Market Data

August 19, 2025

SMU Price Ranges: Flat-rolled balloon continues to leak

Written by David Schollaert & Michael Cowden

Sheet and plate prices were flat or down again this week on lower mill pricing, continued concerns about demand, and comparatively high production rates among US mills.

Some sources speculated that a new round of downstream tariffs and the potential for lower interest rates could lead to better future demand. But few saw any short-term catalyst for better order entry.

By the numbers

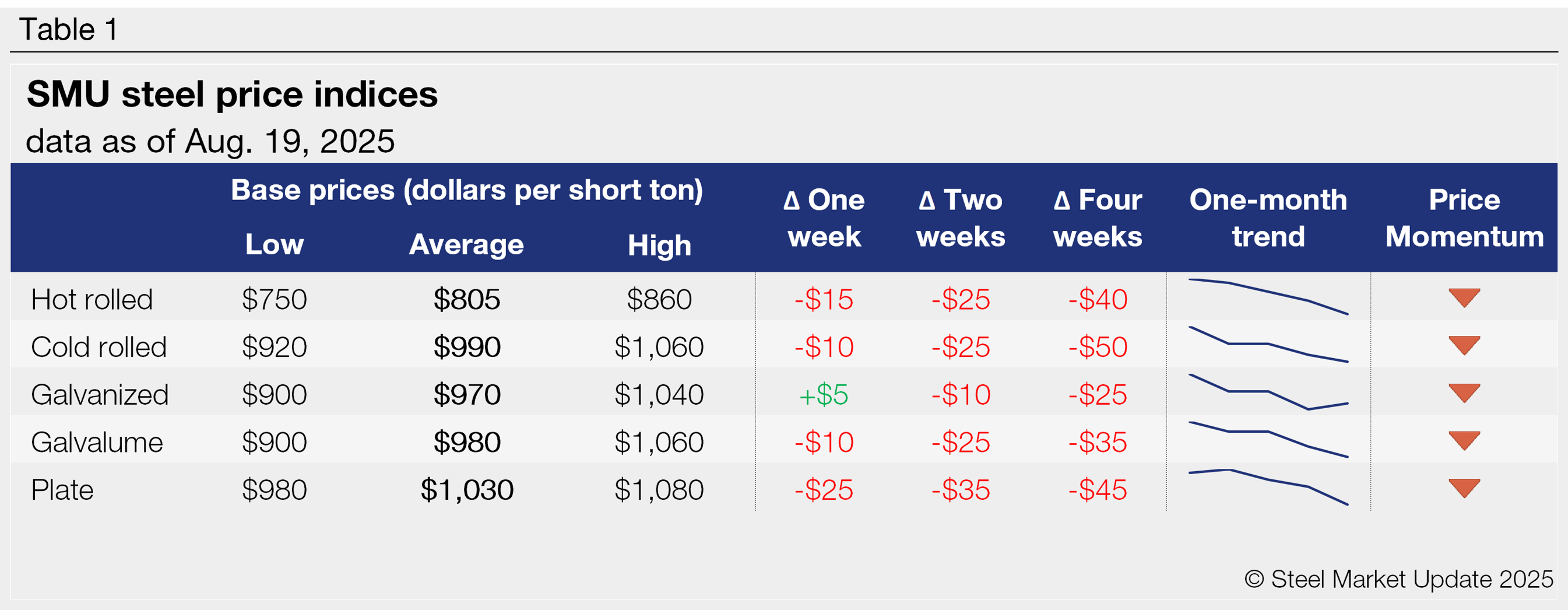

SMU’s hot-rolled (HR) coil price fell to $805 per short ton (st) on average, down $15/st from last week and down $50/st from last month. That figure also marks the lowest point for HR prices since early February, according to SMU’s pricing archives. That’s notable because it’s before blanket Section 232 tariffs of 25% went into effect.

It was a similar story with cold-rolled (CR) coil prices, which dipped to $990/st on average. That’s down $10/st from last week and down $60/st from last month. It also marks the lowest point for CR tags since mid-February.

Galvanized price, meanwhile, were at $970/st on average, little changed from a week ago. And Galvalume stands at $980/st on average, down $10/st from last week.

Plate prices dropped a more significant $25/st to $1,030/st on average. That marks the lowest point for plate prices since $1,000/st in mid-February.

What they’re saying

Many market participants had expected prices to improve as lead times stretched into September, when the market typically sees a seasonal uptick in activity just as fall outages come into play.

But some sources said that outages (estimated to impact approximately 630,000 st) aren’t as widespread this fall because mills had already pulled forward some of that work into their spring outages.

There had also been expectations earlier this summer that raw materials could rise sharply in September on a potential 50% tariff on Brazilian pig iron. In the end, while tariffs on other Brazilian exports shot higher, the tariff on pig iron remained at 10%. And sources said some mills had bought ahead of the higher potential tariff, which could lead to a metallics overhang and scrap prices being flat or lower in September.

Meanwhile, some expressed frustration with foreign mills “selling through” the 50% tariff – which they said had resulted in more import pressure than anticipated.

Still, other market participants think the market could be closer to a bottom than the consensus might assume.

Those sources said mills running at higher production levels was more an indication of domestic producers replacing imports than of them pouring too much steel into a weak market.

They also contended that import volumes could dry up by the fourth quarter – leaving mills with a stronger hand to increase prices then.

Momentum lower

SMU has for the time being shifted its sheet and plate price momentum indicators from neutral to lower given slow but steady declines this summer, a weaker outlook for raw material prices next month, and evidence that domestic mills continue to compete against each other on price to bring in volume.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $750–860/st, averaging $805/st FOB mill, east of the Rockies. The lower end of our range is down $10.st w/w, while the top end is $20/st lower. Our overall average is $15/st lower w/w. Our price momentum indicator for hot-rolled steel has been adjusted from neutral to lower, meaning we expect prices to decline over the next 30 days.

Hot-rolled lead times range from 3–7 weeks, averaging 4.4 weeks as of our August 7 market survey. We will publish updated lead times on Thursday, Aug. 21.

Cold-rolled coil

The SMU price range is $920–1,060/st, averaging $990/st FOB mill, east of the Rockies. The lower end of our range is flat w/w, while the top end is down $20/st. Our overall average is down $10/st w/w. Our price momentum indicator for cold rolled has been adjusted from neutral to lower, meaning we expect prices to decline over the next 30 days.

Cold-rolled lead times range from 5–8 weeks, averaging 6.2 weeks through our latest survey.

Galvanized coil

The SMU price range is $900–1,040/st, averaging $970/st FOB mill, east of the Rockies. The lower end of our range is up $30/st w/w, while the top end is down $20/st. Our overall average is up $5/st w/w. Our price momentum indicator for galvanized steel has been adjusted from neutral to lower, meaning we expect prices to decline over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $978–1,118/st, averaging $1,048/st FOB mill, east of the Rockies.

Galvanized lead times range from 4–8 weeks, averaging 6.2 weeks through our latest survey.

Galvalume coil

The SMU price range is $900–1,060/st, averaging $980/st FOB mill, east of the Rockies. The lower end of our range is down $20/st w/w, while the top end is flat. Our overall average is down $10/st w/w. Our price momentum indicator for Galvalume steel has been adjusted from neutral to lower, meaning we expect prices to decline over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,168–1,328/st, averaging $1,248/st FOB mill, east of the Rockies.

Galvalume lead times range from 5–8 weeks, averaging 6.3 weeks through our latest survey.

Plate

The SMU price range is $980–1,080/st, averaging $1,030/st FOB mill. The lower end of our range is $10/st higher w/w, while the top end is down $60/st. Our overall average is down $25/st w/w. Our price momentum indicator for the plate has been adjusted from neutral to lower, meaning we expect prices to decline over the next 30 days.

Plate lead times range from 4–7 weeks, averaging 5.1 weeks through our latest survey.

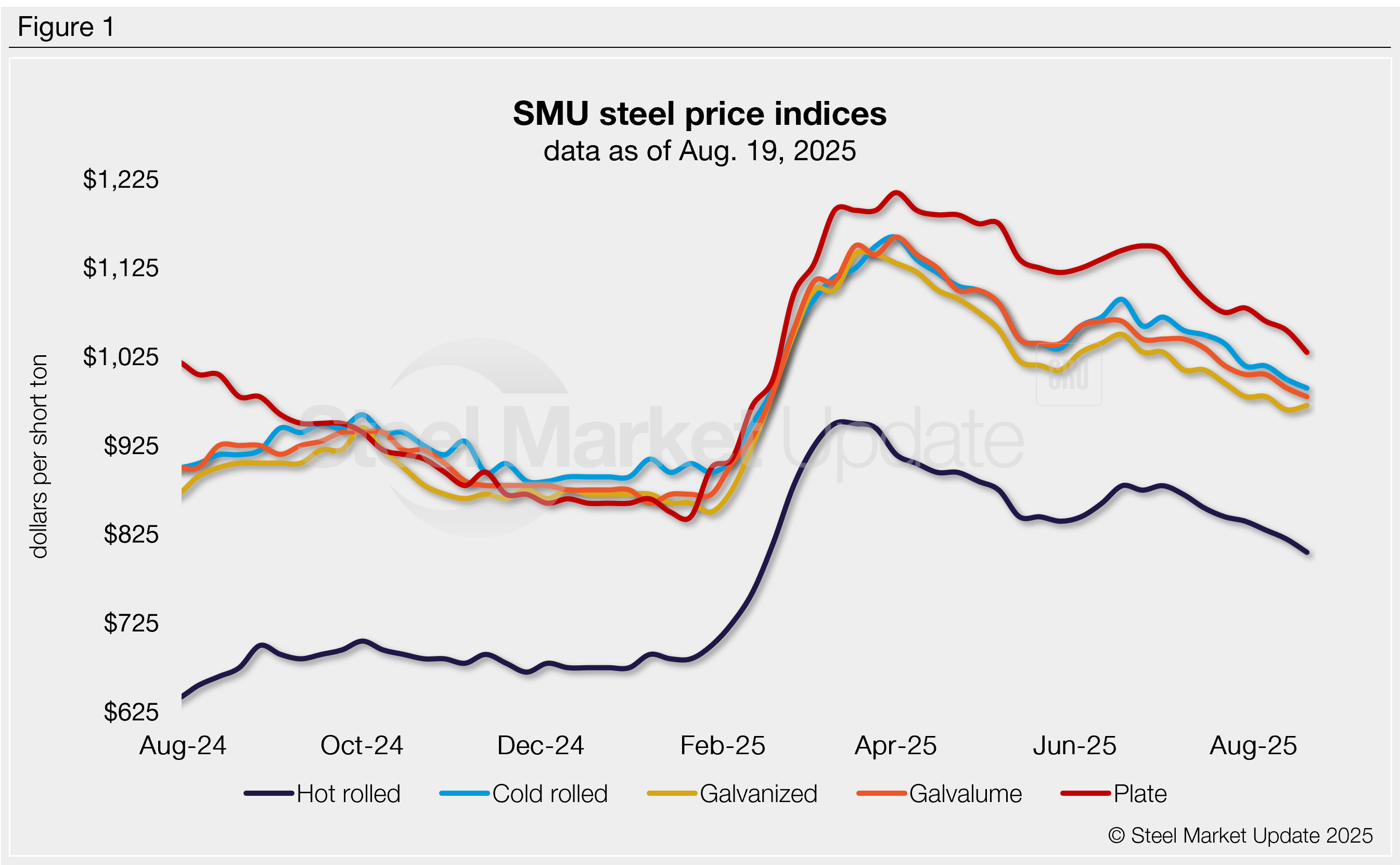

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert