Market Data

June 3, 2025

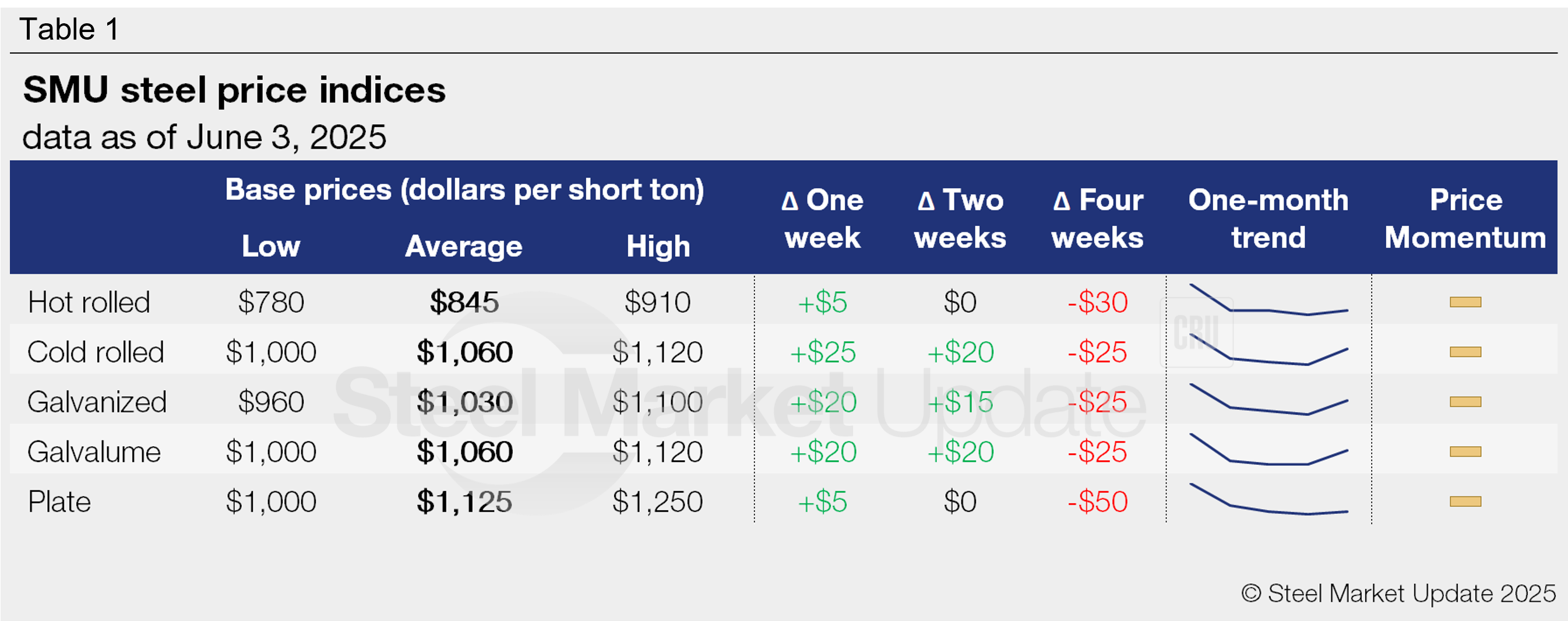

SMU Price Ranges: Marginal uptick in steel prices following tariff announcement

Written by Brett Linton

Following eight consecutive weeks of declines, sheet and plate prices saw some upward movement this week in the wake of last Friday’s Section 232 tariff increase announcement. Gains varied by product.

Hot-rolled coil (HRC) prices inched up $5 per short ton (st) this week, recovering from a three-month low. Plate prices also ticked higher, rising $5/st from last week.

Cold-rolled and coated products saw larger gains this week, all rebounding to four-week highs. Our cold rolled index jumped $25/st week over week (w/w), while our galvanized and Galvalume indices both increased $20/st.

In light of this, SMU’s price momentum indicator has been adjusted from Lower to Neutral for all sheet and plate products, signaling that we see no clear direction for prices over the next 30 days.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $780-$910/st, averaging $845/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is up $10/st. Our overall average is up $5/st w/w. Our price momentum indicator for hot-rolled steel has been adjusted to Neutral, meaning we see no clear direction for prices over the next 30 days.

Hot rolled lead times range from 3-6 weeks, averaging 4.2 weeks as of our May 29 market survey.

Cold-rolled coil

The SMU price range is $1,000–$1,120/st, averaging $1,060/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is up $30/st. Our overall average is up $25/st w/w. Our price momentum indicator for cold-rolled steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Cold rolled lead times range from 5-8 weeks, averaging 6.0 weeks through our latest survey.

Galvanized coil

The SMU price range is $960–$1,100/st, averaging $1,030/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is up $40/st. Our overall average is up $20/st w/w. Our price momentum indicator for galvanized steel has been adjusted to Neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,057–1,197/st, averaging $1,127/st FOB mill, east of the Rockies.

Galvanized lead times range from 4-7 weeks, averaging 5.7 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,000–$1,120/st, averaging $1,060/st FOB mill, east of the Rockies. The lower end of our range is up $10/st w/w, while the top end is up $30/st. Our overall average is up $20/st w/w. Our price momentum indicator for Galvalume steel has been adjusted to Neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,294–1,414/st, averaging $1,354/st FOB mill, east of the Rockies.

Galvalume lead times range from 5-7 weeks, averaging 5.9 weeks through our latest survey.

Plate

The SMU price range is $1,000–$1,250/st, averaging $1,125/st FOB mill. The lower end of our range is up $10/st w/w, while the top end is unchanged. Our overall average is up $5/st w/w. Our price momentum indicator for plate has been adjusted to Neutral, meaning we see no clear direction for prices over the next 30 days.

Plate lead times range from 4-7 weeks, averaging 5.2 weeks through our latest survey.

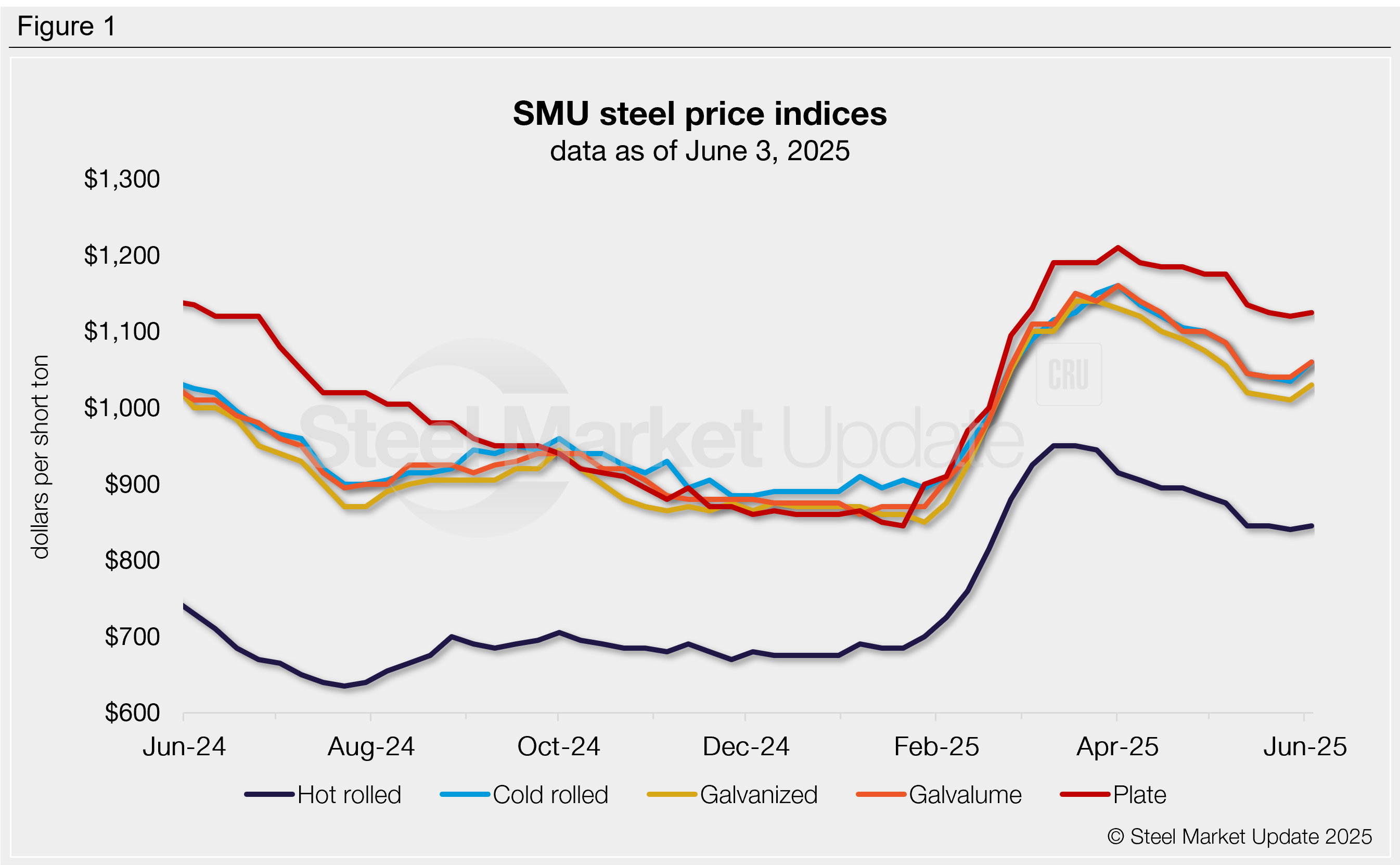

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.