Analysis

November 4, 2025

Final Thoughts

Written by Ethan Bernard

It’s hard to believe we’ve slid well into the final quarter of 2025. Thanksgiving is just around the corner, and soon we will be ringing in the new year. But we’re not exactly close to popping the champagne just yet. While 2025 was a year of trade disruption, what are the chances 2026 will be a year when equilibrium is reached?

That word equilibrium is a slippery one, though. For example, the Covid-19 crisis has passed, but few people think the world has ever fully snapped back. Especially since Russia’s 2022 invasion of Ukraine, 2019 seems a long-gone memory. At the same time, markets always move forward. Like the Great White Shark, they keep moving forward or they pass away. So how do you avoid getting swallowed up by the market?

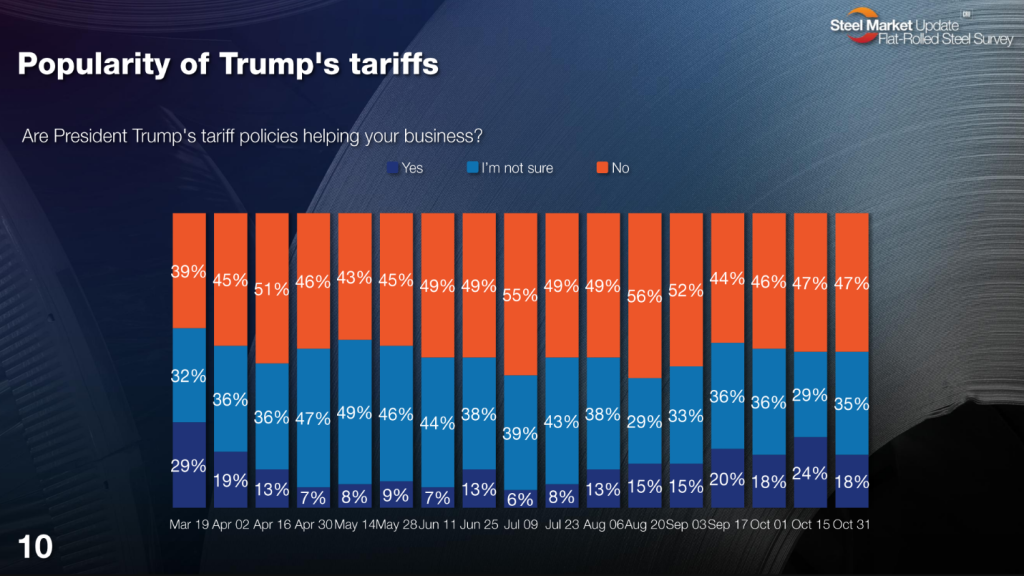

But I’m getting ahead of myself. What is market sentiment like around President Trump’s tariffs? Here are the results from SMU survey respondents in our most recent market check, which concluded last week.

Are President Trump’s tariff policies helping your business?

And here’s what respondents were saying:

“Demand is not high. We are simply bouncing off the bottom, but we likely won’t see a massive run-up.”

“Now, more than earlier in his presidency, the tariff policies MIGHT be helping our business.”

“Not hurting it, either.”

“Reshoring.”

“General feeling of the unknown.”

“Tariffs are making costs higher.”

What it means

I think the “unknown” really captures things at this point. Tariff unpopularity has come off a high of 56% in August, but it still stands at nearly 50%. Factor in the 35% “undecided” in the current survey, and we are looking at a whopping 82% who don’t currently view the tariffs favorably. And recall that, according to our survey, a majority of our readers supported Donald Trump in this election.

While the tariffs are not popular, they are reality. And if chaos is the order of the day for long enough, chances are the markets will start to factor that in, and new patterns will emerge.

Look at “reshoring” as a tariff-avoidance strategy. Perhaps that word may end up being different as the trade landscape continues to develop.

While one side of the coin is US companies returning manufacturing to the US, the other side is foreign companies coming to the US to avoid tariffs.

Take the example of POSCO. It’s in a partnership with fellow South Korean company Hyundai to build a $5.8-billion EAF mill in Louisiana.

Just last week, it announced a memorandum of understanding had been signed with Cleveland-Cliffs for a “transformative partnership.” Korean press reports mentioned a stake of at least 10% and an investment of more than $ 700 million in the Cleveland-based steelmaker.

Hyundai produces vehicles in the US, and the companies have stated that one of their aims is to deliver steel for US facilities. POSCO is no stranger to the US market, but what kind of player will it be in the US market over the next few years?

More broadly, how might supply chains evolve in this environment over the next few years as companies make sure they don’t get bitten by tariffs?

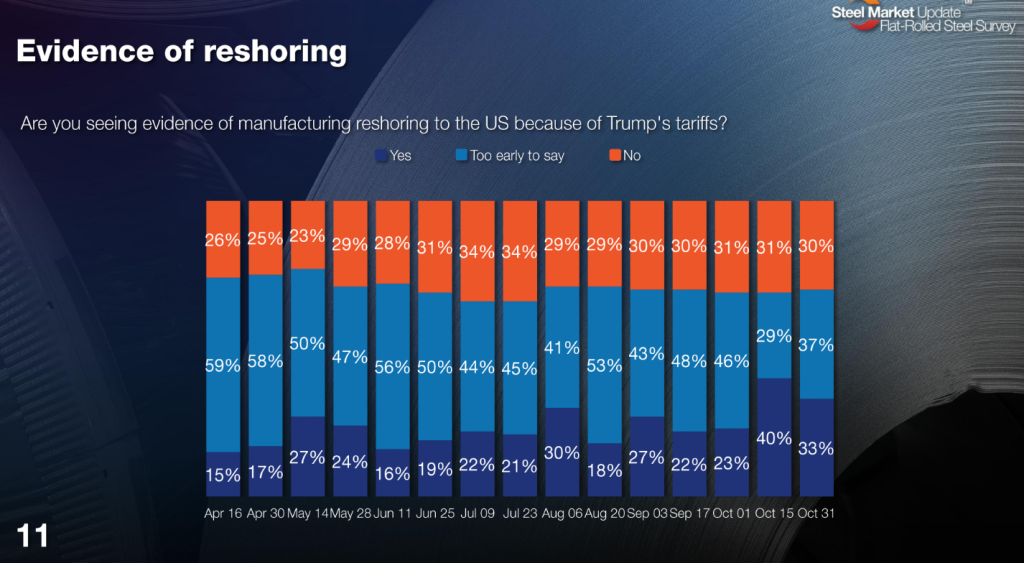

As for what’s taking place now, here are survey results around the question of reshoring.

Are you seeing evidence of manufacturing reshoring to the US because of Trump’s tariffs?

Reshoring is not the kind of massive development that can be turned on a dime. Still, nearly 70% of survey respondents say tariffs are not spurring reshoring, or it’s too early to tell. Let’s see where we are a year from now on that one…

In the meantime, respondents said:

“Just a little bit.”

“But only very minor instances.”

“Demand is up domestically due to tariffs.”

What’s something that’s going on in the market that nobody is talking about?

We always include this question in our surveys. I thought the answers below were revealing because they provide a tour of today’s issues: service center consolidation, overcapacity, and carbon taxes.

Here’s what they said:

“Service center industry likely still needs consolidation. Far too many small service centers given muted demand. This is the path to service centers not racing to the bottom of the market to fight over orders.”

“Should anything be done to limit the domestic sheet mill overcapacity?”

“How additional carbon tax increases are affecting demand and pricing.”

“2026 breakout.”

Final thoughts on Final Thoughts

I like that last answer: “2026 breakout.” Exciting things are brewing. And if a 2026 breakout is indeed in the offing, let’s all hope it’s to the upside! We’ll have plenty of time to talk about it at our Tampa Steel Conference in February. Hope to see you all there!