Analysis

October 5, 2025

Final Thoughts: Survey says edition

Written by Michael Cowden

SMU’s latest steel market survey results indicate that market participants think sheet prices are at or near a bottom. But most also believe there is limited upside once they inflect higher.

Survey respondents attribute the bottom (or anticipated bottom) mostly to limited import volumes and fall maintenance outages at domestic mills – factors that have constrained supply. But anemic demand means that the drop in supply isn’t expected to create any big waves in the market.

However, while most don’t see prices moving sharply higher now, some think there could be more significant upward movement later in Q4, when lead times stretch into Q1 – which is typically a busier time for the steel market.

Anyway, enough from me. Below are some highlights from our survey and comments from our survey respondents. If you’re a ‘premium’ subscriber, you can find the full results here. (The page numbers in the charts below indicate which slide in the survey deck they’re in.)

Also, a bit of shameless self-promotion: If you have an ‘executive’ subscription, data like this is a good reason to consider upgrading to ‘premium’. If you’d like to learn more, ping me at michael@steelmarketupdate.com.

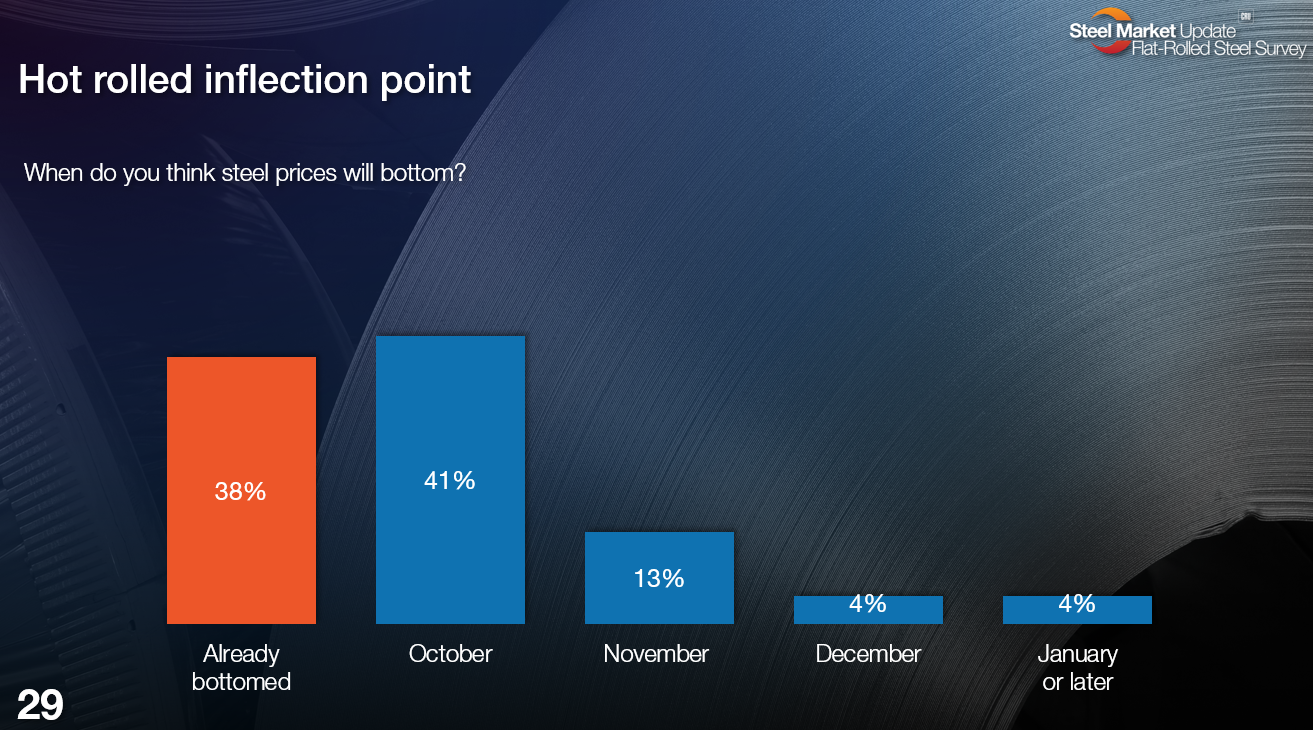

When is the bottom?

As you can see, most people think hot-rolled (HR) prices have already bottomed or will later this month. I’m using HR as a proxy for the rest of the sheet market. If you think, for example, that cold-rolled and coated follow HR on a lag, then you’d want to adjust accordingly from the results below.

That’s the numbers. Here is what some of our survey respondents had to say.

Already bottomed

“Feels like demand is creeping up. And annual maintenance outages may hold pricing where it is or increase it.”

“The bottom came as we flipped the calendar (into October).”

“If we haven’t bottomed yet, I think we’re pretty close.”

October

“Seems like, even though demand has not changed, supply is more constrained than in previous months.”

“Demand is still weak, and supply is good.”

“Weak demand environment.”

“I feel it will be late October or early November – whenever lead times push into 2026. I feel mills will do their best to keep prices from dropping much more. But there is more supply than demand. Once we get into 2026 deliveries, there will be more buying done – and hopefully end-user demand will pick up with more rate reductions.”

November

“We just don’t think the outages are enough to ‘move the needle’ and raise prices.”

“Feels like we are settled in around a fair value price around $800/ton. I anticipate that pricing may decline further to the $750-$800/ton range before increasing leading into Q1.”

“Reduced imports, and stock inventories being drawn down.”

December

“Demand is not there yet.”

January or later

“Tariffs, golden share, too many fingers on too many scales… It’s creating too much uncertainty.”

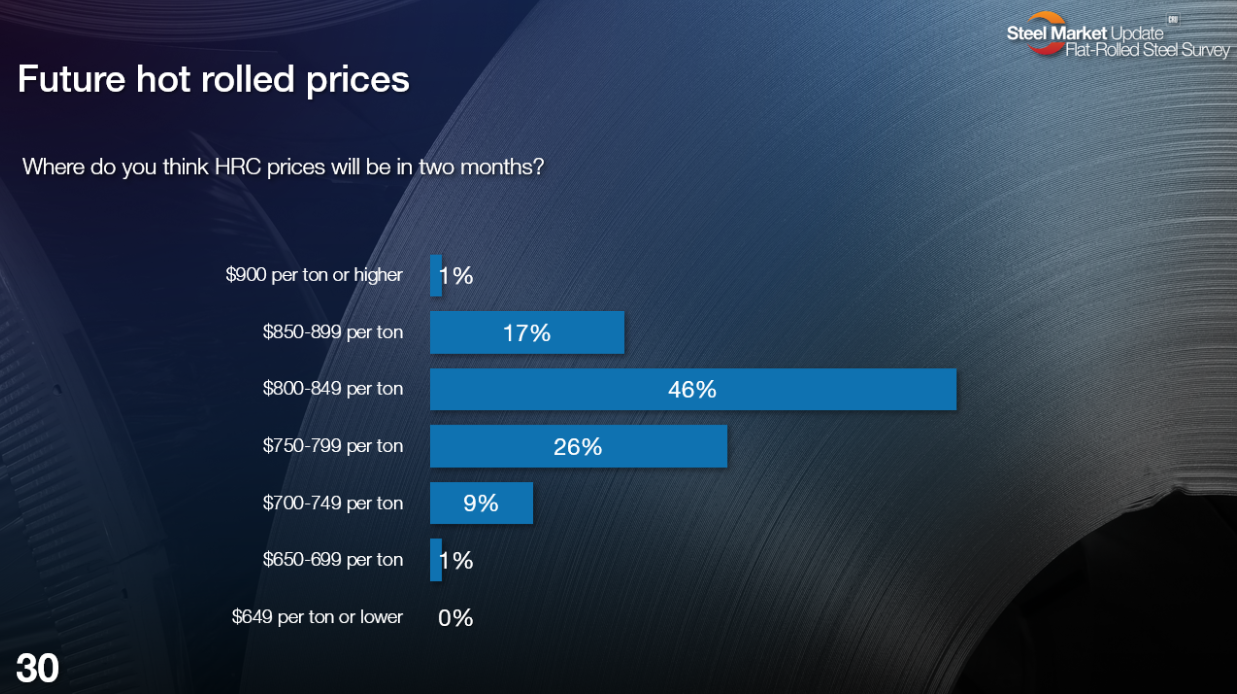

Where is the bottom?

Again, while most people think prices are at or near a bottom, they don’t expect any kind of surge higher like the one we saw in Q1 of this year.

Most respondents (63% of respondents) think HR prices two months from now will be in the $800s/st. Keep in mind that by early December, most lead times should be into 2026. And a significant number (35%) see them remaining in the $700s/st. (SMU’s current HR price stands at $795/st on average. We’ll next update prices on Tuesday evening.)

Here is what survey respondents had to say.

$900/st or higher

“No imports, so domestic mill can do whatever they want.”

$850-899/st

“I think that is the high end, or you start inviting imports back into the country.”

“It’s not demand. It’s the lack of imports. Restocking is required. And there are some shutdowns to help the price go up.”

“Reduced imports. Replacement stock needs to be purchased as prices will have bottomed out soon.”

“Mill outages and decreasing imports.”

$800-849/st

“Market demand will be better and scrap prices will be increasing in two months.”

“Feels like demand is creeping up. And with annual maintenance outages, it may hold pricing where it is or increase it.”

“I believe the market will bottom in four to six weeks and then start a normal cycle back up going in to Q1 – nothing crazy.”

“I just don’t think demand is strong enough to support much of a price increase. And I still think we’re getting at least some foreign steel in, which is helping keep prices low.”

“Lack of imports. Outage effect.”

$750-799/st

“Demand seems to be low, and supply of product is good. Mills are giving very short lead times in last couple of weeks.”

“Soft demand will lead prices down further.”

“Price always dips lower than it should before rebounding.”

“Decent enough market for mills to put through price increases. Scrap should tick up in November.”

“Inventories are low.”

$700-749/st

“Our group is anticipating low $700s during Q4. Demand is just too weak out there.”

“Market demand is still weak.”

“Demand softness.”

“No demand.”

$650-699/st

Editor’s note: The small number of folks who think HR prices will drop back into $600s/st aren’t tipping their hand on why they think that.

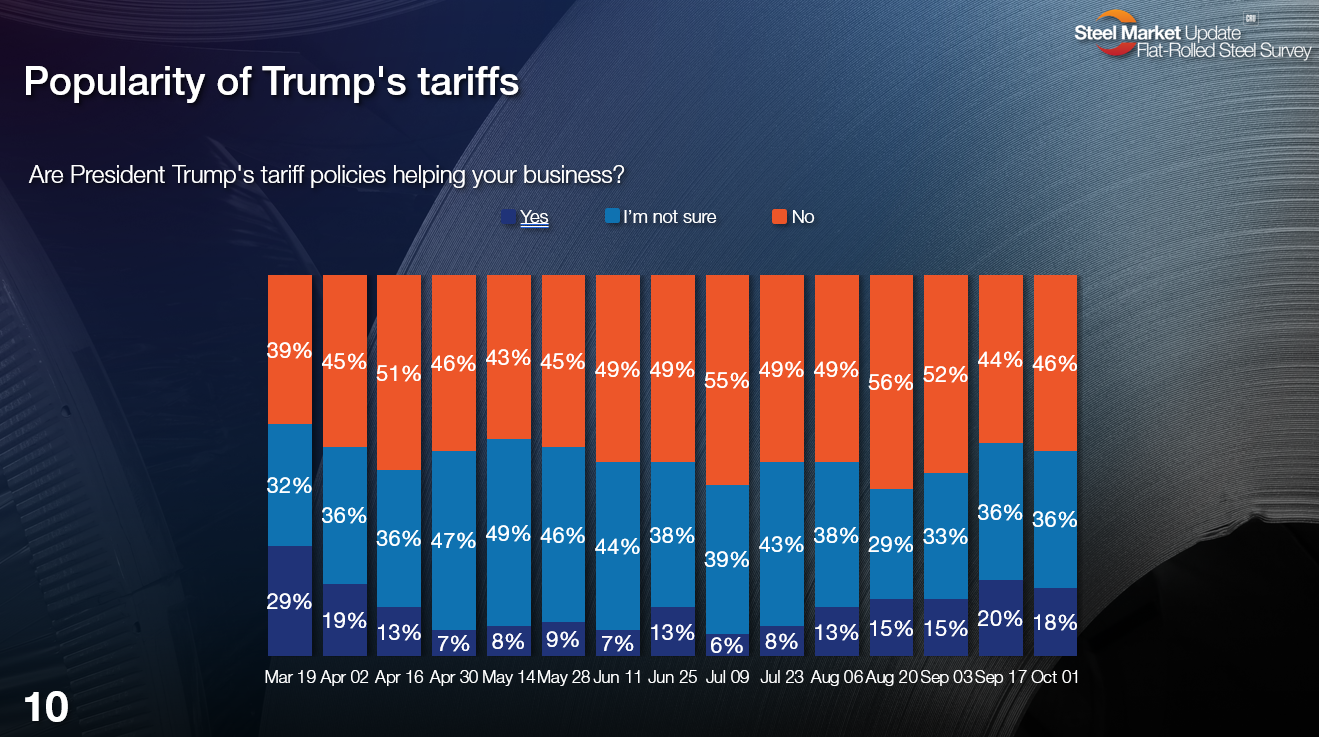

Tariffs remain unpopular

While opinions might differ on prices, one thing has proven remarkably stable since June, when President Trump’s doubling of Section 232 tariffs to 50% went into effect.

Namely, the most common response in our surveys is that Trump’s tariffs are not helping business. The No. 2 response is that it’s not clear what the impact of tariffs is. And only a small minority thinks tariffs are helping business.

In their own words, here is what some respondents had to say to the following question: Are President Trump’s tariff policies helping your business?

Yes

“We have seen new opportunities, and policy is the only reason the market has the current strength we are seeing. I believe CRU would be closer to $700 per ton without protection.”

“We support domestic steel producers. With low-cost imports out of the market, the playing field is level – and our higher level of service helps us stand out above our competitors.”

“Demand is down. If we had cheap imports rolling in (especially Canadian HR), prices would be 10% lower.”

“Helping, but we need interest rates to fall further to help more.”

“They have helped inventory values stay solid in a weak demand environment.”

I’m not sure

“But it does seem we are hearing from customers who traditionally import material.”

No

“They are having a significant negative impact on our volume.”

“So far, I think President Trump’s tariff policies have slowed manufacturing.”

“Besides the constant changing of the goal posts, all it has done has killed demand.”

“Too much uncertainty along with additional cost.”

“Uncertainty, inconsistency of policies.”

“They will drive us into recession.”

“Higher costs due to tariffs.”

“Chaos and cost pressures.”

By the way, here’s another pattern that didn’t change in our last survey: The much smaller “yes” camp (18% of respondents) is far more vocal in the comments section than its vote tally would suggest.

To me, what’s really striking is how silent the “I’m not sure” folks are in the comments. Perhaps it’s yet another sign of our polarized times, when moderates are too often shouted down by partisans… But, seriously, we’d love to hear more from the “I’m not sure” camp. Let us know what you’re thinking in our next survey!

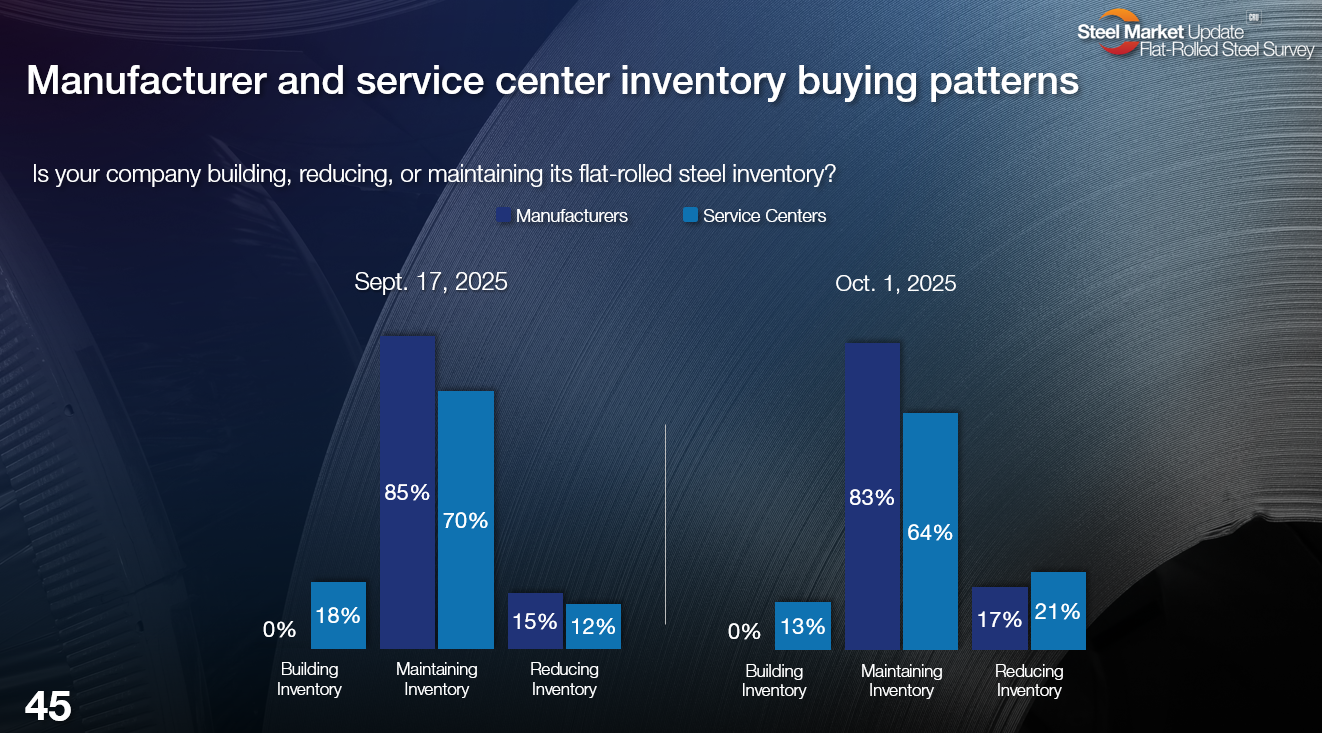

A word on inventories…

We’ll release data on September service center inventories on Oct. 15 to our premium subscribers. So, while I can’t offer the kind of granular data you’ll see then, I can at least give a sense of how things are trending.

And, according to our survey, a clear majority of steel buyers – both service centers and manufacturers – continue to either maintain or reduce inventories:

We do see a little restocking among service center respondents. But there had been hopes in some corners of the market that a restock could stretch out lead times and support higher prices. But so far, we’re not seeing evidence of that.

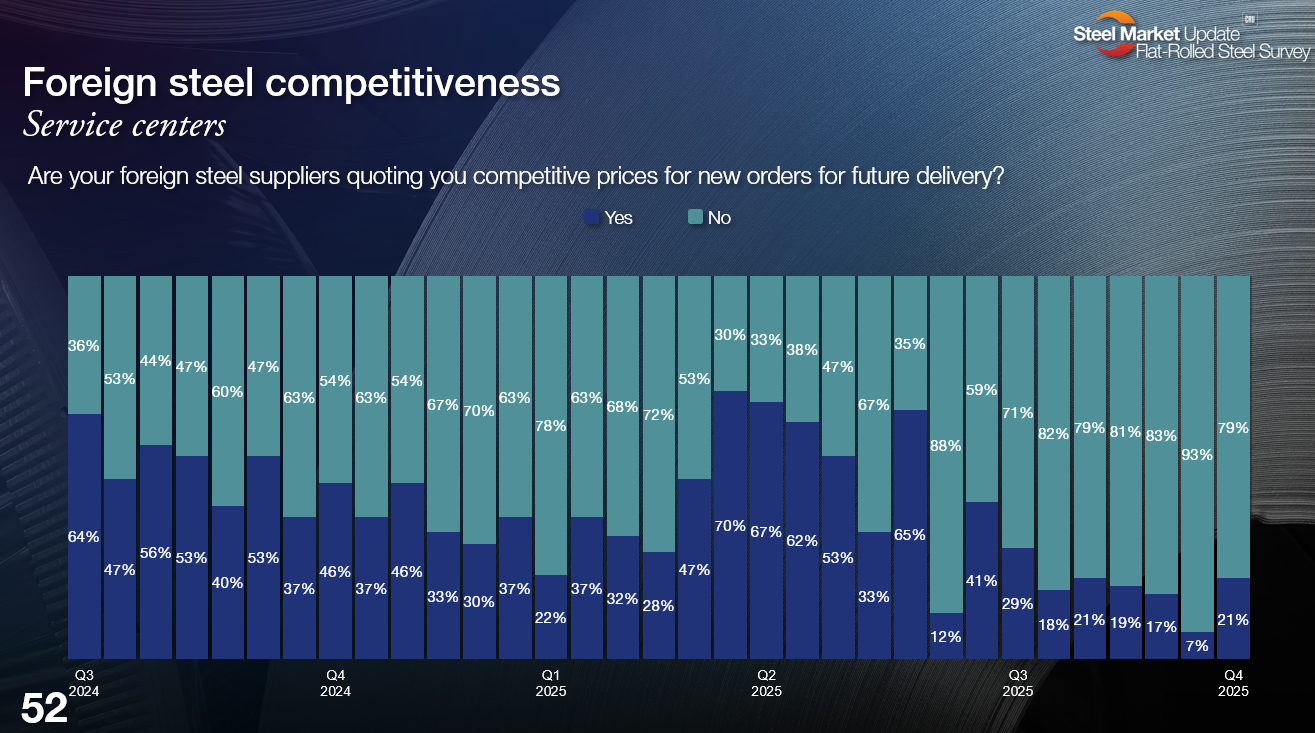

And a word on imports…

What we continue to evidence of is limited imports. Look at the chart below. Nearly 80% of service center respondents say that imports aren’t competitive.

And we’ve been seeing numbers like that since June, when Trump’s 50% Section 232 tariffs went into effect.

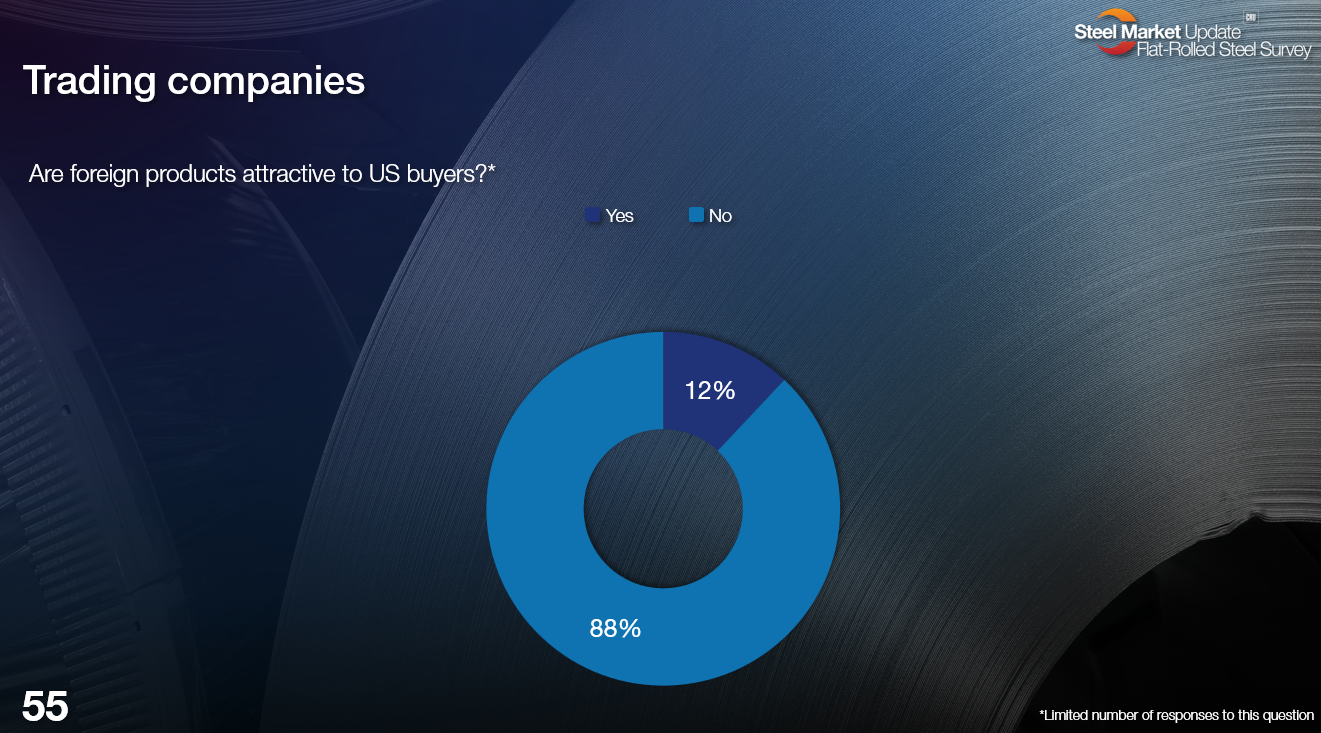

Meanwhile, most trading companies (88%) of respondents tell us that foreign steel isn’t attractive to US buyers.

In normal times, we’d probably have a good idea of what September import license figures looked like by now. When I wrote this column on Sunday, license data hadn’t been updated since Sept. 22 because of the government shutdown – which has impacted the Commerce Department, the agency that collects those figures.

But given results like the ones above, I’d be surprised if imports didn’t remain at low levels in September. And I’d expect them to remain low in October as well.

Thank you!

Shutdown politics is above my paygrade. So, I’ll leave thoughts on the matter to folks like Lewis Leibowitz, who has an interesting column on the matter here. What I can confidently say is this: Whatever happens in DC, SMU will always be here for you – and we truly appreciate your business.