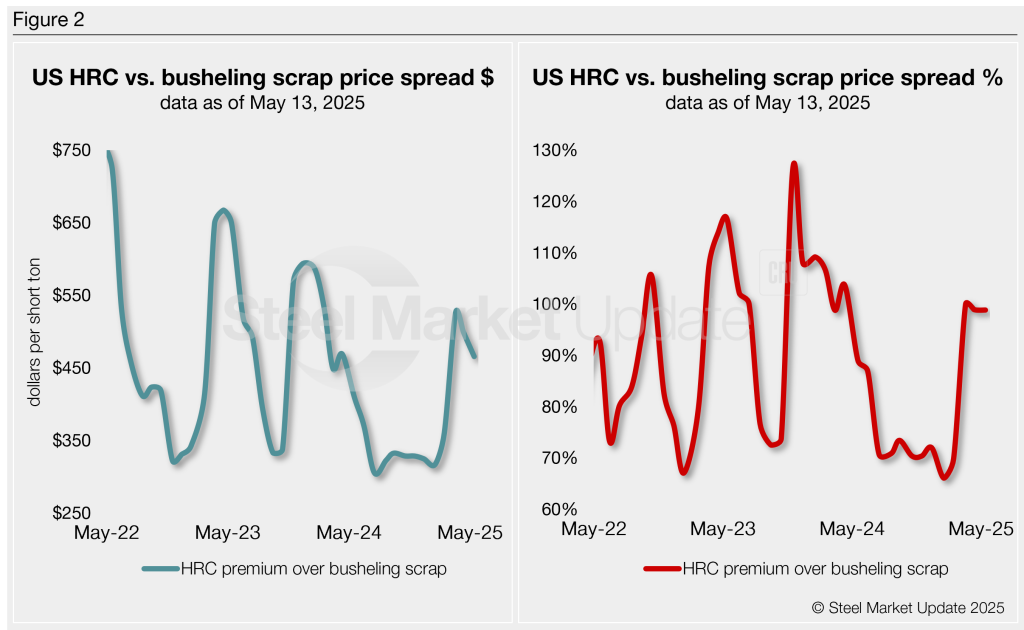

After converting scrap prices to dollars per short ton for an equal comparison, the differential between HRC and busheling scrap prices was $466/st as of May 13. That’s a decrease of $33/st from a month earlier (Figure 2). It has narrowed since March.

What’s going on?

This narrowing was mainly caused by the increased demand for #1 Busheling in a supply-short market. Lagging manufacturing is generating less prime scrap.

The HRC mills prefer prime scrap vs. shredded. So, busheling only went down $30/gt while shredded went down as much as $50. This caused the narrowing as HRC went down further.

If HRC maintains its price going into the summer months, we may see further erosion in scrap prices, and the spread may have a chance of widening.

HRC premium as a percentage

The chart on the right-hand side below shows the spread relationship differently: We have graphed HRC’s premium over busheling scrap as a percentage. HRC prices now have a 99% premium over prime scrap, even with a month ago.

Ethan Bernard

Read more from Ethan Bernard