Analysis

February 20, 2026

HRC vs. prime spread widens in February

Written by Ethan Bernard & Stephen Miller

The spread between domestic hot-rolled coil and prime scrap prices widened slightly in February. It has been trending in that direction since October.

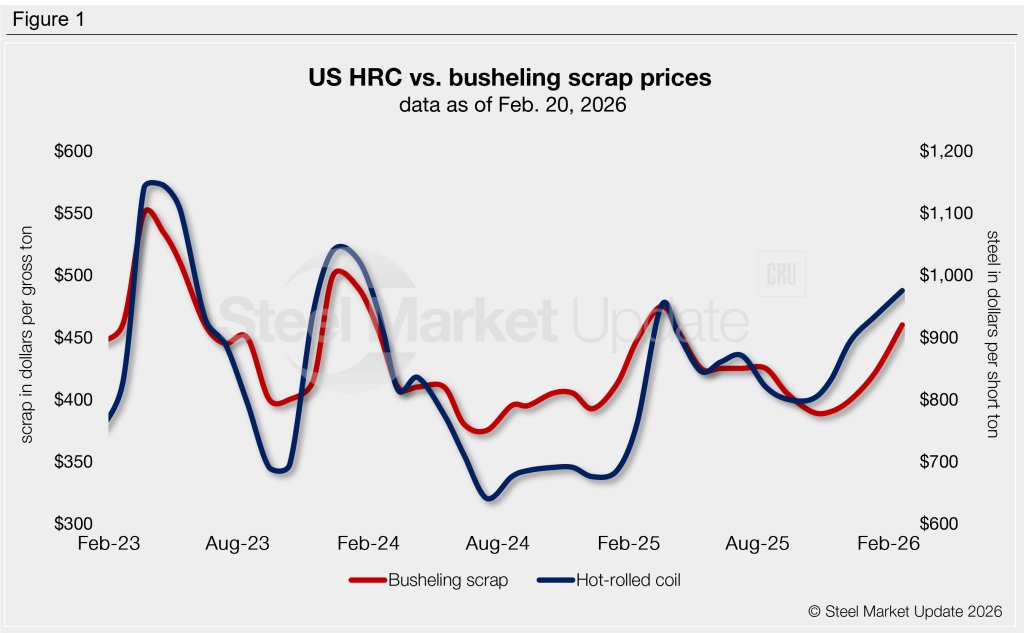

SMU’s average HRC price was $975 per short ton (st), FOB mill, east of the Rockies, as of Tuesday, Feb. 17. That’s even with the previous week but up $30/st from January.

For busheling, tags in February jumped $37.50 month over month to an average of $460 per gross ton (gt).

Figure 1 shows price histories for each product.

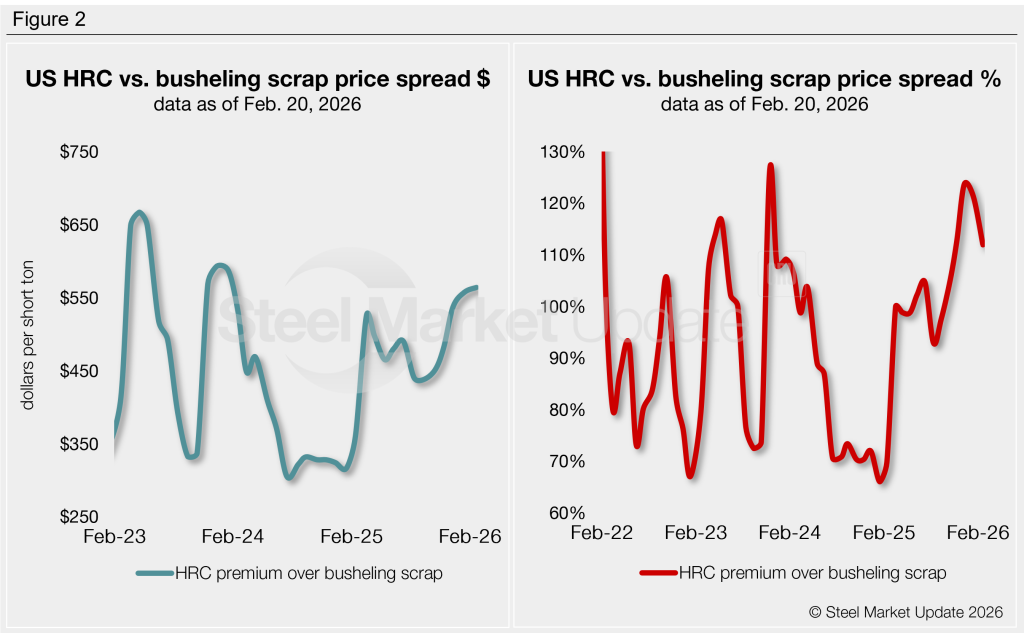

After converting scrap prices to dollars per short ton for an equal comparison, the differential between HRC and busheling scrap prices was $564/st as of Friday, Feb. 20. That’s an uptick of $6/st from a month earlier. This keeps the spread in territory not seen since the beginning of 2024, when it stood at $588/st (Figure 2).

What’s going on?

The US busheling price will most likely start to decrease as spring weather starts to loosen up scrap flows. Whether that happens in March or April is uncertain at this point.

However, this cannot be said about HRC. Steelmakers have been busier so far this year, and it is unlikely there will be an imminent decline in steel prices. So, this implies the spread between these two commodities should widen in the next 1-2 months.

HRC premium as a percentage

The graph on the right-hand side of Figure 2 shows the spread relationship differently: We have graphed HRC’s premium over busheling scrap as a percentage. HRC prices now hold a 112% premium over prime scrap, down from 121% a month earlier.

Ethan Bernard

Read more from Ethan Bernard