Prices

May 29, 2025

HR Futures: Caution prevailing in the market

Written by Gaby Ain

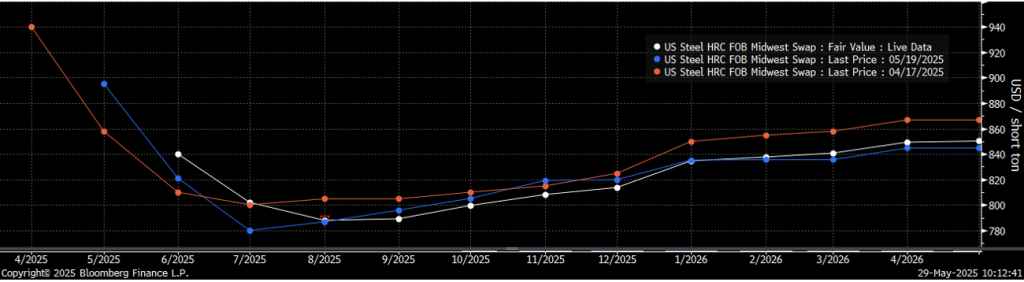

The evolution of the US hot-rolled coil (HRC) futures curve since my last update on April 17 tells a familiar story: fleeting optimism giving way to renewed caution. What then felt like a market at a crossroads now feels more like one still suspended in a state of in between, as outlooks begin to firm and sentiment recalibrates.

Back on April 17, the curve (orange) reflected caution. Prices bottomed near $800 and climbed modestly through Q4 and into 2026. The tone was, “The bleeding has stopped … maybe we stabilize.”

A month later, on May 19, sentiment had improved. The curve (blue) officially slipped into contango starting in July, with front-month contracts lifting and participants beginning to price in a potential H2 recovery. But that optimism didn’t last long.

As of May 29, the curve (white) has flattened back to something resembling the April shape. Near-term prices softened, and longer-dated contracts were trimmed, as expectations for a durable structural floor weakened. The tone has shifted once again, “Actually … let’s not get ahead of ourselves.” The market is back to weighing short-term softness against longer-term structure, still waiting for a catalyst.

CME Midwest HRC futures curve (May 29 in white, May 19 in blue, April 17 in orange)

During this time, the slow pace of activity has allowed space for narratives to take shape. On the more optimistic side, some point to the 25% steel tariffs as a price backstop, mill discipline as a buffer against oversupply, and subdued imports as an ongoing constraint. June scrap, once forecast to decline by $10–30, has been revised to “strong sideways.” That confluence has helped revive the idea that $800 may represent a reliable floor.

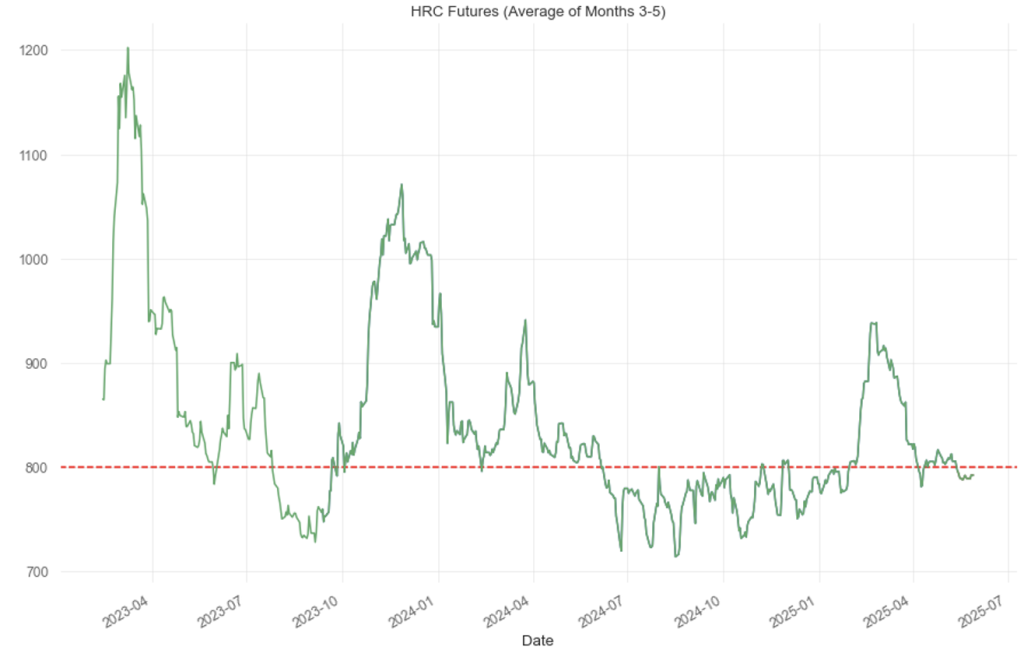

And where has this $800 “floor” come from? Sometimes the simplest answer is the right one. Historically, as shown in the chart above, there’s been clear stickiness around that level. The futures market has hovered near $800 not because of some technical trigger, but because it often does… until it doesn’t.

Around this time last year, prices were drifting lower, yet few were willing to sell the curve below $800. It took a series of mill-led price hikes and a wave of optimism to push it back toward $900. A similar setup unfolded in early 2024. Once again, the market hesitated below $800 until physical spot levels forced its hand. Then, on a single CRU print that was widely viewed as the bottom, futures quickly rallied to $950.

In both instances, sellers only stepped in below $800 once the physical market had already moved there. The same dynamic appears on the upside. While technicals rarely stick in US HRC, $800 has become the rare exception, a psychological anchor.

With the physical market holding up better than many expected, evident in how June and July futures (white curve in first chart) have resisted a full collapse, traders may simply need to stay patient. If a positive demand narrative takes hold, history shows futures can reprice aggressively. In short: the move is coming. The only question is whether we crash through $800 or bounce firmly off it.

Which leads us to the more bearish case, the setup for a sharper repricing event, a crash through. Shrinking mill lead times, which have fallen to roughly four weeks, are raising questions about underlying demand. The seasonal summer slowdown is approaching, and spot market activity remains subdued, making it difficult to say whether current futures pricing is defensible or overly optimistic. The result is a futures curve that continues to reflect caution, not conviction.

This round trip doesn’t signal collapse, but it does highlight hesitation. The market isn’t pricing in a crash. It’s drifting, still unsure of its next move. Each curve update reopens the same question: was Q1 strength the start of something lasting, or just a temporary overshoot? For now, all eyes remain on the $800 level as that’s most likely where we will find out.

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Capital Markets should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.