Market Data

October 21, 2025

SMU Price Ranges: Sheet floor holds as market debates upside

Written by Brett Linton & Michael Cowden

SMU’s sheet prices held steady this week as continued market uncertainty appeared to be offset by pockets of strong demand in untraditional places.

By the numbers

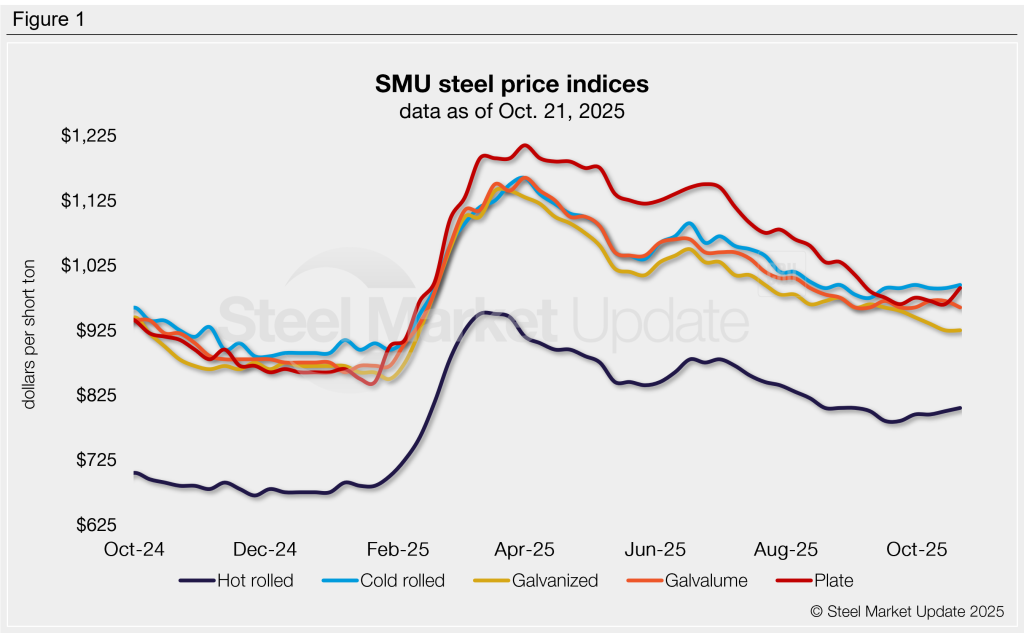

Our hot-rolled coil price increased to $805 per short ton (st) on average, up $5/ton from last week and marking a second consecutive week of modest gains. Market participants generally attributed the increase to a firming price floor.

It was a similar story in cold-rolled (CR) coil, where SMU’s price rose to $995/st on average, also up $5/st from a week ago.

One Midwest service center source provided a golf analogy: “When I got better, it was because my eights became sixes and sevens – not because I was getting more pars and birdies,” he said. In sheet, “It’s not so much that the price is going up, it’s just the worst of the worst is a little better than it used to be.”

While that analogy might hold for HR and CR, it might not be as apt for coated products.

SMU’s base price for galvanized sheet remained unchanged from last week at $925/st on average. While the higher end of our range increased, the lower end slid as pricing for heavy-gauge, HR-base galv slipped on a glut of domestic capacity.

Base prices for Galvalume product slipped $10/st week-on-week to $960/st on average. But it’s important to note that the modest decline in base prices happened against a backdrop of mills raising coating extras on the heels of a higher Midwest premium for aluminum — a subject Aluminum Market Update (AMU) has reported on extensively.

On the plate side, the picture was less blurry. SMU’s plate price increased to $990/st on average, up $25/st from a week ago. The gains follow a wave of mill price hikes. Also, our latest survey data shows plate mills are less willing to negotiate lower prices than sheet mills.

The big picture

Some market participants said they have grown more pessimistic about the prospects of the market turning around in Q4. They pointed to tariff uncertainty, uneven demand, and mills getting past their fall outages – something will increase supply. They are concerned about the possibility of a “sloppy” year-end market.

Others said steel was stronger than it might appear at first glance. They noted a litany of non-traditional sources of demand – including the border fence with Mexico, data centers, and energy transmission infrastructure necessary to meet increased energy requirements from data and AI.

Another non-traditional source of demand: Certain US mills are aggressively selling into Mexico (and perhaps into Canada as well). The reason: Using US-made steel in downstream, steel-intensive goods provides a way around 50% Section 232 tariffs.

Some sources said they could not quantify such non-traditional sources of demand. And they considered them more as talking points than as real market drivers. Others said those expressing such caution could be caught by surprise when it becomes clear that US mills have less availability.

Wildcards

Sources also mentioned some non-traditional wildcards to watch.

Among them is the potential for waivers or reductions in Section 232 tariffs on Mexican or Canadian steel for companies that expand downstream capacity in the US. (SMU will report on that matter later this week.)

Another wildcard: The impact of the fire at a Novelis aluminum mill in Oswego, N.Y, which AMU has also reported on extensively.

Immediately after the fire, attention turned to the Ford F-150, which has an aluminum body. But there is now an increasing focus on other models that are primarily made of steel but use aluminum in trunks, hoods, and other enclosures.

The big question: Whether and to what extent a shortage of automotive aluminum could cause broader production disruptions.

SMU’s price momentum indicator remains at neutral for sheet and plate, meaning we see no clear direction for prices over the next 30 days.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $760-850/st, averaging $805/st

The lower end of our range is unchanged w/w, while the top end is up $10/st. Our overall average is up $5/st w/w.

Hot-rolled lead times range from 3–6 weeks, averaging 4.7 weeks as of our Oct. 15 market survey.

Cold-rolled coil: $940-1,050/st, averaging $995/st

The lower end of our range is unchanged w/w, while the top end is up $10/st. Our overall average is up $5/st w/w.

Cold-rolled lead times range from 4–8 weeks, averaging 6.3 weeks through our latest survey.

Galvanized coil: $860-990/st, averaging $925/st

The lower end of our range is down $30/st w/w, while the top end is up $30/st w/w. Our overall average is unchanged w/w.

Galvanized .060” G90 benchmark: SMU price range is $938–1,068/st, averaging $1,003/st FOB mill, east of the Rockies.

Galvanized lead times range from 4–8 weeks, averaging 6.1 weeks through our latest survey.

Galvalume coil: $920-1,000/st, averaging $960/st

The lower end of our range is down $20/st w/w, while the top end is unchanged. Our overall average is down $10/st w/w.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,274–1,354/st, averaging $1,314/st FOB mill, east of the Rockies.

Galvalume lead times range from 5–8 weeks, averaging 6.5 weeks through our latest survey.

Plate: $950-1,030/st, averaging $990/st

The lower end of our range is up $30/st w/w, while the top end is up $20/st. Our overall average is up $25/st w/w.

Plate lead times range from 3–7 weeks, averaging 5.0 weeks through our latest survey.

SMU note: The graphic above shows a history of our hot rolled, cold rolled, galvanized, Galvalume, and plate prices. This data is also available on our website with our interactive pricing tool. If you need help navigating the site or logging in, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton