Analysis

March 24, 2026

Final Thoughts

Written by Michael Cowden

Sheet prices continue to inch higher. And people who once thought hot-rolled coil (HR) couldn’t go above $1,000 are now saying $1,100 doesn’t seem out of the question.

That probably shouldn’t come as a surprise. As we reported last week, lead times continue to extend, domestic mills still have the pricing power, and (as our premium subscribers already know) service center inventories continue to move lower. (If you’re interested in upgrading from executive to premium, let us know at smu@crugroup.com.)

Inventories decline as imports remain at historic lows

Fun fact: Service center inventories had 52.2 days of supply of sheet in February. That’s tied for lowest February total we’ve seen since February 2023.

If you want to find a February with a lower total, you have to go back to February 2021 (42.7 days of supply) – at that time a frenzy erupted when a combination of low inventories, extending lead times, and massive winter storm sent prices skyrocketing.

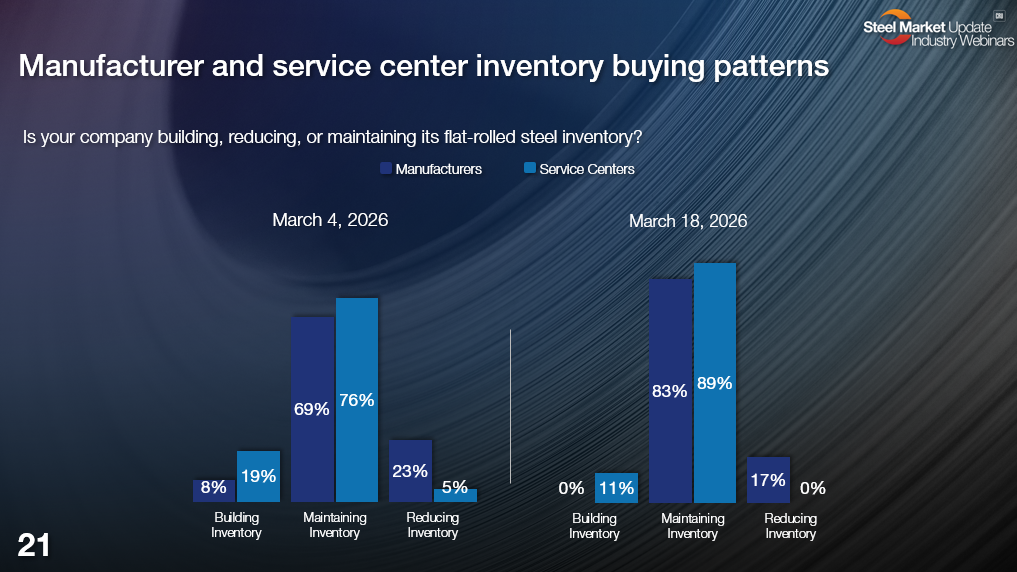

We’ll release March inventory data in mid-April. But we already have some idea of how companies are managing inventories from our last steel market survey. (Editor’s note: The page numbers below refer to where in our full survey deck SMU premium subscribers can find these results.)

In short, almost no one is building inventory. And that’s despite there being some largish holes in stocks. So I wouldn’t be surprised if we find inventories flat or lower again next month.

Meanwhile, as we’ve also reported in recent issues, imports remain historically low. When it comes to overall steel imports, we’re seeing some of the lowest numbers we’ve seen since 2020. And for some products – galvanized, for example – we haven’t seen import volumes as low as what we saw in February in about 15 years.

Availability is a growing concern

An increasing number of you tell me availability is at least as much of a concern as price – especially now that we’re officially in outage season. Can you get your contracted tons? Probably. Can you get 100% of your contracted maximum? Maybe. Can you get spot tons? Maybe not.

Also, as I’ve noted before, certain mills appear to be having trouble keeping up with the orders they’ve got, let alone new business. This message sent by Cleveland-Cliffs to some of its customers last week might be a case in point: “Cliffs is still not yet open for HR May orders. We are anticipating opening HR May desired orders 3/30/26. Cliff’s current situation is once we open May HR, those orders will most likely be confirmed for June delivery.”

We’ve also been getting some questions about when exactly in Q2 U.S. Steel might restart the ‘B’ furnace at Granite City near St. Louis. (We don’t know.) And whether Cliffs might consider restarting a furnace – perhaps at its Dearborn Works near Detroit. (We’re not aware of any imminent plans to do so.)

In theory, such restarts could alleviate the supply squeeze the market has been experiencing. In practice, it’s hard to see that happening soon.

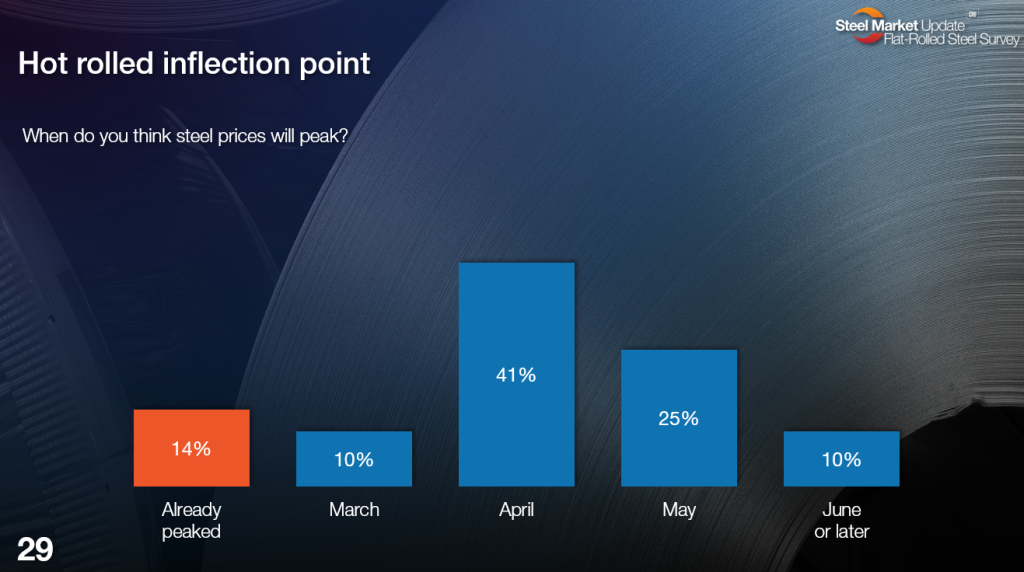

Stronger for longer

Meanwhile, the stronger for longer consensus continues to grow. Most people we survey now tell us they expect sheet prices to peak in April or May.

In a sense, we’ve been kicking the can on when we think prices will peak from one month to the next.

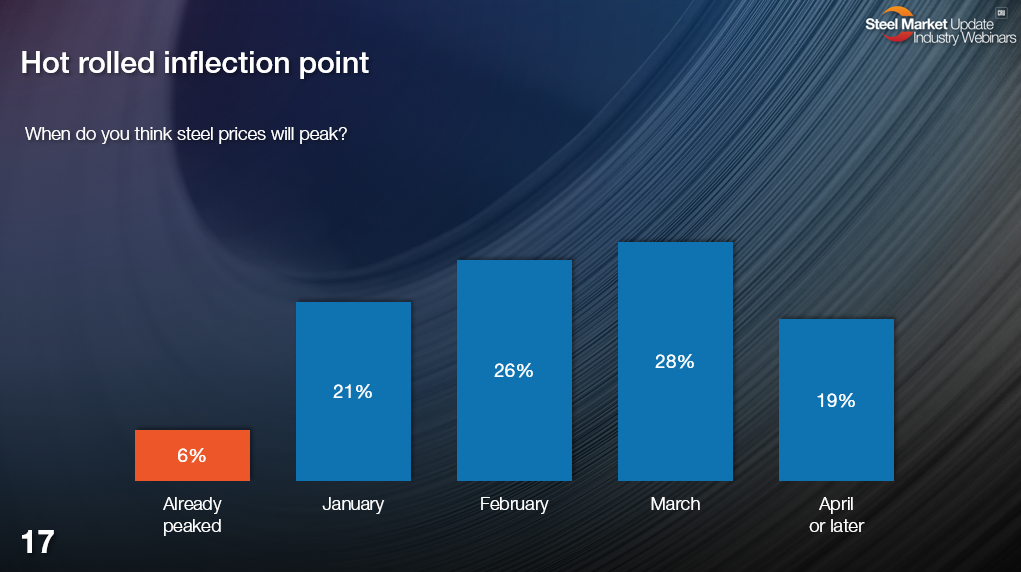

Here is the answer to that same question when we asked it of people in our first survey of 2026 – so back in early January.

Not many expected prices to keep rising into Q2. But that didn’t stop prices from doing just that.

Freight costs up

Some of the smart 19% who predicted prices would continue to rise into spring/summer made import buys early in Q1. But there are some questions now about when those orders will arrive.

Maybe an order scheduled to land in May will slip into June or July. Why? There are the headline-grabbing (and rightfully so) headlines about the Iran War and the bottleneck that is the Strait of Hormuz. Another bottleneck – as our sister publication Aluminum Market Update (AMU) has reported – is delays on the Panama Canal stemming from a drought. (Ping us at amu@crugroup.com if you’d like to subscribe to or take a free trial of AMU.)

And then there is the matter of vessel availability and how to divvy up higher freight costs. It’s probably a straightforward enough matter if a company can fill an entire vessel. That’s not uncommon for, say, Brazilian slabs, Turkish rebar, or a boat loaded with a mix of South Korean products. The freight is higher. But otherwise, it’s relatively straightforward.

Still, let’s say a vessel is filled with multiple smaller orders from multiple suppliers across several countries. Or maybe you’re shipping via container. Our understanding is those situations are where things get complicated. How do higher freight costs get distributed among several parties on a per-ton basis? One industry source described it as “the Wild West.” Maybe an offer is pulled or postponed. Or maybe the price changes over the course of negotiations to account not only for higher freight and fuel costs but for higher insurance rates as well.

To be clear, this isn’t like aluminum, where some of the world’s largest smelters in the Middle East have been impacted. But that’s not to say there is no impact from the Iran conflict on steel. Certain light-gauge galvanized suppliers, for example, are in the region and could face disruption form the conflict, we’re told.

In energy, the US is of course the world’s largest oil producer and so is insulated from the impact of the Iran War. But it’s a global market. And with oil prices going up, so are prices for gasoline and diesel. The result: freight and fuel surcharges are up (or soon will be). Doesn’t matter whether it’s train or truck, it’s going to cost more.

2H uncertainty up too

So, it’s pretty clear prices will continue to move higher in the near term. That’s why our momentum indicators continue to point upward.

But what happens as we get into the summer and fall? There seems to be a little more uncertainty about the longer term than usual based on our channel checks this week.

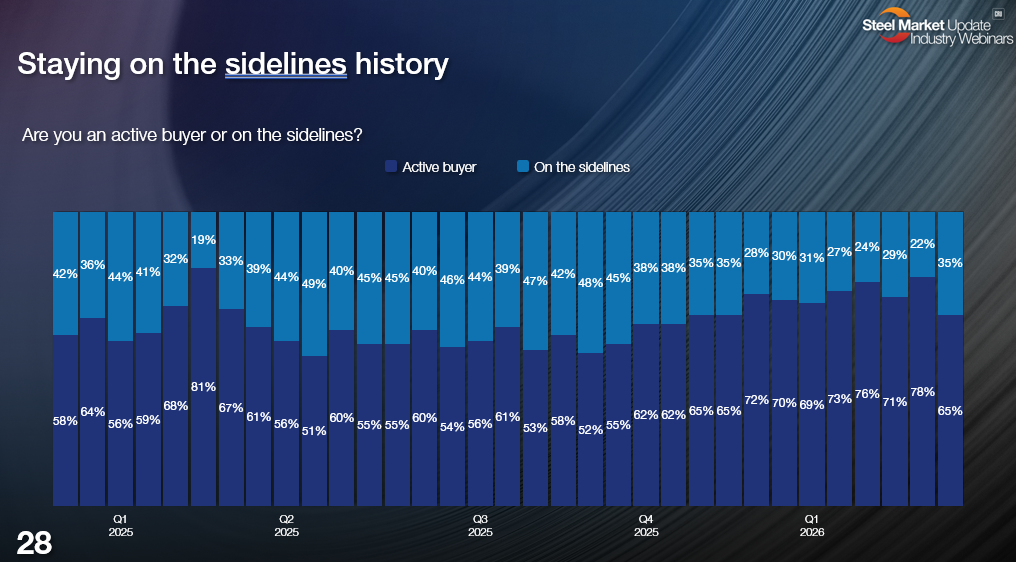

Maybe the uncertainty explains why we saw fewer people describe themselves as active buyers in our last survey:

Rewind to the beginning of the month, and nearly 80% of respondents said they were active buyers. But more recently, that number has dropped to 65%.

Perhaps it’s just noise in the data. I tend to watch the long-term trend lines. And I try not to read too much into any given survey result. That said, I can see why there might be a little more hesitation now than in prior weeks.

Some of it is just seasonal. We tend to see prices dip as we get past spring outages and as lead times get into the summer months, when automakers take their outages. And mills will eventually catch up on orders.

Sure, both the floor and the ceiling for sheet prices seem to be moving higher from one year to the next when it comes to sheet prices. But do you want to be the person who bought HR at $1,100 when the market dips below $1,000?

Then there is the uncertainty around the Iran war. How long will it last? How high might oil prices go? The war hasn’t had the immediate impact on the US market that confusion surrounding President Trump’s “Liberation Day” tariffs did last April.

But ask anyone what they think the market will look like in Q3 and they turn philosophical. At what price does oil start to create demand destruction? What is the playbook for a widening conflict, if that’s what happens? There are no easy answers to those. Or at least none that I’m aware of.

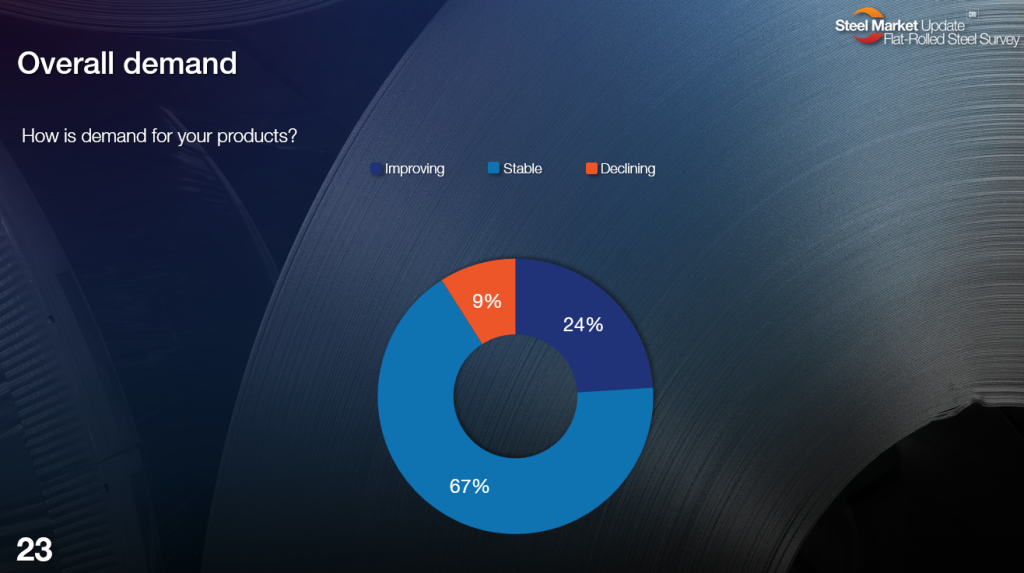

The good news? Most people in our last survey continued to report demand as stable or improving:

And if we’ve got a sauce of decent demand, maybe it’s enough to make all the geopolitical uncertainty at least palatable for the domestic steel market. (Pardon the food metaphor, it’s getting late – and I’m getting hangry.)

SMU Steel 101

We had a great SMU Steel 101 last week in Monterrey, Mexico. It was our first event in Mexico, and we don’t think it will be our last!

A shoutout to my colleagues, our instructors, and everyone who attended for making it a success. Also, thank you to Ternium for letting us tour their Pesquería complex, one of the most modern hot strip mills in North America – and what will soon be one of the newest (and biggest) EAFs as well.

Our next Steel 101 will be on May 19-20 in Corpus Christi, Texas, and will feature a tour of SDI Sinton – another cool, new North American EAF sheet mill. You can find out more and register here.