Sheet

September 4, 2025

HR Futures: Market finds footing on supply-side mechanics

Written by Gaby Ain

As Labor Day marks the transition into fall, the steel market enters September with a similar sense of change. Supply-side fundamentals are beginning to show signs of restraint: imports are limited, outages loom, and production is capped, setting the stage for a market that feels steady on the surface but still unsettled underneath. The balance leaves pricing stable for now, yet sensitive to the next shift.

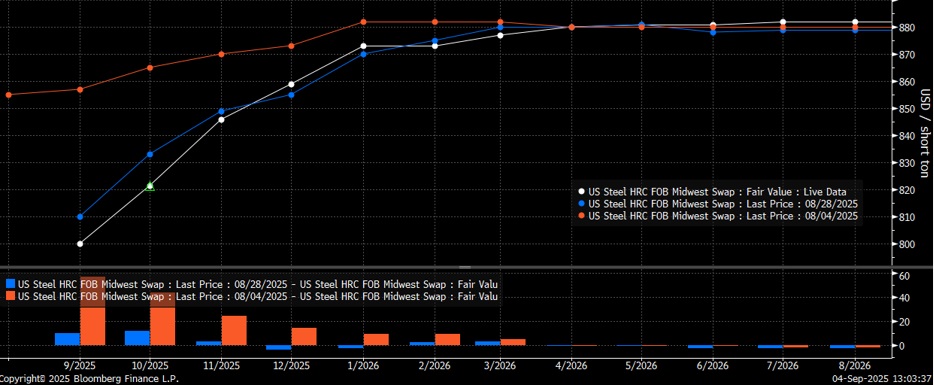

CME Midwest HRC Futures Curve (9/4 in white, 8/28 in blue, 8/4 in orange)

A month ago (Aug. 4, orange), the curve carried a modest upward slope, and by late August (one week ago, blue), that optimism had unwound; nearby contracts had corrected by $20-50/ton. Over the past week, the curve has stabilized. September through December maturities have retraced part of the late-August drop, while out months have flattened around $870-880/ton. The shape underscores a balanced tone: mills have regained some near-term traction, but forward markets remain cautious beyond Q1’26. That caution is underscored by the spread to spot, with the CRU Midwest HRC index at just $809/ton. Rather than a reflection of present demand, the premium resembles an effort to establish a structural floor, anchored by mill discipline, tight imports, and the Q4 outage season.

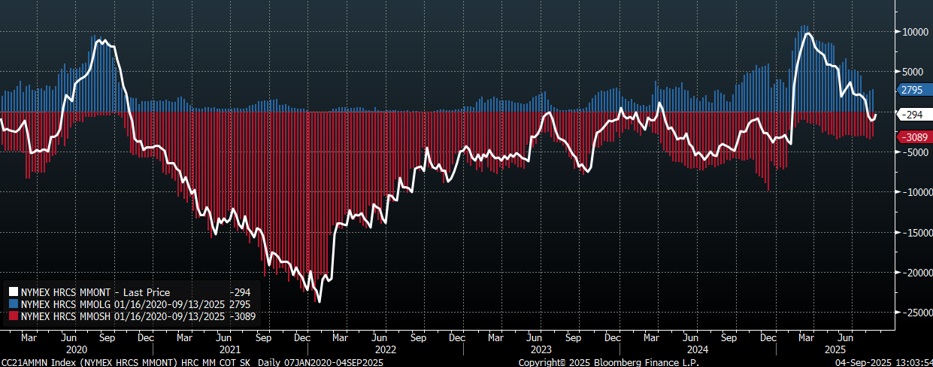

CME HRC Money-Manager Positioning

Speculative positioning reinforces the same theme. Managed money length, which peaked at over 10,000 contracts in Q1, has since been liquidated, leaving net positions essentially flat at -294 contracts. With little speculative length left, downside risk from liquidation is limited, but upside momentum is capped until fresh length comes in. Futures strength, therefore, is less about “hot money” and more about underlying fundamentals.

And fundamentals are beginning to set the stage. Imports have been consistently below the long-run average since February and are trending toward the lowest levels since 2009, closing off external supply pressure. Domestic production remains steady, with capacity utilization just right below 80%. Lead times, after being stagnant for several weeks, are beginning to tick up as mills warn of the outage season. Globally, the narrowing spread between domestic spot and landed prices has curbed import arbitrage, reinforcing support for a floor. On the demand side, however, momentum is lacking. Construction spending has fallen for nine straight months, auto sales remain uneven, and manufacturing still struggles to stay in expansion. These softer demand signals may explain why the back end of the curve has flattened rather than extended higher.

Looking ahead, the new 50% tariff regime remains a variable yet to be fully tested. Futures have only traded under these conditions during the subdued summer period. The historical seasonal pick-up in activity could provide the first real measure of how much these tariffs have shifted the landscape.

Taken together, the futures market has corrected, found its footing, and is leaning more on supply-side mechanics than speculative flows or demand growth. For now. As ever in this market, volatility may not be far away.

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Capital Markets should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.