Sheet

August 21, 2025

HR Futures: Forward curve shifts lower, structure maintains

Written by Joshua Toney

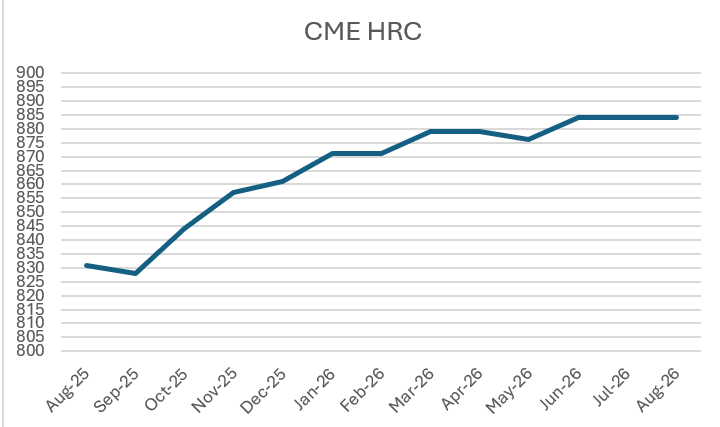

Scraping lower-quartile $800s on nearby futures is bringing limited trading ideas for CME hot-rolled coil (HRC) at present.

The Nucor Consumer Spot Price (CSP) moved down $10 per short ton (st) this week to $865/st. CRU posted at $832/st this week a -$6/st drop week over week. The Index justifies the weakness in Sep’25 futures pricing, and we are witnessing marginal carry expansion with the step lower in front-end pricing.

I’d diagnose this as structural heading into annual contract negotiations at the end of Q4’25. The market loves to keep some semblance of contango. This writer will be curious to see if there are further price action drivers from Cleveland-Cliff’s three-year supply contracts and if last week’s 1.4% decline reported by the American Iron and Steel Institute (AISI) in raw steel output begins a new trend.

Source: CME

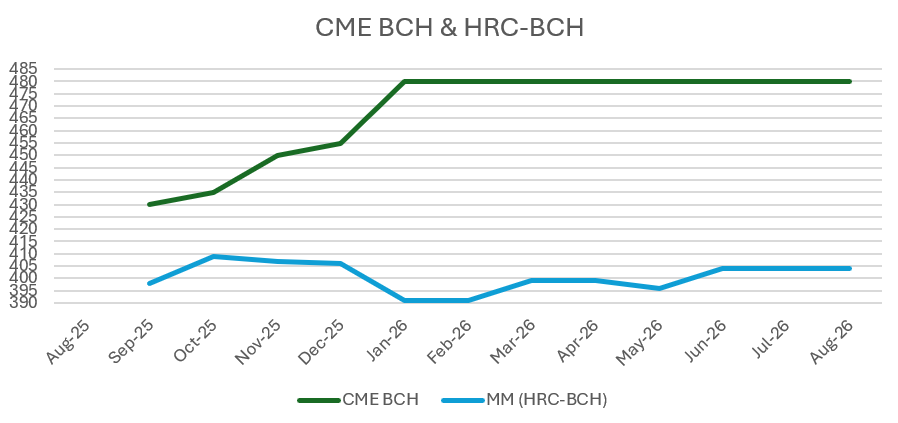

Mill margins imply tightening into Q1’26, which aligns with potential seasonal scrap tightness and inventory declines for end-of-year return on asset calculations. The implication today is that busheling forward velocity is stronger than HRC, which I find difficult to mesh in the current HRC environment of reduced lead times and limited saving grace for exports of ferrous scrap.

CME BCH and HRC-BCH

Source: CME

Market Positioning (CFTC Commitment of Traders):

As of Aug. 12, CFTC reporting, physical participants added 16,940 st to their short positioning. Long positioning grew by 26,500 st. Managed money is sitting net short and added 4,720/st to shorts. Swap dealers are positioned long and added 7,100 st to that net position. Other recordables are roughly balanced.

Source: CFTC Disaggregated Commitments of Traders – Futures Only, Aug. 12, 2025

Disclaimer:

The views and opinions expressed in this column are solely those of the author, Joshua T. Toney, Principal of Corsair Elements LLC. This material is provided for informational and educational purposes only and does not constitute investment, trading, legal, or financial advice. Corsair Elements LLC is not registered with the Commodity Futures Trading Commission (CFTC) or the National Futures Association (NFA). Nothing contained herein constitutes a solicitation or recommendation to buy or sell any commodity interest, futures contract, swap, or other financial instrument. Readers should consult their own professional advisors before making any financial decisions.