Market Data

July 1, 2025

SMU Price Ranges: Sheet and plate steady ahead of Independence Day

Written by David Schollaert & Michael Cowden

Sheet and plate prices were little changed in the shortened week ahead of Independence Day, according to SMU’s latest check of the market.

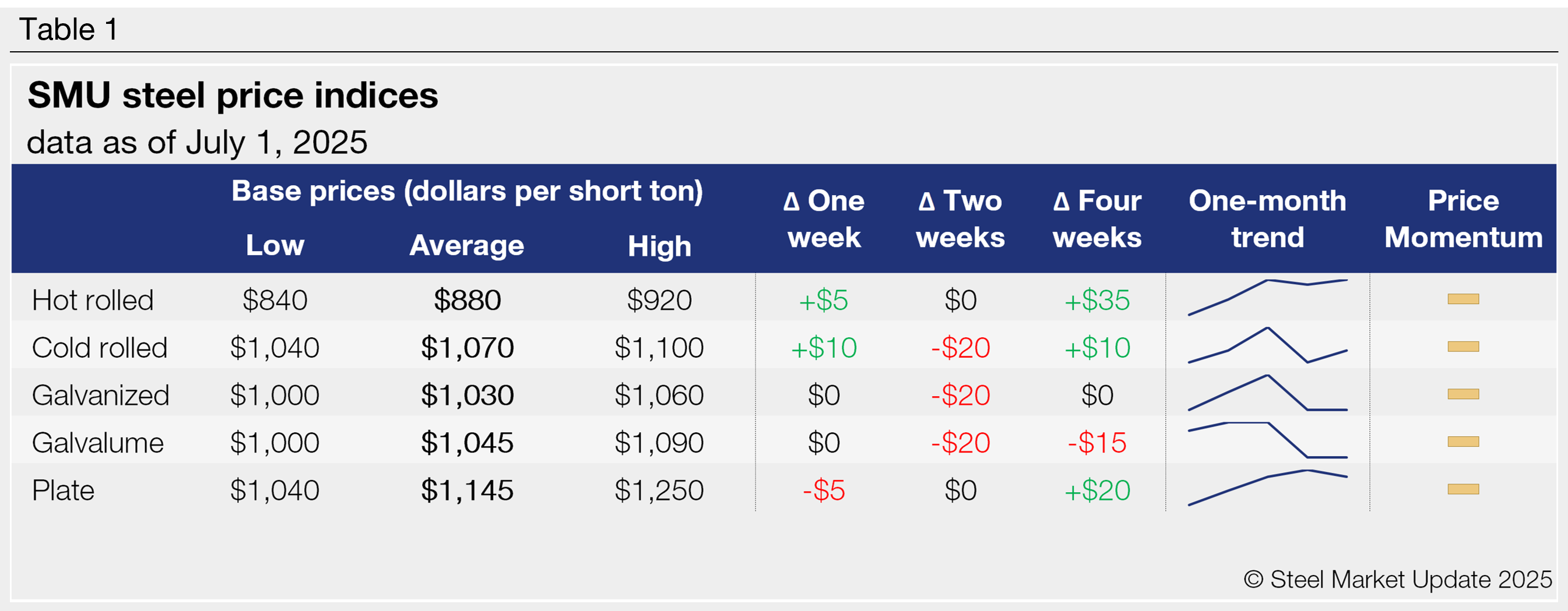

SMU’s hot-rolled (HR) coil price inched up $5 per short ton (st) to $880/st on average this week. Prices for other products were also little changed week over week (w/w).

Our cold-rolled (CR) coil price stands at $1,070/st on average, up $10/st vs. last week. Galvanized base prices are unchanged at $1,030/st on average, and Galvalume base prices were flat at $1,045/st. Plate, meanwhile, dipped to $1,145/st on average, off $5/st from last week.

If there was a change, it was that some of our price ranges consolidated in a tighter band compared to prior weeks – with modestly higher lows and somewhat lower highs.

Our price indicators for all sheet and plate products remain at neutral.

What they’re saying

Market participants generally characterized the market as quiet ahead of July 4. And more than a few noted that they were already on vacation.

A producer source said his company has gotten more orders this week without the discounting that pervaded prior weeks. He said it could be a sign that inventories continue to move lower.

A service center source said his company has been buying only as needed as it tries to tune out the noise around emotional issues such as the Big Beautiful Bill, tariffs, and tensions in the Middle East.

Both agreed that volumes were lower than they would be during a non-holiday week.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $840-920/st, averaging $880/st FOB mill, east of the Rockies. The lower end of our range is up $10/st w/w, while the top end is unchanged. Our overall average is up $5/st w/w. Our price momentum indicator for hot-rolled steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Hot rolled lead times range from 3-6 weeks, averaging 4.4 weeks as of our June 26 market survey. We will publish updated lead times next Thursday.

Cold-rolled coil

The SMU price range is $1,040–1,100/st, averaging $1,070/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is flat. Our overall average is up $10/st w/w. Our price momentum indicator for cold-rolled has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Cold rolled lead times range from 4-9 weeks, averaging 6.2 weeks through our latest survey.

Galvanized coil

The SMU price range is $1,000–1,060/st, averaging $1,030/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is down $20/st. Our overall average is flat w/w. Our price momentum indicator for galvanized steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,078–1,138/st, averaging $1,108/st FOB mill, east of the Rockies.

Galvanized lead times range from 4-8 weeks, averaging 6.0 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,000–1,090/st, averaging $1,045/st FOB mill, east of the Rockies. The lower end and the top end of our range flat w/w. Our overall average is unchanged w/w as a result. Our price momentum indicator for Galvalume steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,268–1,358/st, averaging $1,313/st FOB mill, east of the Rockies.

Galvalume lead times range from 4-8 weeks, averaging 6.2 weeks through our latest survey.

Plate

The SMU price range is $1,040–1,250/st, averaging $1,145/st FOB mill. The lower end of our range is flat w/w, while the top end is down $10/st. Our overall average is down $5/st w/w. Our price momentum indicator for plate has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Plate lead times range from 4-8 weeks, averaging 5.6 weeks through our latest survey.

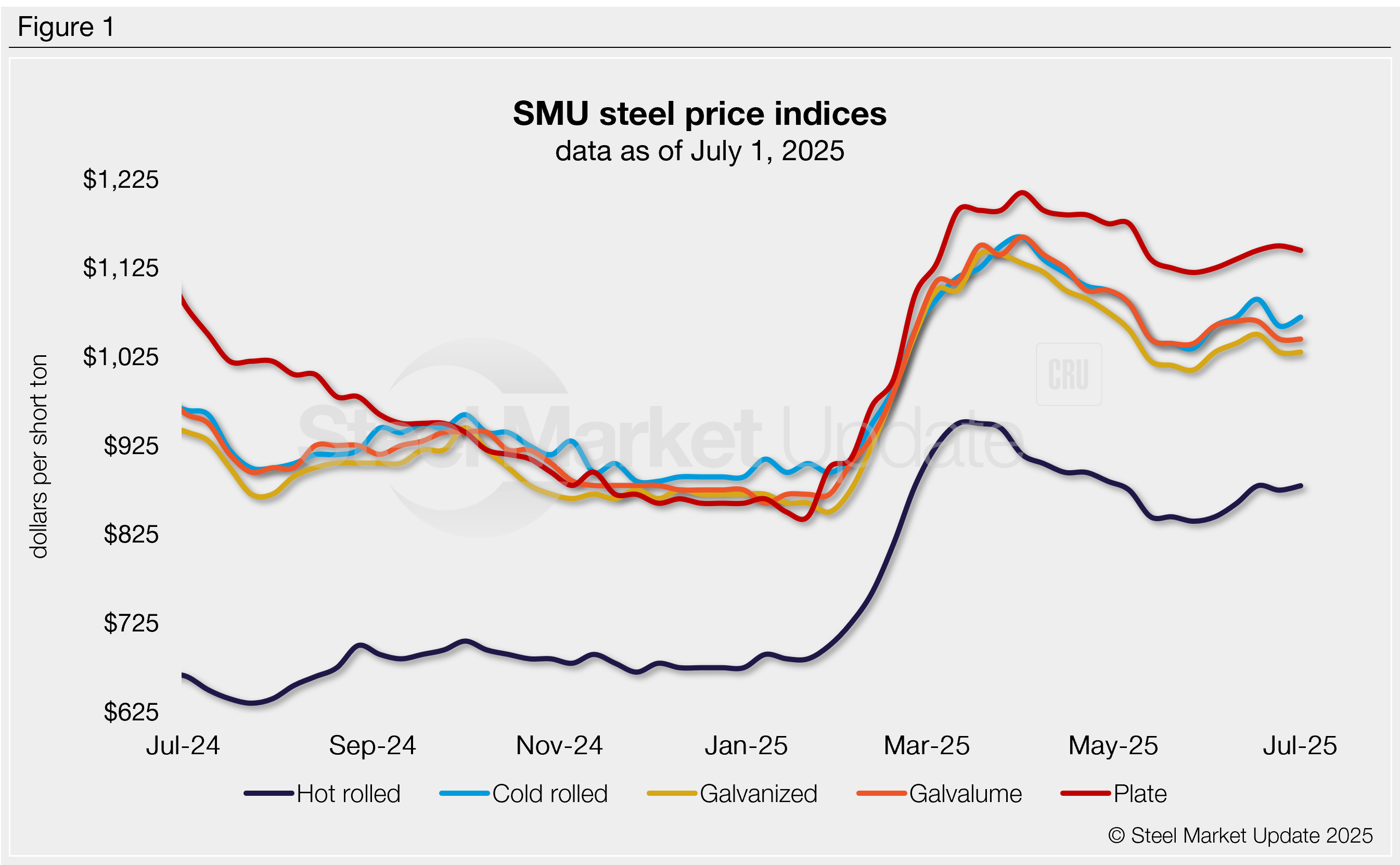

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert