Market Data

January 29, 2026

Steelmaking raw material prices increase through January

Written by Brett Linton

Editor’s note: Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact Luis Corona at luis.corona@crugroup.com.

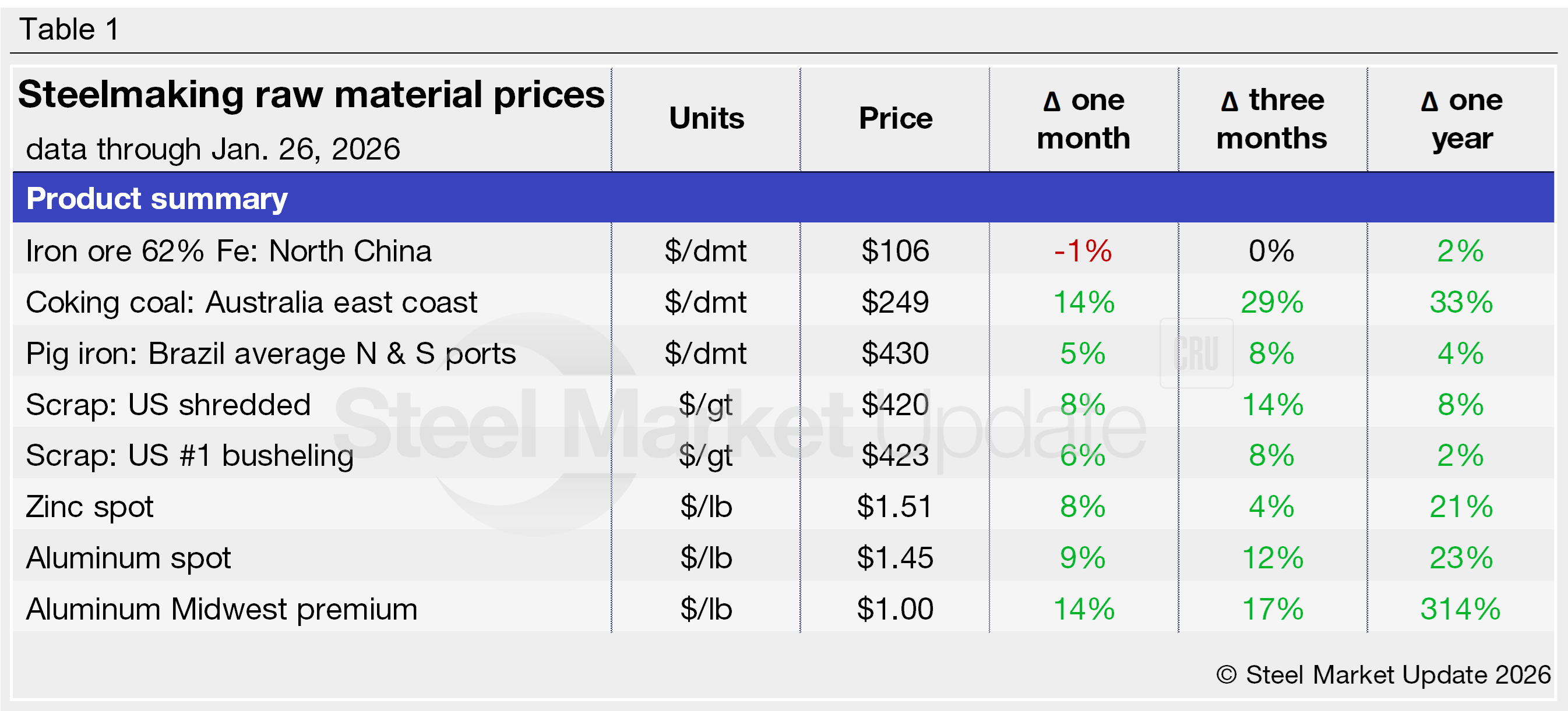

All but one of the steelmaking raw materials we track increased in price over the last month. Coking coal, pig iron, shredded scrap, busheling scrap, zinc, and aluminum prices have all risen in the last 30 days, while iron ore declined 1%. Collectively, prices rose 8% month over month (m/m). Seven of the eight products we track are more expensive than they were three months ago, and all are greater than levels recorded this time last year.

Table 1 shows the latest prices for each product and their changes from recent months.

Iron ore

Chinese iron ore fines (62% Fe, delivered North China) have remained over $100 per dry metric ton (dmt) for over six months. Through the week of Jan. 26, prices have eased to a six-week low of $106/dmt, down 1% compared to month-earlier levels (Figure 1). Iron ore is now equal to prices seen three months ago and 2% higher than it was this time last year.

Coking coal

Premium hard coking coal prices have trended upwards in the past six months, rising 14% m/m to reach a one-and-a-half-year high of $249/dmt this week (Figure 2). Coking coal prices have risen 29% across the past three months and are up 33% from year-ago levels.

Pig iron

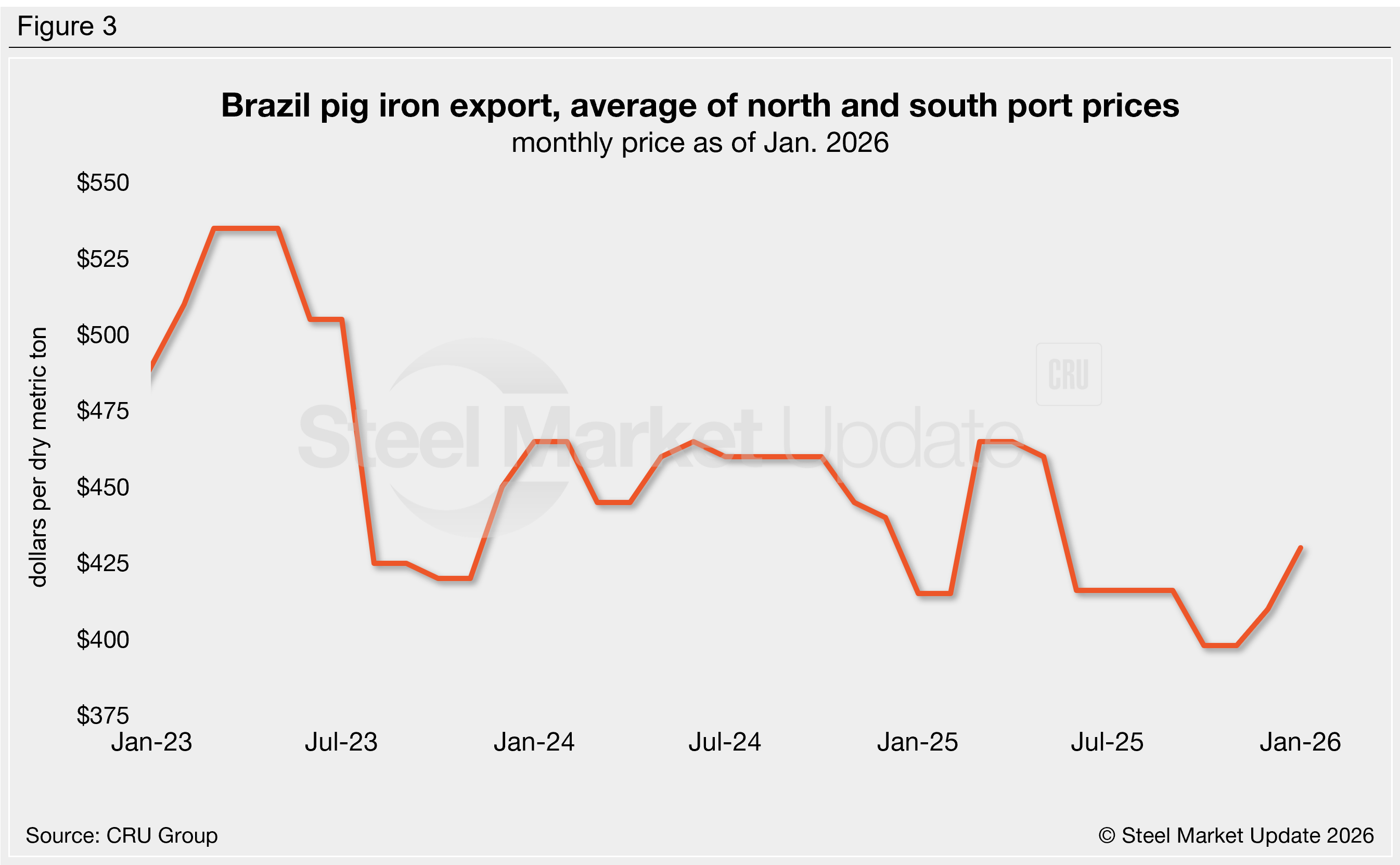

Brazilian pig iron prices increased 5% m/m in January to $430/dmt, the highest price recorded since May 2025 (Figure 3). Pig iron has risen 8% across the last three months and is 4% more expensive than it was one year ago. Prices are expected to rise again in February per a recent SMU article by Stephen Miller.

Note that this report uses Brazilian pig iron prices, now the main source of US imports rather than Russia and Ukraine, averaging prices from the country’s northern and southern ports.

Scrap

Steel scrap prices recovered for the second-consecutive month in January. SMU’s shredded scrap index rose to $420 per gross ton (gt) and our busheling index increased to $423/gt. Scrap prices are 8-14% higher than they were three months prior and 2-8% above those seen this time last year (Figure 4). As published earlier this week, many buyers expect scrap prices to increase further in February due to harsh winter weather and shipment disruptions.

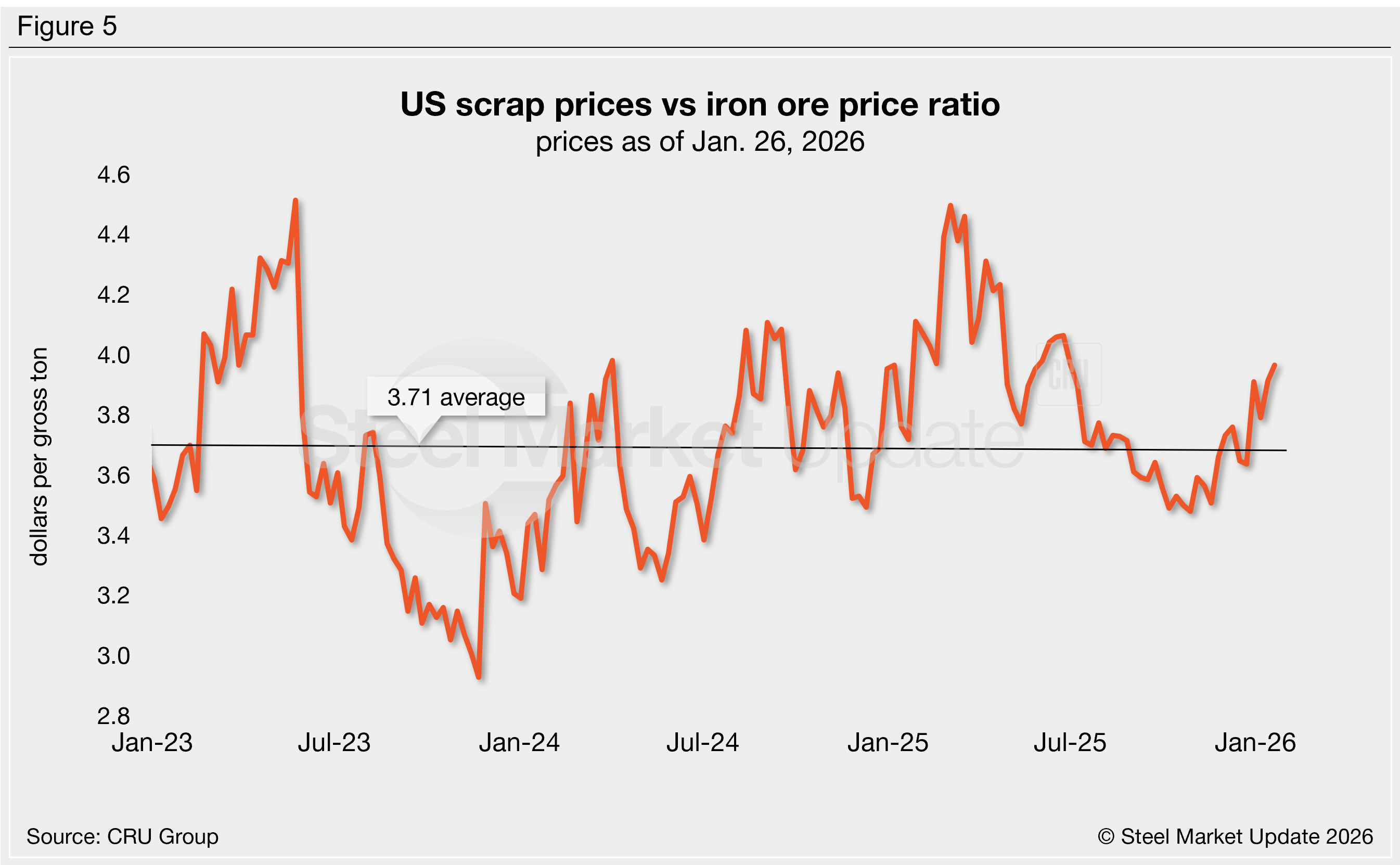

Fluctuations in scrap and iron ore prices provide insight into the competitiveness of integrated (blast furnace) mills, whose primary feedstock is iron ore vs. mini-mills (electric-arc furnace), whose primary feedstock is scrap. To compare these two mill materials, SMU divides the shredded scrap price by the iron ore price to calculate a ratio. A higher ratio favors integrated mills, a lower ratio favors mini-mill producers (Figure 5).

Focusing on the last two years, this cost advantage gradually shifted from mini-mill producers in 2024 to integrated mills in early 2025. After peaking in March of last year, the ratio trended lower through late 2025, but reversed course in recent weeks. As of this week it stands at 3.97, slightly favoring integrated producers.

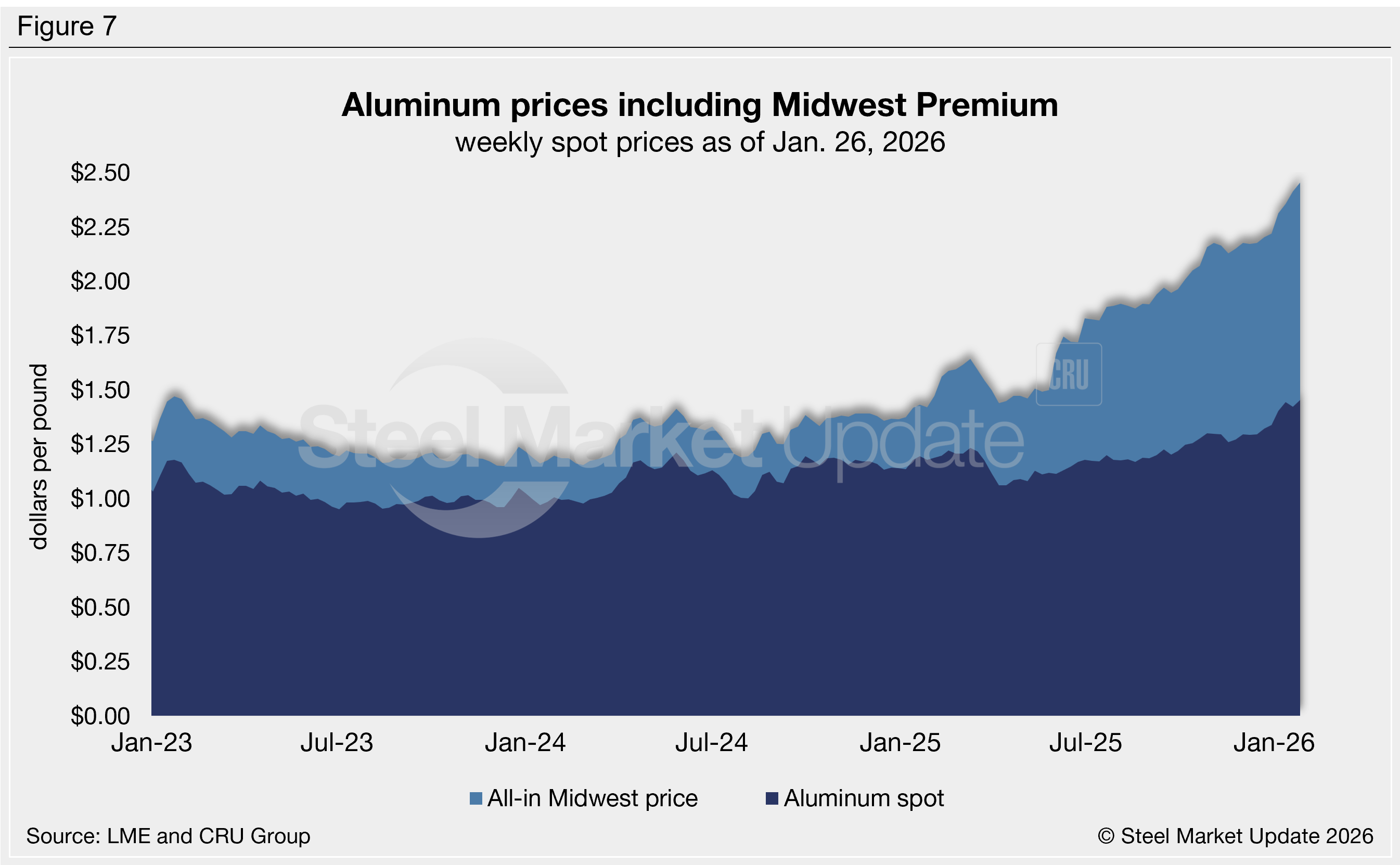

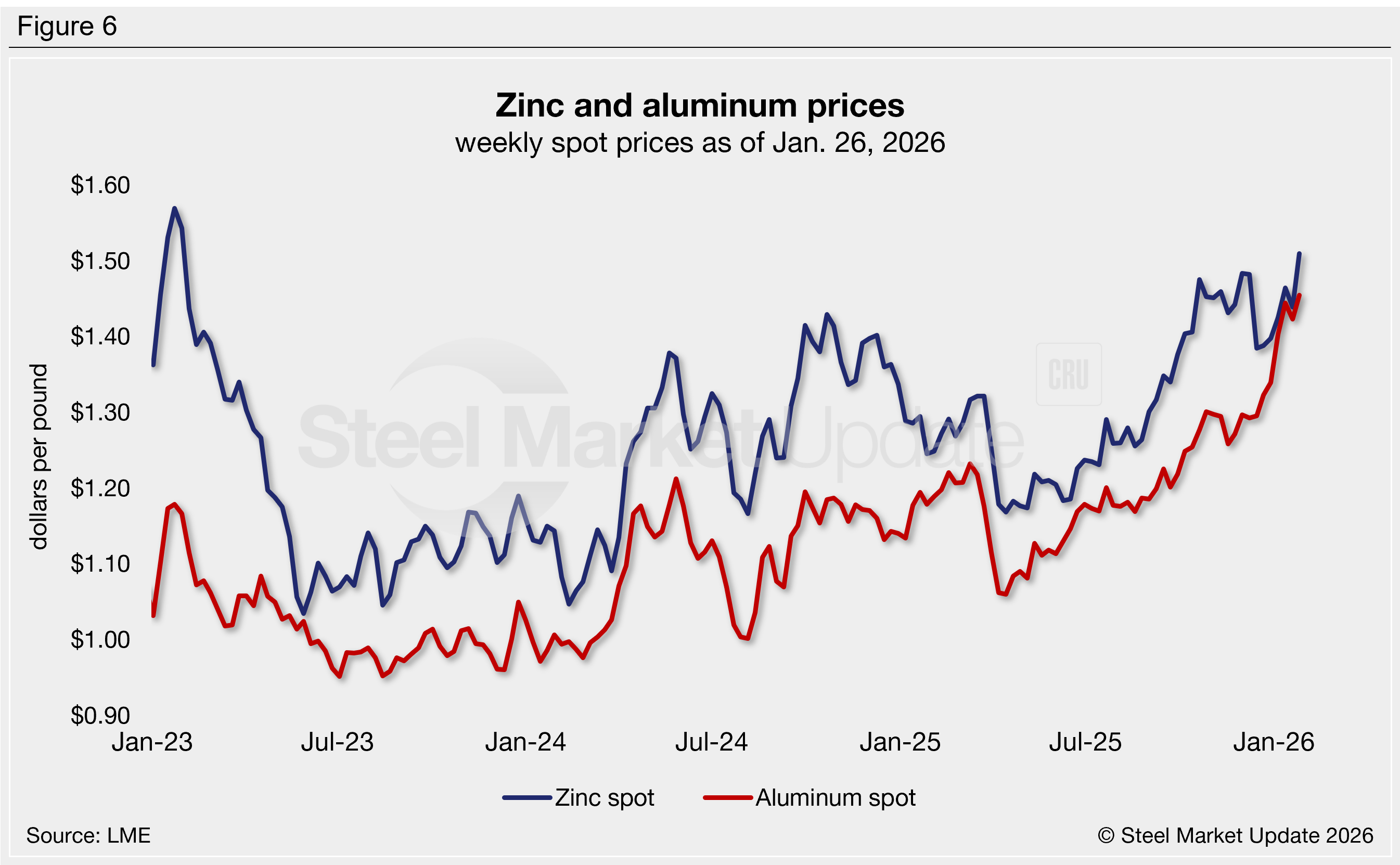

Zinc and aluminum

Zinc and aluminum are used in some coated steel products. Fluctuations in spot prices can prompt steel mills to adjust their galvanized and Galvalume coating extras.

Zinc prices have trended upwards over the last eight months, reaching a near-three-year high of $1.51/lb as of Jan. 26. Prices have risen 4% over the past three months and are up 21% from this time last year (Figure 6).

Aluminum spot price movements typically mirror those of zinc. However, we saw these prices diverge in December when aluminum prices spiked. The latest weekly LME cash price is up to $1.45/lb, the highest rate seen in almost four years (Figure 6). Prices have increased 12% in the last three months and 23% year over year.

The weekly average aluminum MWP reached $1.00/lb this week, the highest rate recorded in our limited six-year data history. The MWP has increased 17% over the past three months and is up 314% from this time last year. The all-in Midwest aluminum price now totals $2.45/lb, the highest in our limited history (Figure 7).