Analysis

October 23, 2025

Final Thoughts

Written by Michael Cowden

We’ve seen another week in which steel prices haven’t risen so much as the floor has firmed. The result: SMU’s hot-rolled coil price ticked a little above $800 per short ton (st) on average. That’s after dropping into the $700s for most of September and into early October.

What comes next depends on who you talk to and what data points they point to. We’ve all heard the narrative by now: Prices should go up on limited imports, lower inventories, and less discounting among US mills. SMU has written about that at length, and I’m not going to retread it here.

Below are some other issues that should be on your radar. Because while prices have been steady, a lot is going on when it comes to news that could impact them.

A (slightly) lower Section 232 tariff wall

One big question is around potential exemptions, waivers, and reductions to Section 232 tariffs on imported steel and aluminum. Notably when it comes to material from Canada and Mexico.

The tariff walls went up with big announcements from President Trump on Truth Social or in front of TV cameras. The chipping away of those walls – which probably makes sense for tightly integrated North American supply chains – seems to be happening more quietly and under the oversight of the Commerce Department.

Case in point: The big news last Friday (and with Trump, there is always news on Friday) was that the president would impose a 25% Section 232 tariff on imports of medium- and heavy-duty trucks as well as a 10% tariff on imported buses, including school buses. That’s all in a fact sheet here.

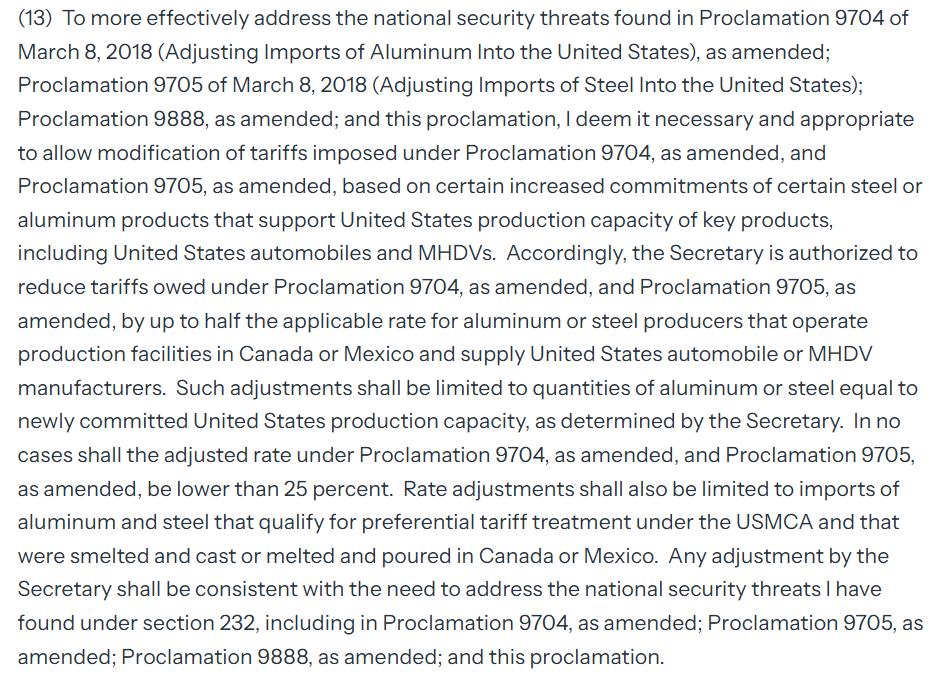

What’s worth a closer look is the full text of the president’s proclamation. Because that is arguably where the more important stuff is for the North American steel industry – especially in paragraph 13, which is below:

Here is the key part: Commerce Secretary Howard Lutnick “is authorized to reduce tariffs owed under Proclamation 9704, as amended, and Proclamation 9705, as amended, by up to half the applicable rate for aluminum or steel producers that operate production facilities in Canada or Mexico and supply United States automobile or MHDV manufacturers.”

A little translation here. Proclamation 9704 and 9705 are what was initially imposed for Section 232 tariffs on imported aluminum and steel, respectively, in 2018. MHDV is short for medium- and heavy-duty vehicles. In short, Canadian and Mexican steel mills can get reductions to S232 if they supply carmakers and truckmakers in the US.

To be clear, Lutnick is not giving away the farm. And the proclamation also specifies this key point: “In no cases shall the adjusted rate … be lower than 25%.” So we’re talking about Section 232 going from 50% back to 25% for Canada and Mexico in some limited instances.

This isn’t 2019 all over again, when there was a sudden lifting of S232 tariffs for Canadian and Mexican steel – and a subsequent fall in US prices. But it’s an indication that US tariffs walls can go both up and down. And that maybe, just maybe, we’re moving closer to the “Fortress North America” trade policy that several prominent steel executives argued for at Steel Summit in August.

The big question: Could we see more of such waivers or exemptions in the future? And what volume of steel could they impact?

An aluminum supply chain snarl

One more thing to watch in the hard-to-quantify-right now category: The impact on the automotive market of a significant fire last month at a Novelis aluminum mill in Oswego, N.Y. Aluminum Market Update (AMU) has written extensively about the issue. Some of that reporting is here.

Cleveland-Cliffs President, Chairman, and CEO Lourenco Goncalves wasted no time in his company’s earnings call on Monday to spike the football in aluminum’s end zone.

“When light-weighting became a major trend several years ago, some automakers jumped on the aluminum bandwagon,” Goncalves said. “A huge fire at the nation’s largest automotive aluminum producing mill this past quarter revealed the fragility of that shift.”

“Vehicle models that were years ago moved away from steel and toward aluminum are suffering the most. The silver lining is that switching back to steel is now under serious consideration by the most affected OEMs,” he added.

Goncalves has a point. Maybe we’ll see vehicles shift from aluminum back to steel in the years ahead. But for now, the bigger question is what happens to production lines over the next few weeks.

After the fire, attention immediately turned to the potential impact on the Ford F-150 pickup truck, which stunned the steel world when it switched from a steel body to an aluminum one about a decade ago.

But scores more vehicles for years have been making less dramatic shifts – notably when it comes to switching from steel to aluminum in “enclosures” such as hoods and trunks. When and to what extent could we see automotive production disrupted given the current US automotive aluminum supply squeeze and a 50% S232 tariff on imported material?

In the meantime, we’ve heard some crazy stories. Are certain automotive companies flying in aluminum from abroad and absorbing the S232 tariff too to keep lines going? SMU hasn’t been able to verify that. But the chatter is out there.

He’s back: The chip shortage, that is

Writing about potentially widespread disruption to automotive production because of parts shortages reminded me of 2021. Back then, it felt like SMU was reporting on chip shortages and automotive lines shutting down just about every day.

So, when I started messaging colleagues about the aluminum issue, I was surprised to learn that it might be less significant than I thought because of – wait for it – a chip shortage.

That’s right. Jason Voorhees of Friday the 13th fame isn’t back. But the chip shortage is.

If you’re not familiar with it, the Detroit Free Press has some good coverage of the matter. That’s here.

In short, China and the Netherlands have gotten into a serious spat over intellectual property related to chips. The result: Nexperia, a chipmaker based in the Netherlands, might be unable to supply auto parts companies and automakers. And the issue could begin impacting US auto assembly plants within as little as week or so.

“We don’t know all the circumstances surrounding this incident. What we do know (from very recent experience) is this: Disruptions to the interconnected automotive supply chain will quickly ripple inside the US and around the world,” John Bozzella, CEO of Alliance for Automotive Innovation, said in a statement to the Free Press.

“If the shipment of automotive chips doesn’t resume ― quickly ― it’s going to disrupt auto production in the US and many other countries and have a spillover effect in other industries. It’s that significant,” he added.

It’s worth noting here that the Alliance for Automotive Innovation represents a who’s who of the global auto industry – not just US automakers but foreign automakers and parts manufacturers from across the globe.

Here’s is another way to think about it. One bad thing (a potential aluminum shortage) is maybe not so bad. Because another bad thing (a potential chip shortage) is worse.

That’s, admittedly, a dark way to look at it. And, again, I’m not going to sound a three-alarm fire. But these are all issues that you should be paying close attention in the weeks ahead. And we’ll no doubt be reporting on them in more detail in future issues of SMU and AMU.