Analysis

September 4, 2025

Final Thoughts

Written by Michael Cowden

I’ve been getting some calls lately from some of you who want to kick around ideas on where prices might bottom and when.

In some respects, it’s a nearly impossible market to forecast. A lot hinges, for example, on whether and for how long a 50% Section 232 tariff remains on Canadian steel.

Perhaps no one but President Trump knows the answer to that. (And he might not know the answer until he says it or posts it on social media.)

But in other respects, that leaves ones we’re used to reading – things like demand, imports, and inventory levels.

A few scenarios

Maybe we see a V-shaped recovery if, say, imports drop, demand improves, and everyone restocks at the same time.

Maybe we bounce along a bottom for months, like we did last year – if tariff uncertainty continues to weigh on the market, just as election uncertainty did this time a year ago.

Or perhaps the market still has further to fall before it hits a bottom. Let’s say demand disappoints and competition among domestic mills (with their new capacity) means the marginal import price doesn’t set the bottom for the US market in the way that it typically has.

Trends to watch

While we’re at it, here are some other questions.

Does the low end of our price range – which typically represents prices available to larger buyers – become the prevailing price for all buyers on a lag of a month or so? That’s something you often see in a downward market.

Maybe our price range stabilizes and narrows. That sometimes happens when demand stagnates. Mills keep prices flat, realizing that lower prices won’t bring in more business.

Or maybe we see a sharp drop in prices followed by an equally sharp rebound. When demand improves, an early indication is (somewhat counterintuitively) competition on price. And then once mills have enough volume, lead times can extend and prices can snap back quickly.

Survey says

There is no obvious sign of an inflection point right now. Most mills remain willing to negotiate lower spot prices. And lead times – which some had hoped would extend in the fall – remain mostly unchanged. That suggests more of the same flat or lower prices we saw for much of the summer.

So, what are some other data points to consider? SMU doesn’t do forecasts. But we can provide you with a snapshot of what the current consensus is among the steel buyers we survey.

The data below is a preview of our steel-market survey, the full results of which will be released to our premium subscribers on Friday. (Editor’s note: The numbers on the slides show which pages they’ll be in the deck on Friday. Also, if you’d like to upgrade from executive to premium, contact SMU senior account executive Luis Corona at luis.corona@crugroup.com.)

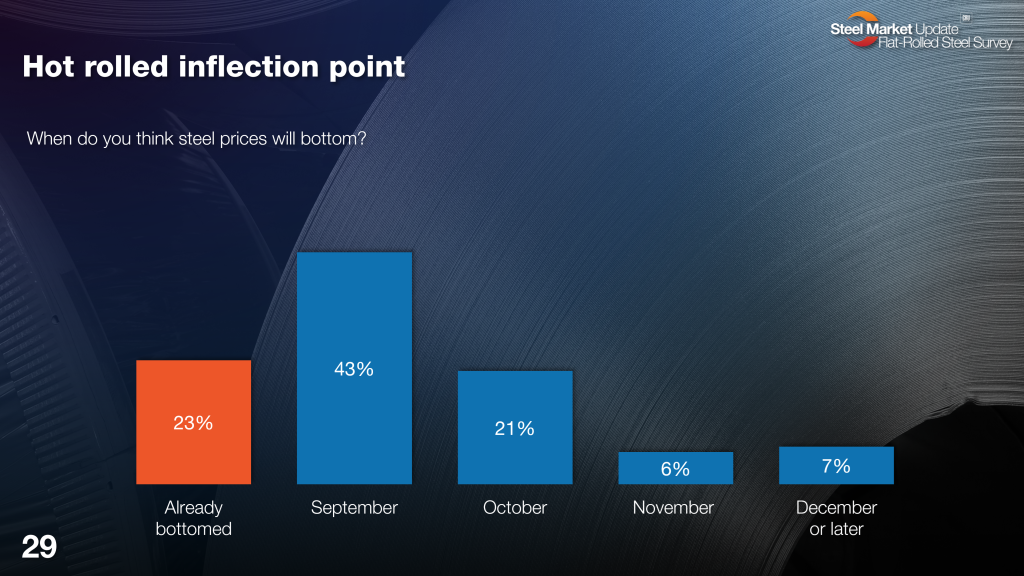

Asked when the hot-rolled (HR) coil market would bottom, here is what respondents to our latest survey thought:

The most common response (43%) was that prices would bottom this month. But significant minorities think prices have already bottomed (23%) or will next month (21%). And more than a few (13%) don’t see prices improving until November, December, or into 2026.

Here is what some of them had to say.

Already bottomed

“Mill outages and low imports will put upward pressure on spot prices.”

“Weak demand is hampering price increases, but they are coming.”

“(Lower prices) won’t drive more business, and players will finally understand this.”

September

“I think tariffs keeping foreign steel prices elevated will keep domestic steel prices from falling much further and within about 5% of where they are now.”

“Close to the bottom, but still a few more weak weeks.”

“Weakness in the plate market, and supply is still good at service centers.”

“Imports lower, tariff uncertainty back on the table, and demand cautious.”

“Will bottom in next 1-2 weeks.”

October

“Back end of outage season and interest rate drops.”

“Bottom of the market will be late October/early November.”

“Demand is still very weak.”

November, December or later

“We still think there is more blood in the water. Demand is just too weak.”

“Even with tariffs, foreign prices are below domestic pricing.”

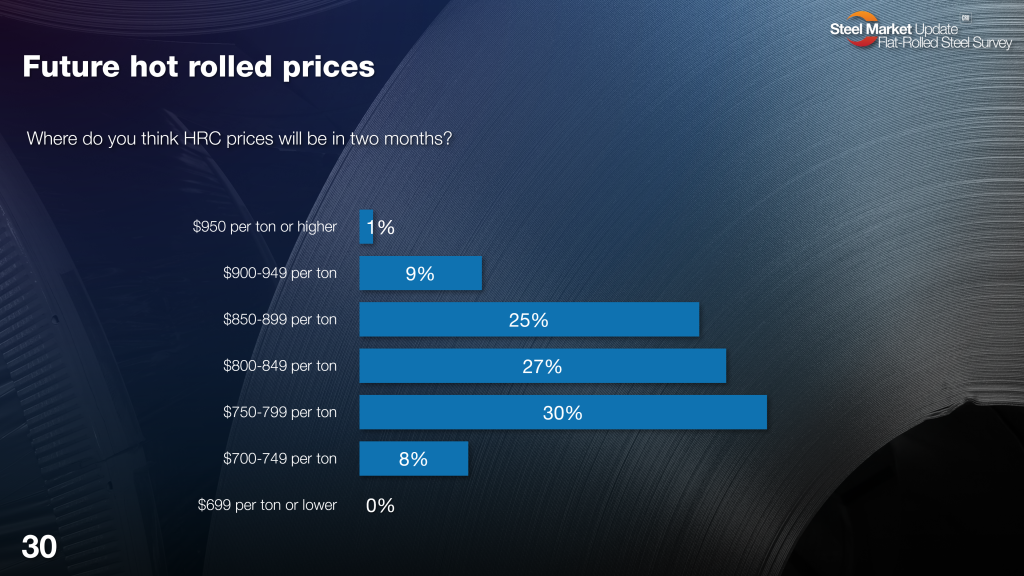

Let’s set the question of when prices will bottom aside for a moment. Where do survey respondents think HR prices will be in early November? Those results are below:

Most (52%) think we’ll be in the $800s per short ton (st), so where we are now or somewhat higher. But a sizeable minority (38%) think we’ll drop into the $700s/st. Very few (10%) see the US HR market climbing back into the $900s/st.

Here is what folks had to say.

$900-949s

“Limited imports and restocking by distributors will spur buying.”

“Restocking, fewer imports – tempered a bit by lax demand.”

$850-899

“Mill outages and low imports will put upward pressure on spot prices.”

“I believe it will go up, but slowly.”

$800-849

“Slow demand keeps prices down. Low imports help keep the price stable. I predict prices will remain flat to soft until 2026.”

“Market uncertainty continues. Tight bandwidth.”

“Market absorbing lack of import and domestic mills will increase prices.”

“Hopefully an end to the summer doldrums, a seasonal pick up in manufacturing, and a little more tariff clarity. Also, a decrease in interest rates will help manufacturing and business activity pick up a bit – and that’ll put a little upward pressure on steel prices.”

“Seems like mills can pull pricing up a bit, but I’m not seeing a runaway market.”

$750-799

“Sept futures already flashing high $700s, and I think there is still downside.”

“No positive impulse, no real additional demand.”

“Not high demand, so mills think they need to lower to get traction.”

“Soft demand.”

“Soft demand, and mills need orders.”

“I’m hearing prices are already there.”

$700-749

“Maybe towards the end of the year (for early ’26 delivery) we see mills get a few more bucks. Until then, it’ll be tough sledding.”

“CRU minus deals are already below $750 per ton.”

“Pricing is falling, and the world market will not allow domestic prices to remain at current levels.”

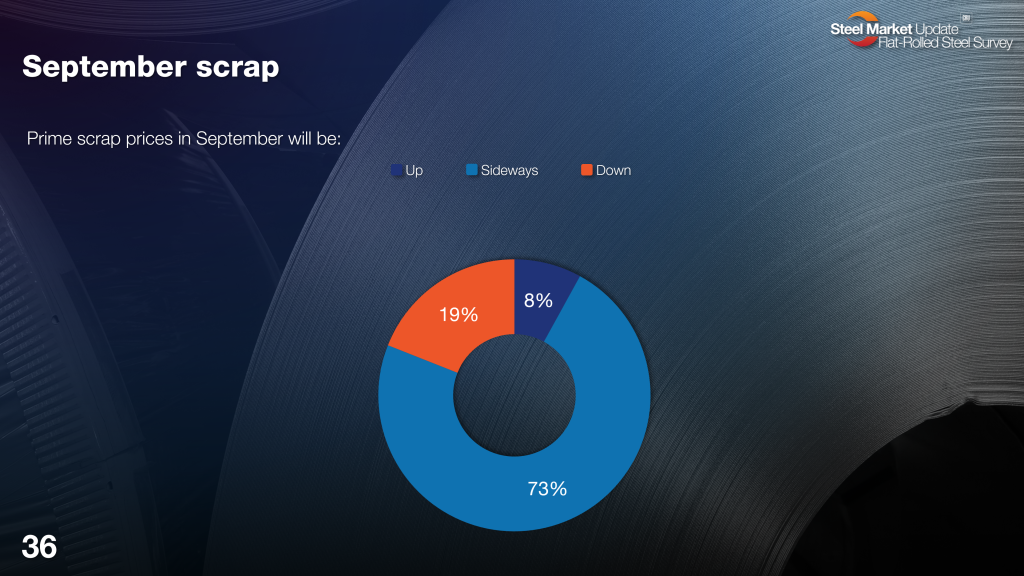

Where prime scrap settles this month of course factors into such projections. So, where do SMU readers think prime will land? Check out the results below:

Most (73%) think prime scrap will be sideways again this month. A significant minority (19%) think it will be down. And only a few (8%) see prime settling higher.

Here is what some of them had to say.

Up

“Seasonal increase in the late fall.”

Sideways

“Opposing forces: demand down but virgin iron units up.”

“Flat to down, we hear.”

Down

“I don’t know anyone on the scrap side who is bullish right now.”

“Prime will be down.”

“Scrap prices preceded steel prices.”

Steel 101

Does what’s above read like Greek to someone you know? That’s OK if it’s your cousin. But it’s not so great if it’s a colleague.

Check out our next Steel 101 if you know anyone who could use an introduction to how steel is made, sold, and priced.

Our next Steel 101 will be Oct. 14-15 in Davenport, Iowa. It will feature a tour of SSAB’s plate mill in Montpelier, Iowa. (We’re happy to be touring a plate mill for the first time in a few years.)

It’s a good, practical course. Students learn how steel is made, and then see it being made – something that really makes the knowledge stick. You can learn more here and register here.

In the meantime, thanks to all of you for your continued support. We really do appreciate it.