Market Data

July 10, 2025

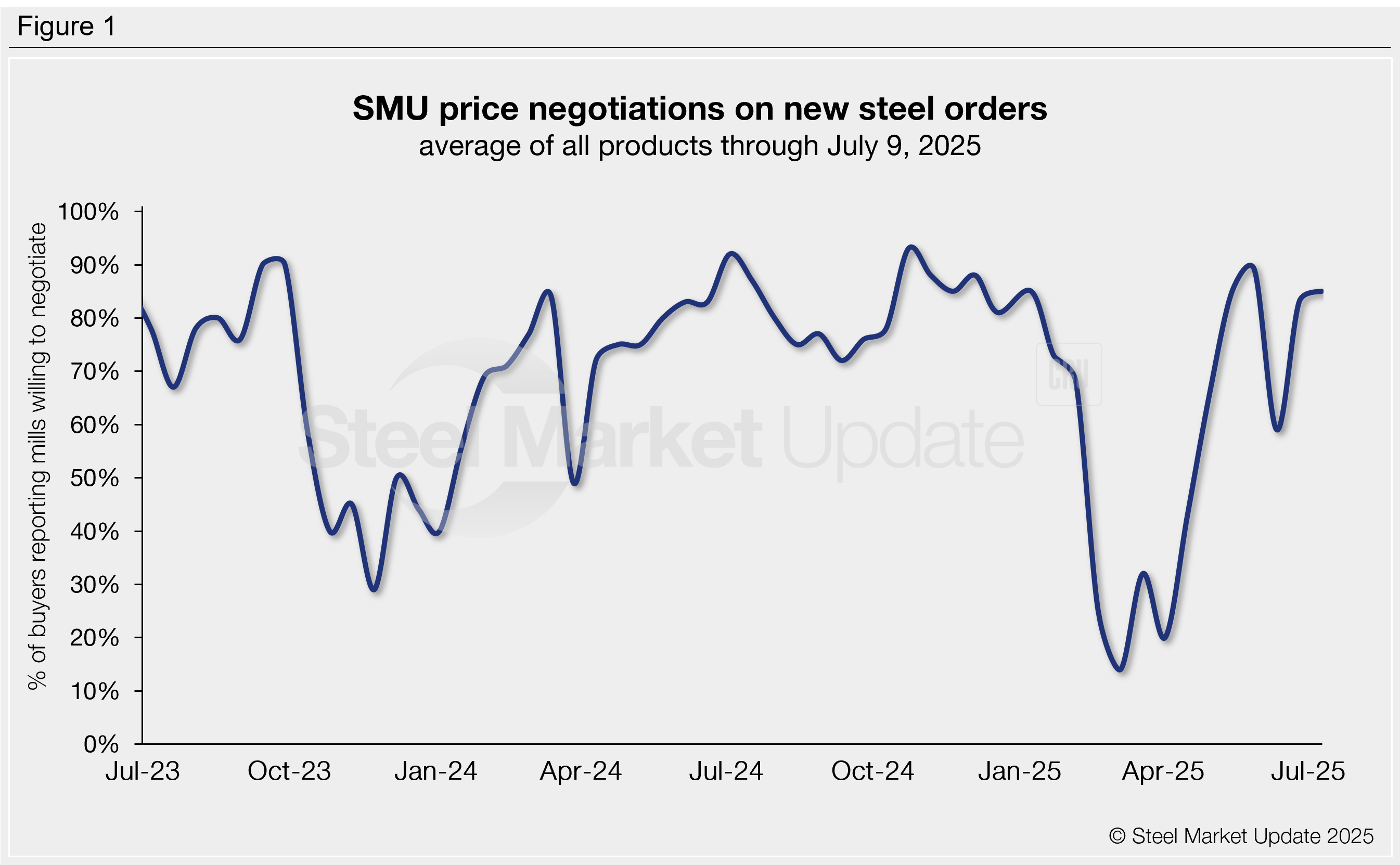

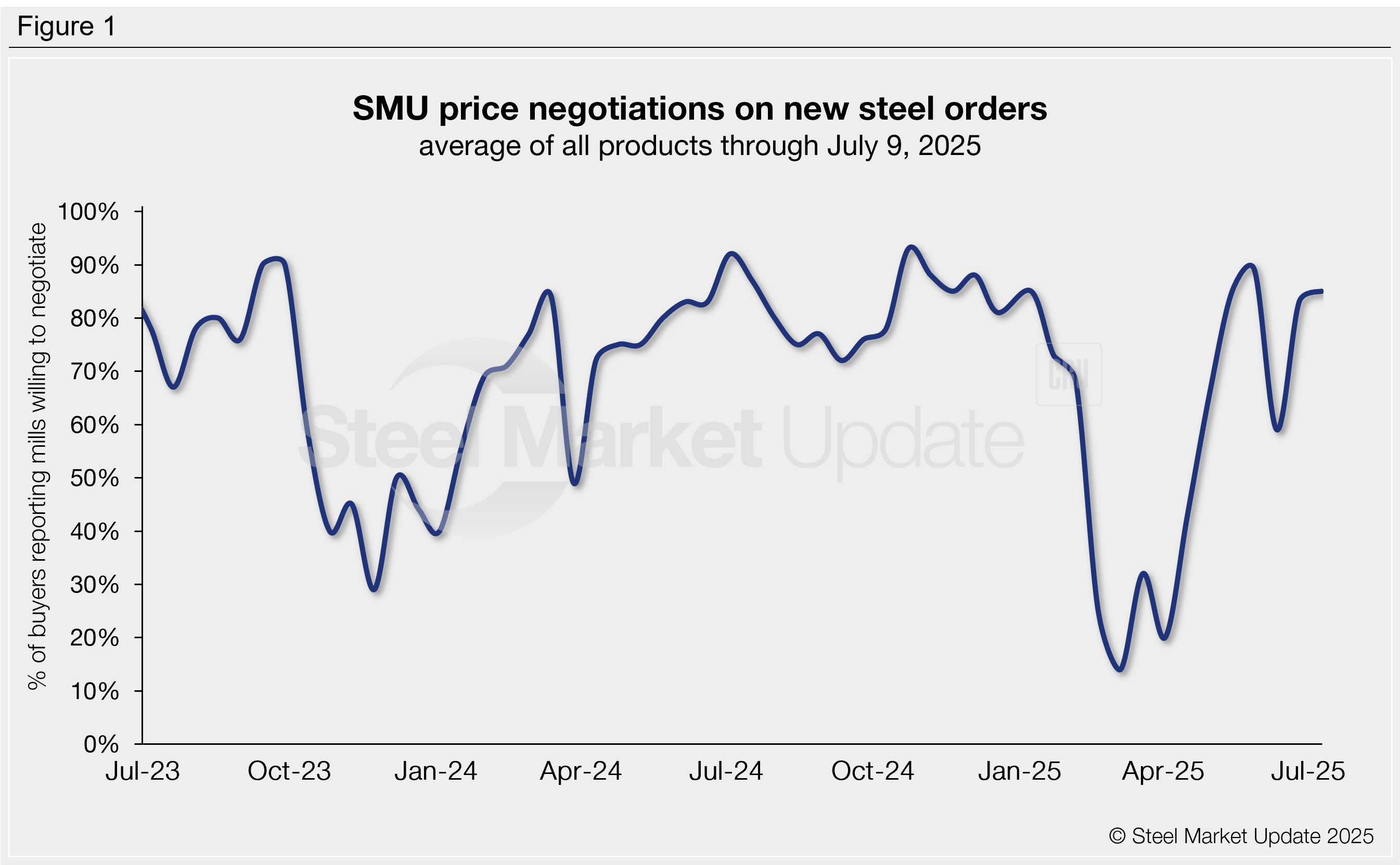

SMU Survey: Mill willingness to negotiate remains high

Written by Brett Linton

Domestic mills are more open to talk price on new orders than they were in June, according to most steel buyers responding to our market survey this week. Negotiation rates have recovered from the early-June lull and are now just a few percentage points shy of the high levels seen late last year.

The uptick in price flexibility over the past month marks a notable shift from the firmer stance mills held earlier this year when tariff headlines pushed the market higher. That leverage shifted back to buyers in April and May as negotiation rates climbed to multi-month highs. In early June, we saw mills briefly regain control amid renewed tariff headlines, but that power has since swung back to buyers.

Every other week, SMU surveys thousands of buyers asking if domestic mills are negotiable on new spot order pricing. This week, 85% of respondents said mills were willing to negotiate, up from 83% in our last survey and 59% one month ago (Figure 1).

Negotiation rates by product

Negotiation rates rose this week for two of the four sheet products we track, with all holding near some of the highest rates recorded this year. Plate rates have remained historically strong for six straight weeks (Figure 2). Current rates are:

- Hot rolled: 87% of buyers said mills are negotiable on price, up three percentage points from two weeks ago. For comparison, the highest rate this year was 94% in late May.

- Cold rolled: 83%, up 11 points. This is tied with late-May peak for an eight-month high.

- Galvanized: 82%, down one point (highest this year was 90% in January).

- Galvalume: 80%, down seven points (2025 max was 92% in late-May).

- Plate: holding steady at 100% for the second-consecutive survey.

Steel buyer remarks:

“Mills will deal if there is volume behind the order.”

“Some [on sheet] depending on volume.”

“Yes [on hot rolled] if you are willing to place significant (2,000+) tons.”

“Negotiable with substantial [plate] tons.”

Note: SMU surveys active steel buyers every other week to gauge their steel suppliers’ willingness to negotiate new order prices. The results reflect current steel demand and changing spot pricing trends. Visit our website to see an interactive history of our steel mill negotiations data.