Analysis

November 19, 2025

SMU Steel Demand Index falls back, remains in contraction

Written by David Schollaert

SMU’s Steel Demand Index slackened from late October, remaining below expansion territory, according to mid-November indicators.

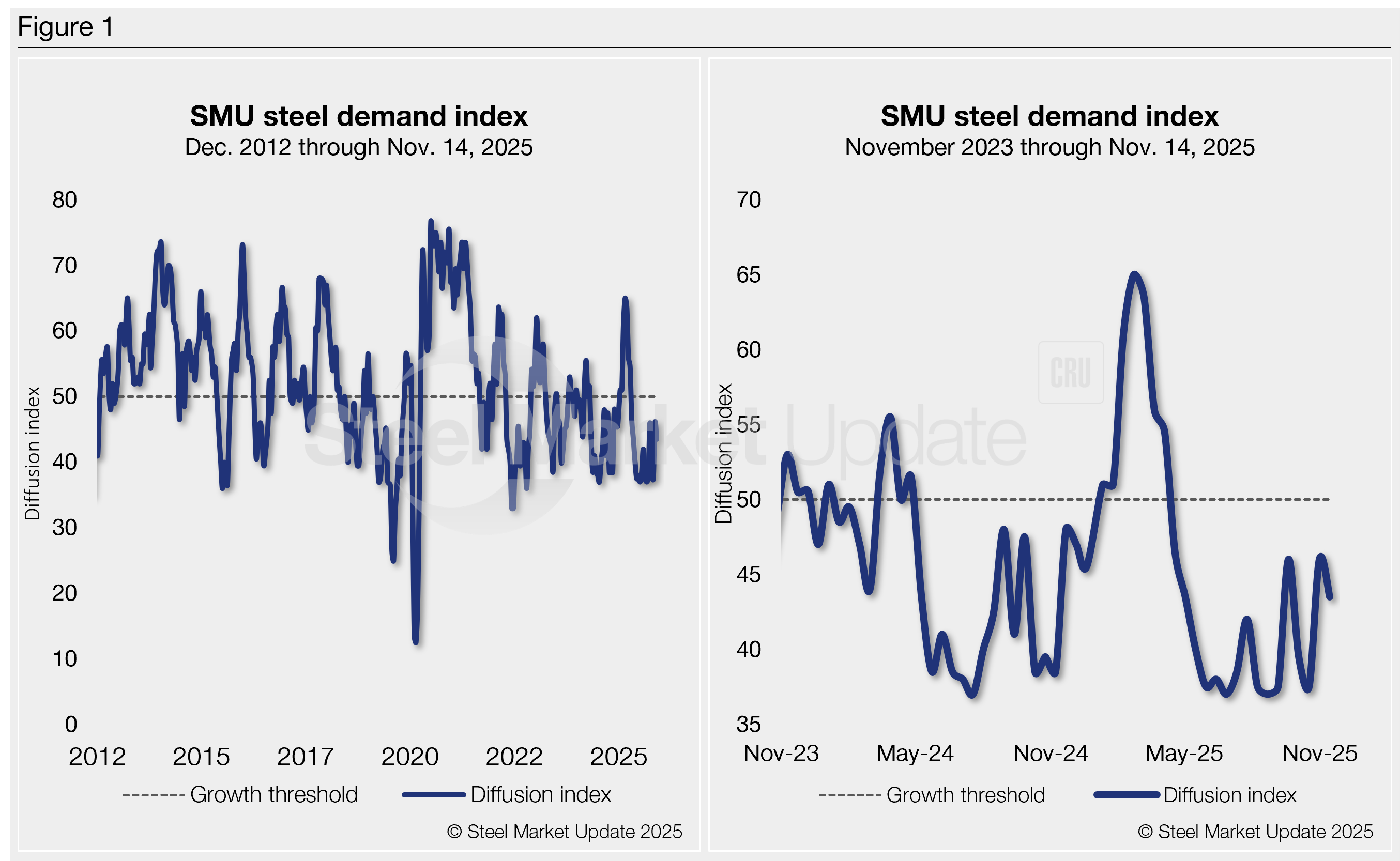

The Steel Demand Index, compiled from our survey data, now stands at 43.5, down from late October and far off from a four-year high of 65.0 in late February.

Though growth faded again, the index has detailed a bit of the see-saw buying pattern we’ve seen throughout the spot market. Especially following the early buying flurry ignited by the onset of undiluted Section 232 tariffs in March.

Still, the slowdown remains largely in place due to softer demand and ongoing tariff uncertainty.

Following steady declines since the back half of March, the index has recovered slightly in response to some Q4 buying backed by mill price hikes. But still, the index has struggled to find its footing since mid-April and remains out of expansion territory.

Methodology

Derived from the market surveys SMU conducts every two weeks, the index compares lead times and demand to create a diffusion index. This index has historically preceded lead times. This is notable given that lead times are often seen as a leading indicator of steel price moves. An index score above 50 indicates rising demand, and a score below 50 suggests declining demand.

Figure 1 shows the nearly 13-year history of the index on the left and provides a closer look at the Steel Demand Index readings of the past two years on the right.

Rearview mirror analysis

Last year, demand slipped. Not all at once—just a slow, steady drop. Spot buying faltered and prices faded. The index sank into contraction and stayed there most of 2024.

Momentum accelerated at the start of the year, driving growth. But despite brief price spikes — driven by sudden price increases from mills — market conditions have stayed soft due to sluggish end-use demand.

That has been a very similar story for 2025 as well. The main caveat is that tariffs have set a slightly higher floor for prices this year. Still, demand has continued to contract since mid-April.

A tale of shifting tariffs

Early optimism with the arrival of a new presidential administration faded after a reworked Section 232 tariff stirred the market. And while tariff uncertainty has curbed buying, weaker demand has been the culprit.

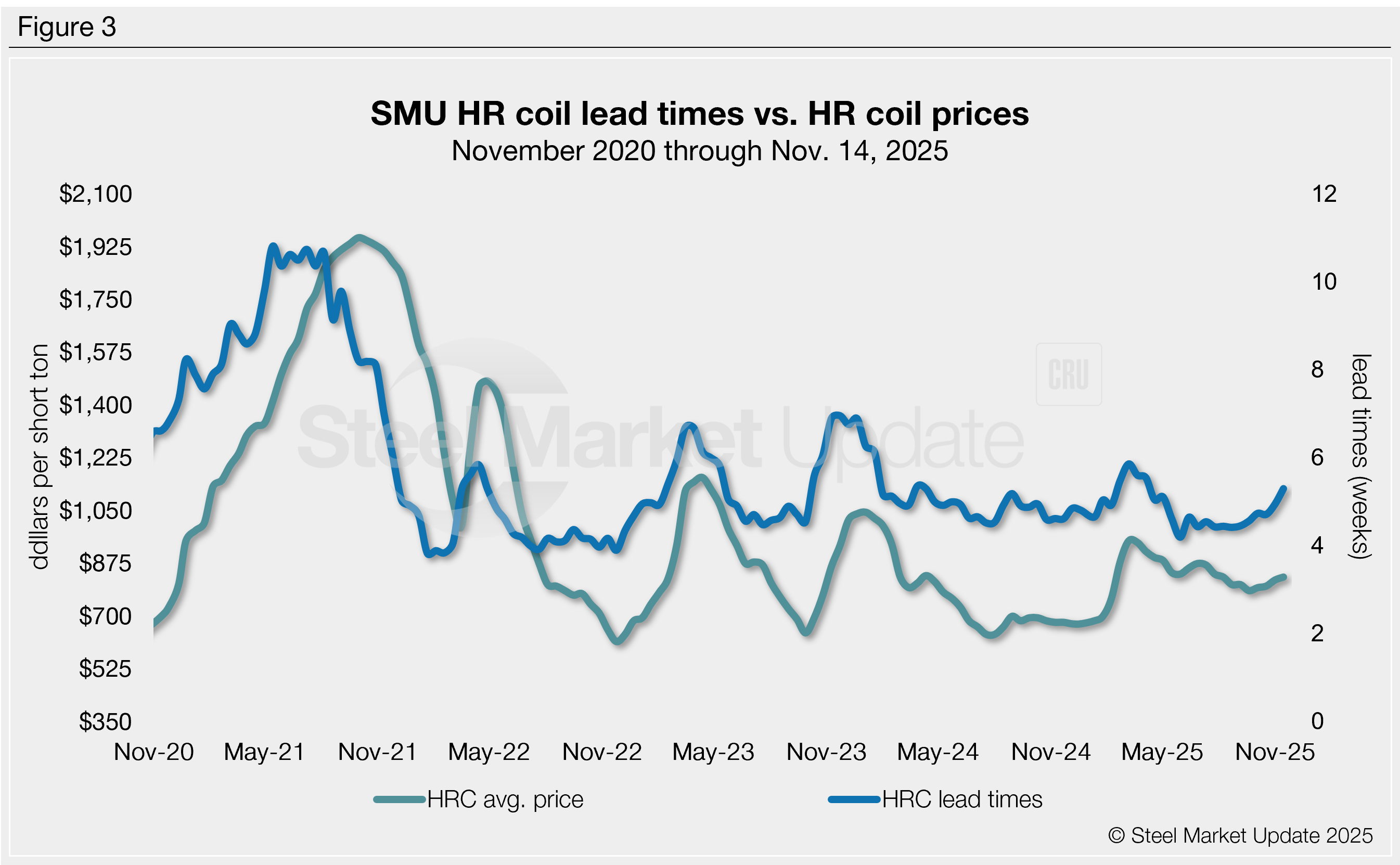

HR coil prices have followed a similar trend, reaching an average of $950 per short ton (st) in early March. But then they slowly declined for nearly 30 straight weeks to $795/st. They now average $860/st, according to SMU’s latest market check on Tuesday, Nov. 18.

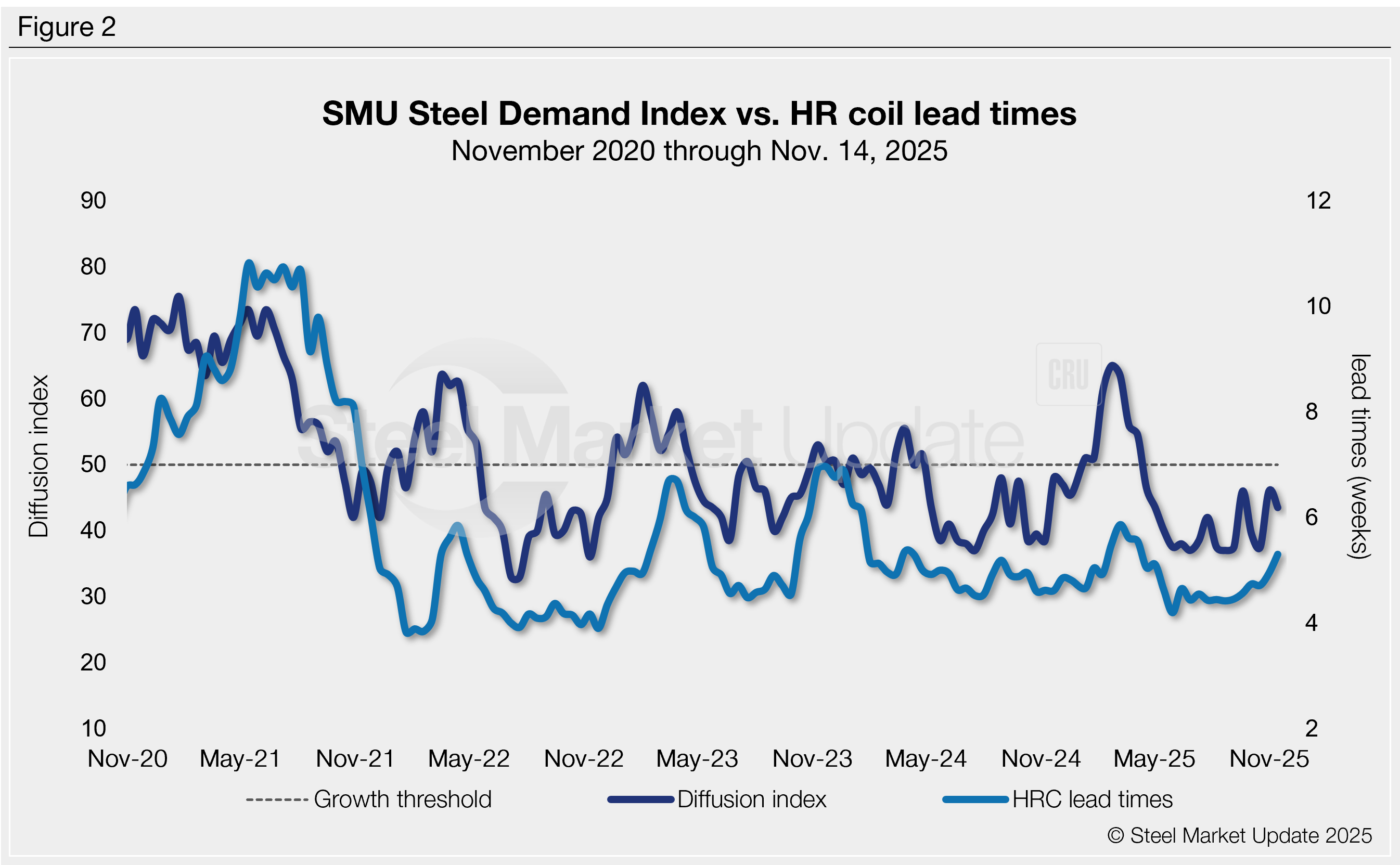

Lead times have moved up as well, now at 5.30 weeks for HR in our latest assessment on Nov. 12. That’s the longest lead time reading in 16 weeks.

For nearly a decade, SMU’s steel demand diffusion index has preceded moves in mill lead times (Figure 2), and SMU’s lead times have also been a leading indicator of flat-rolled steel prices, particularly for HRC (Figure 3).

In their own words

Here are a few quotes from our latest survey about how flat-rolled steel buyers see demand:

“A new normal is setting up in the spot market. Customers are buying what they need when they need it.”

“We’ve seen growth through regional expansion, but not so much from overall economic demand.”

“Demand is weak and not showing much strength for imports at the moment.”

“Slight pick-up.”

“A weak stable – could slip down.”

“Demand has picked up compared to some very slow times earlier this year.”

“Orders keep coming, but are smaller in size.”

“These rate cuts aren’t translating to more CapEx spends…at least not yet.”

Signals ahead

Demand is steady, but buying remains largely tied to contracts—in many cases, buyers are taking max volumes but buying sparingly on spot. Inventories remain closely monitored.

But lead times and prices are moving up. In fact, HR coil prices are in the middle of one of their most sustained rallies since Q1. And while few, if any, expect demand to rally at a significant rate early in the new year, tariffs have cut import competition, providing a higher floor.

Add that to lean inventories and higher raw material costs, and you have some support for a rally. And still, most are having no trouble finding available tons.

But how long does it last if it’s not fundamentally demand-driven?

Maybe a while? If mills continue holding the line on pricing, especially in such a protected market, we’re unlikely to see any pricing volatility for the time being.

Ultimately, time will tell.

Editor’s note

Demand, lead times, and prices are based on the average data from manufacturers and steel service centers participating in SMU’s market trends analysis surveys. Our demand and lead times do not predict prices but are leading indicators of overall market dynamics and potential pricing dynamics. Look to your mill rep for actual lead times and prices.