Market Data

March 31, 2026

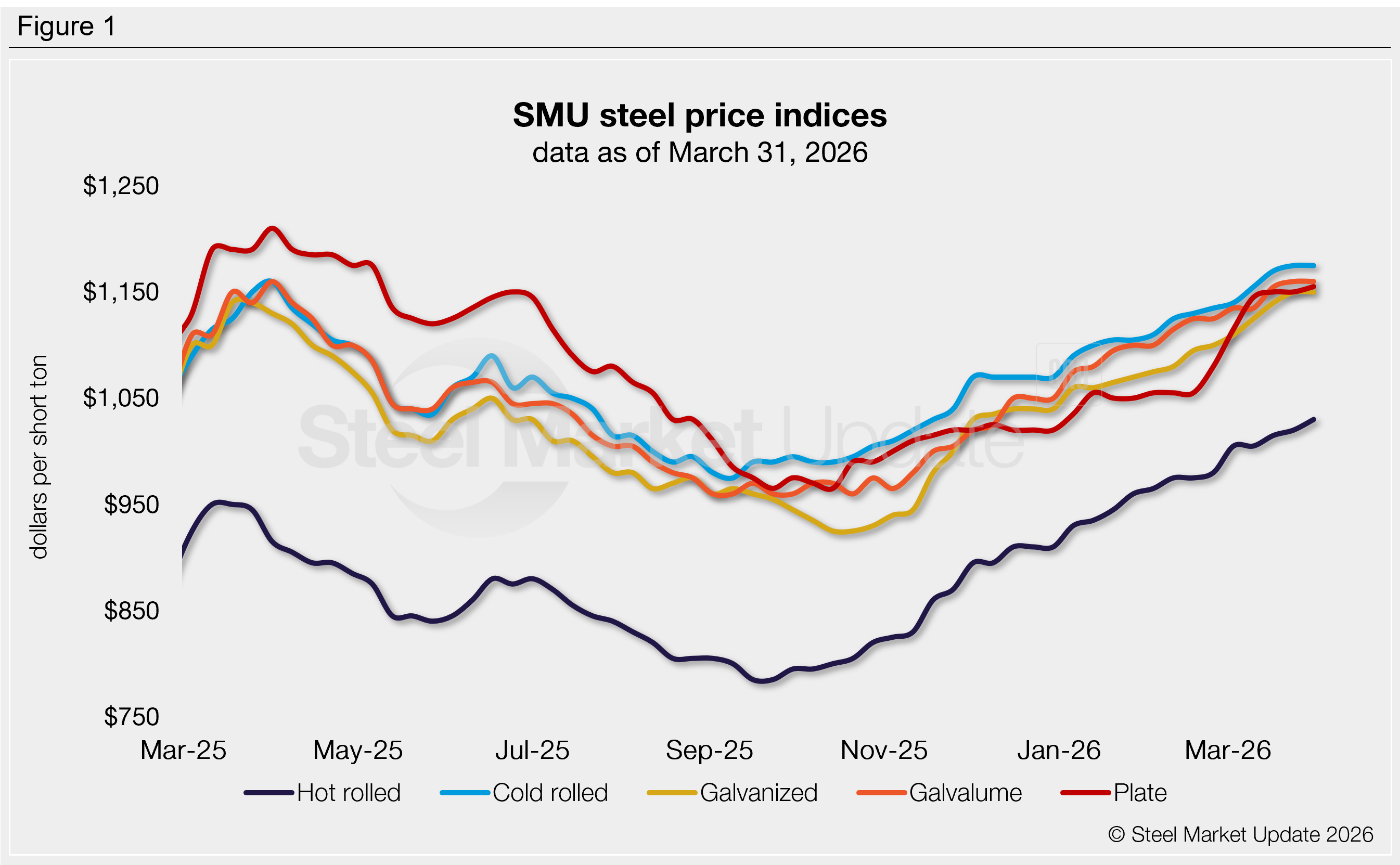

SMU Price Ranges: Sheet and plate prices flat or up (again) – for how long?

Written by Brett Linton & Michael Cowden

Sheet and plate prices were flat or modestly higher this week, continuing a trend we’ve seen since the beginning of Q4.

A slow, six-month pricing upcycle is something of an anomaly in a US steel market that has been characterized by price spikes following market shocks and then protracted downturns.

Some market participants said domestic mills had managed the current pricing cycle well, perhaps in an effort to avoid such spikes, which have in past cycles invited an influx of imports.

Few questioned the overall direction of the market. But while some sources said solid demand merited continued prices gains, others said it remained mostly a story of limited supply.

Opinions were mixed on the outlook for supply. Some market participants said domestic mills were beginning to catch up on late orders and supply shouldn’t be as tight as it’s been going forward. But others said outages and delayed ramps at certain facilities could keep supplies tight for longer than expected.

Several sources expressed concern about the Iran war and what might happen if higher fuel prices, for example, translated into broader inflation. But most said they had seen no impact or only a limited impact from the conflict in the Middle East to date.

SMU’s price momentum indicators remain at higher for both sheet and plate products, signaling we expect prices to increase further in the short term.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $1,000–1,060/st, averaging $1,030/st

The lower end of our range is unchanged week over week (w/w), while the top end is up $20/st. Our overall average is up $10/st w/w.

Hot-rolled lead times range from 4–8 weeks, averaging 6.4 weeks as of our March 18 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil: $1,150–1,200/st, averaging $1,175/st

Our range was unchanged w/w.

Cold-rolled lead times range from 6–10 weeks, averaging 8.2 weeks through our latest survey.

Galvanized coil: $1,100–1,200/st, averaging $1,150/st

The lower end of our range is down $20/st w/w, while the top end is up $20/st. Our overall average is unchanged w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,190–1,290/st, averaging $1,240/st FOB mill, east of the Rockies.

Galvanized lead times range from 6–10 weeks, averaging 8.0 weeks through our latest survey.

Galvalume coil: $1,120–1,200/st, averaging $1,160/st

Our range was unchanged w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU’s price range is $1,549–1,629/st, averaging $1,589/st FOB mill, east of the Rockies.

Galvalume lead times range from 6–10 weeks, averaging 8.4 weeks through our latest survey.

Plate: $1,130–1,180/st, averaging $1,155/st

The lower end of our range is up $30/st w/w, while the top end is down $20/st. Our overall average is up $5/st w/w.

Plate lead times range from 6–9 weeks, averaging 7.0 weeks through our latest survey.

Brett Linton

Read more from Brett Linton