Analysis

November 12, 2025

HRC vs. prime spread widens again in November

Written by Ethan Bernard & Stephen Miller

The price spread between HRC and prime scrap has widened for a second month, based on SMU’s most recent pricing data.

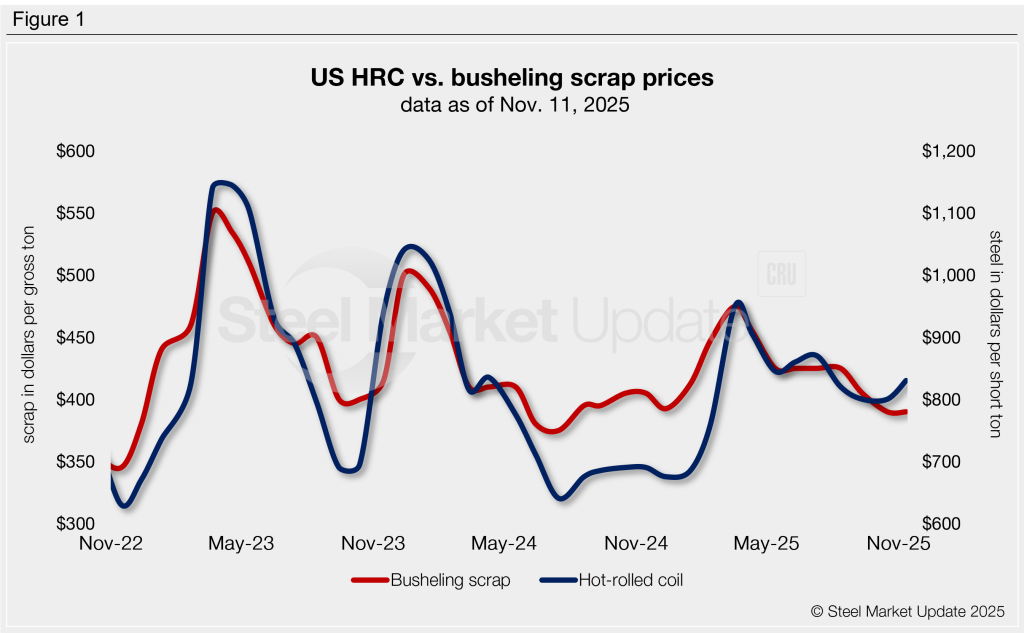

SMU’s average HRC price was $830 per short ton (st), FOB mill, east of the Rockies, as of Tuesday, Nov. 11. That’s up $5 from the previous week and $30 from the prior month.

Meanwhile, busheling tags for November stayed flat month on month at an average of $390 per gross ton (gt).

Figure 1 shows price histories for each product.

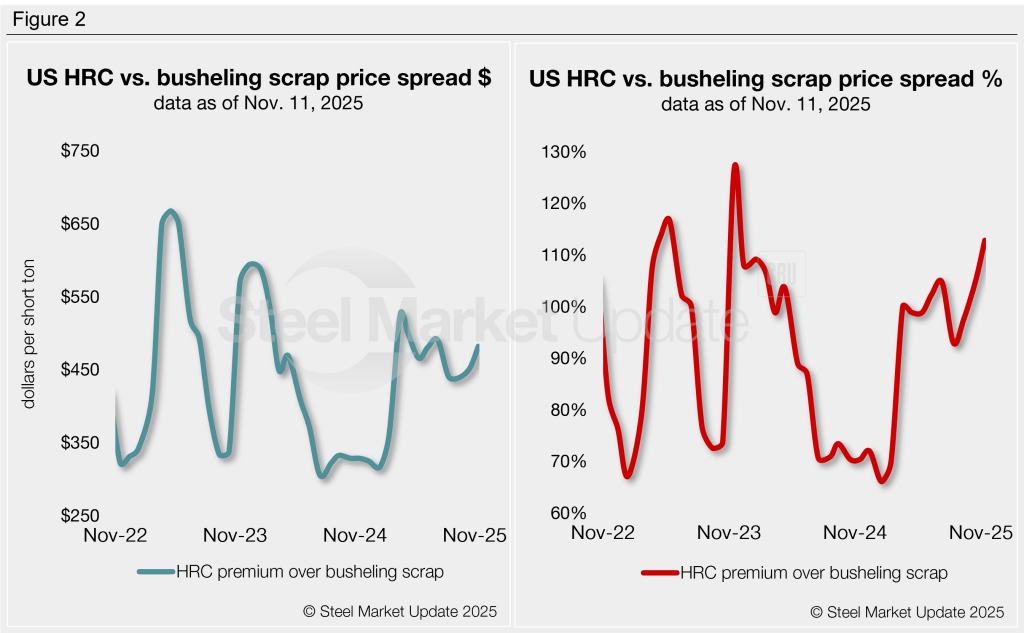

After converting scrap prices to dollars per short ton for an equal comparison, the differential between HRC and busheling scrap prices was $482/st as of Nov. 11. That’s an increase of $30/st from a month earlier. This is the widest spread since July, when it stood at $491/st (Figure 2).

What’s going on?

The scrap market has started to show some firmness, as November’s sideways move suggests a bottom has been reached.

Scrap flows will be slower in December and won’t meaningfully recover until spring, weather permitting. So, in the December-February period, scrap prices are expected to increase.

The amount of that increase is speculative, but over the last three years, prices increased by $80-100/gt during the winter months.

Therefore, unless HRC prices match or at least track the upward movement in scrap, the spread between busheling and HRC is likely to narrow.

HRC premium as a percentage

The graph on the right-hand side of Figure 2 shows the spread relationship differently: We have graphed HRC’s premium over busheling scrap as a percentage. HRC prices now hold a 113% premium over prime scrap compared to 105% a month earlier.

Ethan Bernard

Read more from Ethan Bernard