Market Data

March 10, 2026

SMU Price Ranges: Sheet and plate flat or up as tight market keeps pricing power with mills

Written by Brett Linton & Michael Cowden

Sheet and plate prices were flat or higher this week in a US market that remains characterized by extended lead times and limited spot availability.

SMU’s price assessment for hot-rolled (HR) coil was unchanged at $1,005 per short ton (st) on average. Meanwhile, prices for cold-rolled (CR) and galvanized products rose by $15/st to $1,155/st and $1,125/st, respectively.

Market commentary

Some sources said they could max out their contracts to secure the tons they need. But others said they were being held to contract minimums and were struggling to get spot tons to fill any gaps.

Among the factors market sources said were keeping supplies tight: EAF mills have only limited spot availability. One re-roller is facing late slab deliveries. And an integrated mill is grappling with potential overbooking and delayed order processing.

Some buyers said they were having trouble even getting quotes for CR and coated products because mills could make more money on commodity HR than they could on value-added, downstream goods.

Plate prices are also up on the heels of another round of mill price hikes.

A bit of history

How tight is the current market? Below are some historical data points to put it in context.

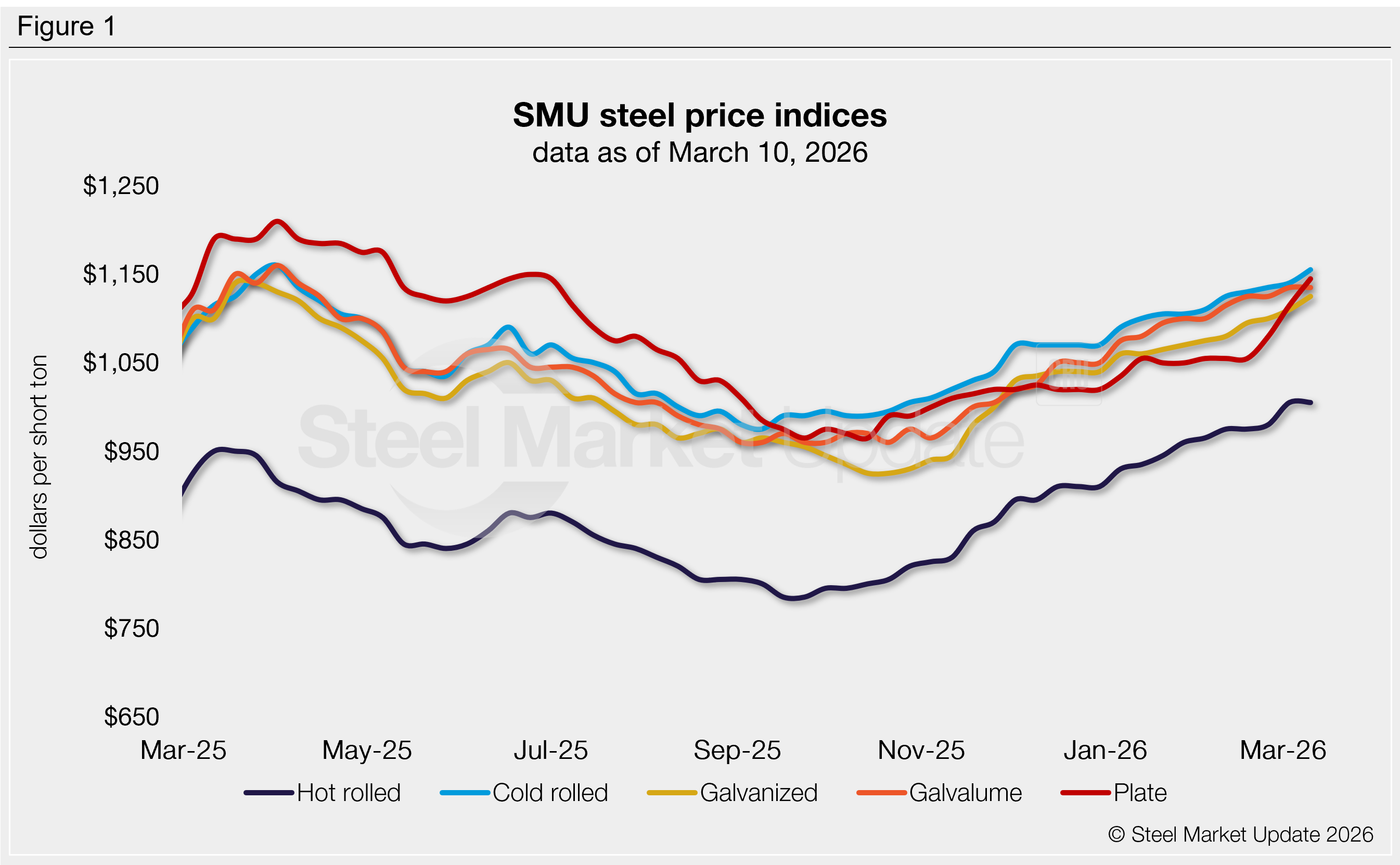

CR and galv prices are their highest point since April 1, 2025 – when the market peaked last year before a wave of uncertainty following “Liberation Day” on April 2 sent tags lower, according to SMU’s pricing archives.

HR, meanwhile, stands at its highest point since mid-January 2024. In other words, HR is higher now than it was following the tariff frenzy that characterized most of Q1’25.

Mills still have the pricing power

Scrap prices might have settled sideways in March, with April looking potentially even weaker. And market participants said imports could become a bigger factor in late spring/early summer.

But neither potentially lower raw material costs nor possibly increased import competition appears to be impacting the market now. Case in point: only 13% of steel buyer respondents in SMU’s last survey said mills were willing to negotiate lower HR prices.

SMU’s price momentum indicator remains at higher for both sheet and plate products, signaling that we expect prices to increase further in the short term.

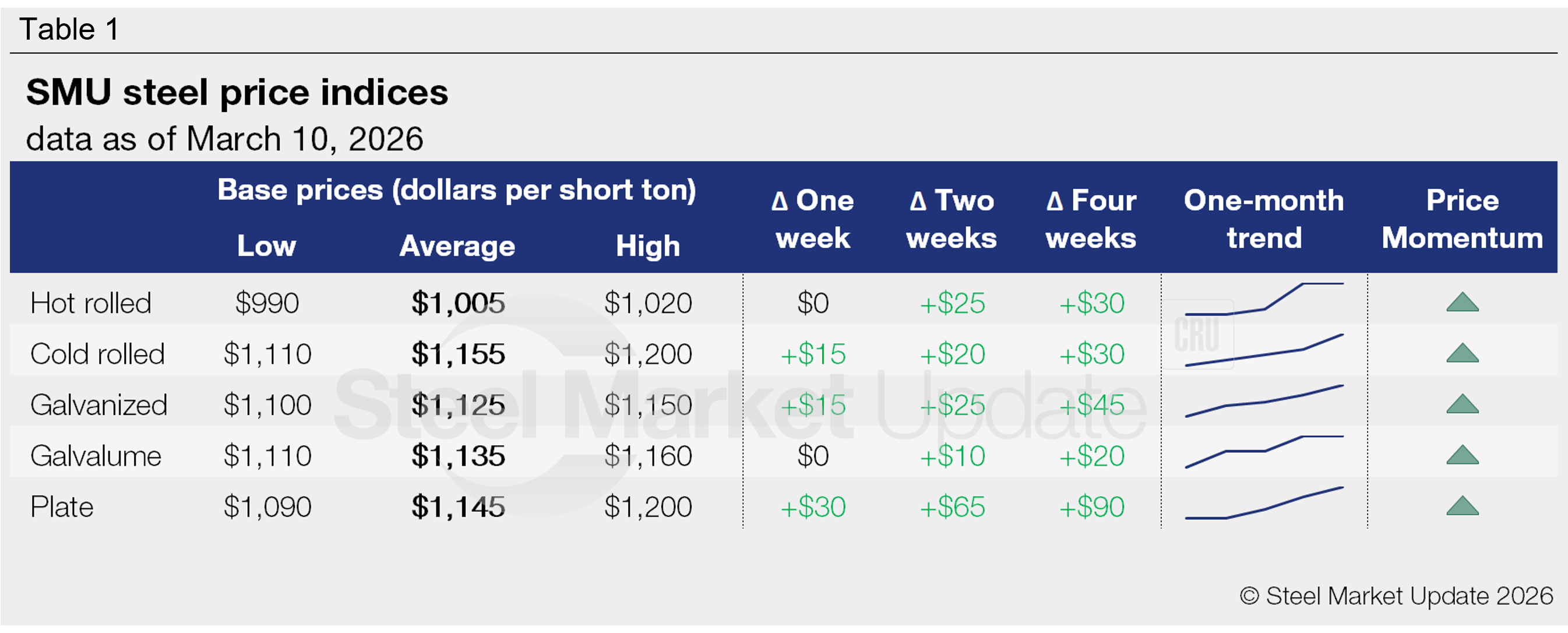

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

HR coil: $990–1,020/st, averaging $1,005/st

Our entire range is unchanged w/w.

Hot-rolled lead times range from 4–9 weeks, averaging 5.9 weeks as of our March 4 market survey.

CR coil: $1,110–1,200/st, averaging $1,155/st

The lower end of our range is unchanged w/w, while the top end is up $30/st. Our overall average is up $15/st w/w.

Cold-rolled lead times range from 5–10 weeks, averaging 7.8 weeks through our latest survey.

Galvanized coil: $1,100–1,150/st, averaging $1,125/st

The lower end of our range is up $30/st w/w, while the top end is unchanged. Our overall average is up $15/st w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,190–1,240/st, averaging $1,215/st FOB mill, east of the Rockies.

Galvanized lead times range from 6–10 weeks, averaging 7.4 weeks through our latest survey.

Galvalume coil: $1,110–1,160/st, averaging $1,135/st

Our entire range is unchanged w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU price range is $1,539–1,589/st, averaging $1,564/st FOB mill, east of the Rockies.

Galvalume lead times range from 5–10 weeks, averaging 8.2 weeks through our latest survey.

Plate: $1,090–1,200/st, averaging $1,145/st

The lower end of our range is unchanged w/w, while the top end is up $60/st. Our overall average is up $30/st w/w.

Plate lead times range from 5–8 weeks, averaging 6.4 weeks through our latest survey.

Brett Linton

Read more from Brett Linton