Analysis

March 12, 2026

HRC vs. prime scrap spread widens further in March

Written by Ethan Bernard

The spread between domestic hot-rolled coil and prime scrap prices widened in March, marking a six-month trend.

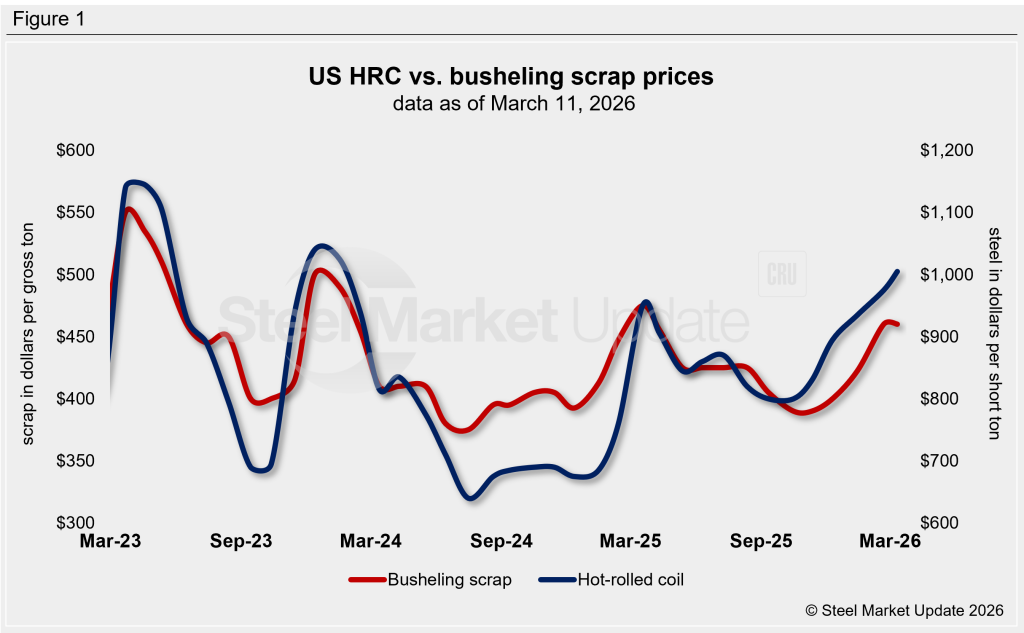

SMU’s average HRC price was $1,005 per short ton (st), FOB mill, east of the Rockies, as of Tuesday, March 10. That’s unchanged from the previous week but up $30/st from a month earlier.

Busheling tags were flat in March at an average of $460 per gross ton (gt).

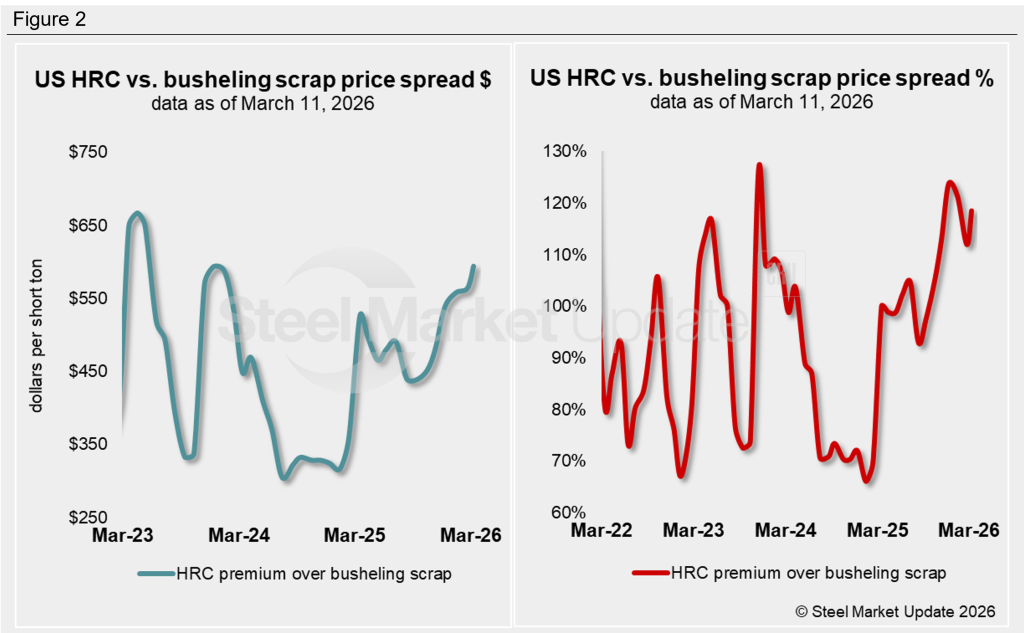

Figure 1 shows price histories for each product.

After converting scrap prices to dollars per short ton for an equal comparison, the differential between HRC and busheling scrap prices was $594/st as of Wednesday, March 11. That’s an increase of $30/st from a month earlier. The last time it touched this mark was December 2023 (Figure 2).

What’s going on?

This month, we saw an increase in the HRC price assessment, but the price of #1 busheling remained static. Therefore, the spread naturally widened. What can we expect in the month ahead?

The general feeling regarding ferrous scrap is supply will increase after a rough winter, and prices, overall, will fall in April. According to SMU’s steel survey, mills are quite reluctant to bargain on the price of HRC. If this is true, the spread is likely to increase, with HRC static or higher while scrap seasonally declines.

The supply of busheling and prime grades, in general, may not drop as much as shredded and HMS, and this may limit the widening of the spread. However, most players are expecting a decline of some amount.

HRC premium as a percentage

The graph on the right-hand side of Figure 2 shows the spread relationship differently: We have graphed HRC’s premium over busheling scrap as a percentage. HRC prices now hold a 118% premium over prime scrap, up from 112% a month earlier.