Mexico

July 31, 2025

HR Futures: Market blues turn bearish

Written by Gaby Ain

The cautious neutrality and summertime blues we discussed just a few weeks ago have evolved into something decidedly more bearish. With little movement in tariff negotiations between the US, Mexico, and Canada, exemplified by this morning’s announcement of a 90-day extension on the existing US Mexico trade deal, and lukewarm fundamentals in the physical market, participants have increasingly positioned for softer prices. Recent shifts in both the futures curve and speculative positioning confirm the cautious tone in early July has given way to clearer bearish conviction.

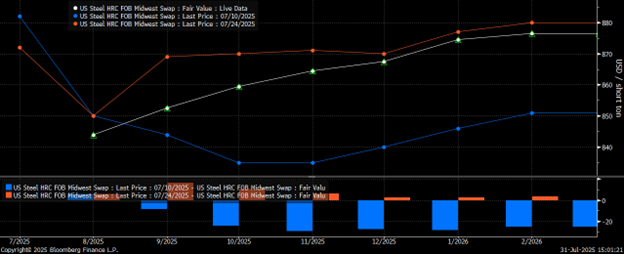

CME Midwest HRC futures curve (July 31 in white, July 24 in orange, July 10 in blue)

Looking closely at the futures, sentiment has undeniably shifted downward as shown in the chart above. Compared to July 10 (blue), when the curve displayed backwardation, the “cliff-edge” has notably morphed. By July 24 (orange), a week ago, the curve had shifted to a mild contango.

Today’s curve (July 31, white) underscores continued price erosion in near-term months (August through November), signaling skepticism around demand recovery and diminished concerns about near-term supply tightness. Rather than wild swings, volatility has gradually been “bled off” as uncertainty, an environment we’ve become familiar with, narrows and the market edged toward consensus.

Despite the softer front-end pricing, longer-term contracts into 2026 remain relatively stable, suggesting market participants anticipate longer-term structural support, even as short-term confidence wanes.

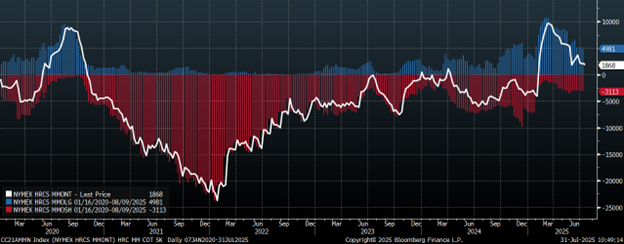

CME HRC Money-Manager Positioning

Money manager positioning further validates the bearish pivot in market sentiment.

The latest data illustrates a continued decline in speculative net length, now notably lower than the cautiously neutral positions held earlier in the summer. Notably, gross short positions continue to rise, reflecting a clear and deliberate increase in bearish bets or defensive hedging.

Concurrently, long positions continue their steady liquidation, indicating fading optimism and cautious sentiment about near-term pricing momentum. Together, these trends make clear an increasing skepticism of a near-term recovery, aligning closely with recent pricing movements on the futures curve.

Fundamentally, market conditions remain tepid. Nucor’s CSP price held steady at $900 per short ton (st), while lead times have shortened. This reflects ongoing lukewarm demand. Import arrivals are coming in at their lowest levels since January 2021. Yet, seemingly, no immediate supply tightness has emerged, reinforcing perceptions of underlying demand weakness and limiting potential upward momentum.

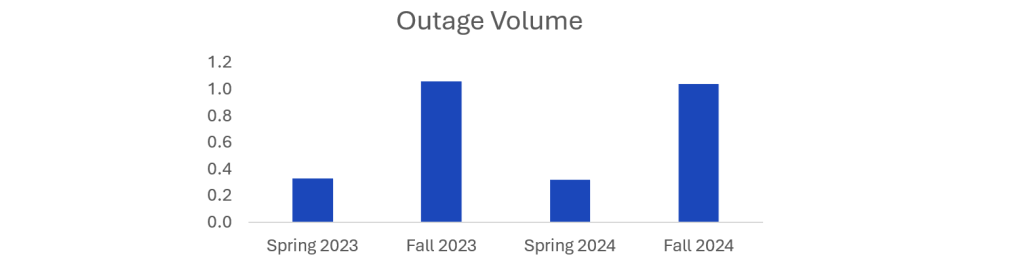

Nevertheless, the approaching end of the summer lull typically marks a seasonal turning point for demand. As summer transitions into fall, we enter into a planned outage season, which is traditionally larger than the spring outage season as shown in the chart below.

This combination, depending on how strongly seasonal demand materializes following the dog days of summer, will be crucial in determining if this bearish sentiment persists.

Overall, historical patterns remind us that periods of market calm rarely linger for too long. The current state could quickly give way to renewed volatility upon meaningful tariff-related news or shifts in fundamentals.

The forward curve has been through a lot this July. Until another catalyst comes along, the market will likely remain rangebound. With the fall season just around the corner, let’s hope the summer lethargy shakes off. After all, in the steel market, clarity often arrives quickly, and volatility is rarely far behind.

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Capital Markets should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.