Market Data

May 28, 2026

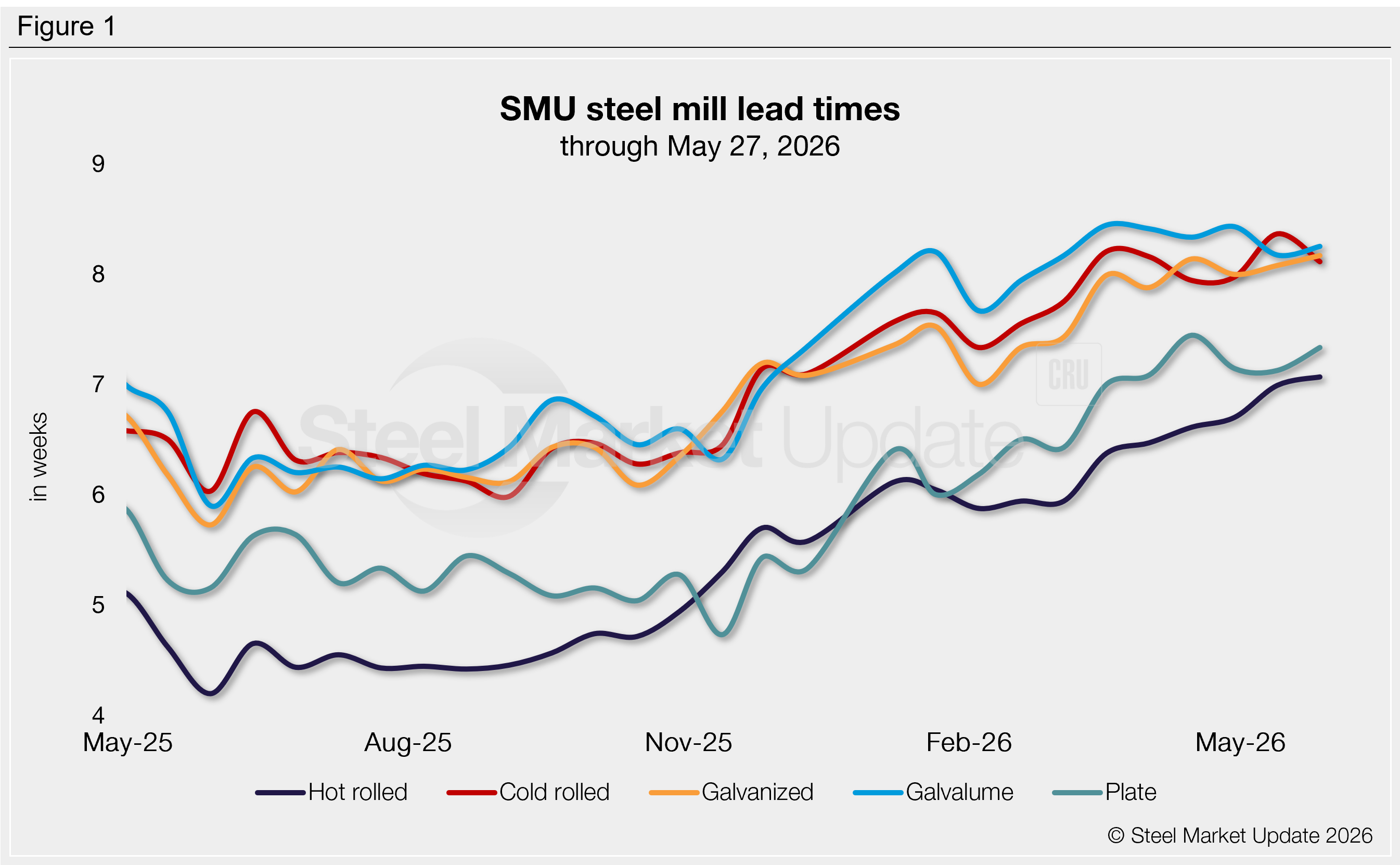

SMU Survey: Sheet and plate lead times hold at extended levels

Written by Brett Linton

Steel mill lead times are holding at or near multi-year highs on sheet and plate products, according to buyers responding to our latest market survey. Production times began extending late last year, with all products reaching multi-year highs in May. Current lead times are between two to three weeks longer than those seen this time last year.

- The average production time for hot-rolled coil is just over seven weeks, the highest recorded since October 2021.

- Cold rolled eased to just over eight weeks, holding near a two-year high.

- Coated products remain at just over eight weeks, both at some of the highest levels seen in over two years.

- Plate rose to just under seven and a half weeks, marginally below the four-year high seen in April.

Table 1 summarizes current lead times and recent changes by product (click to expand)

Compared to our mid-May analysis, three of our lead-time ranges shifted this week:

- The longest hot rolled lead time we considered decreased from 11 weeks to 10.

- The longest Galvalume lead time decreased from 12 weeks to 10.

- The shortest plate lead time considered increased from five weeks to six, and the longest increased from eight weeks to nine.

Buyers continue to predict stability

Roughly half of responding buyers (53%) predicted lead times will be flat two months from now, down slightly from our previous survey. The rest were split, with 27% expecting lead times to extend further and 20% foreseeing contractions. Comments included:

“Flat – mills will do their best to hold the ‘demand & lead-times’. However, I do believe automotive softness will eventually impact the mills’ ability to hold pricing and lead times.”

“Flat – demand is stable, but instability in the broader market may reduce demand.”

“Extending – domestic mills will remain tight for the foreseeable future. At least through the summer and into the third quarter or longer.”

“Extending – between maintenance and full order books, there is no reason to believe otherwise.”

“Contracting – in two months, the air will be out of this market and lead times will be falling back. Thank goodness!”

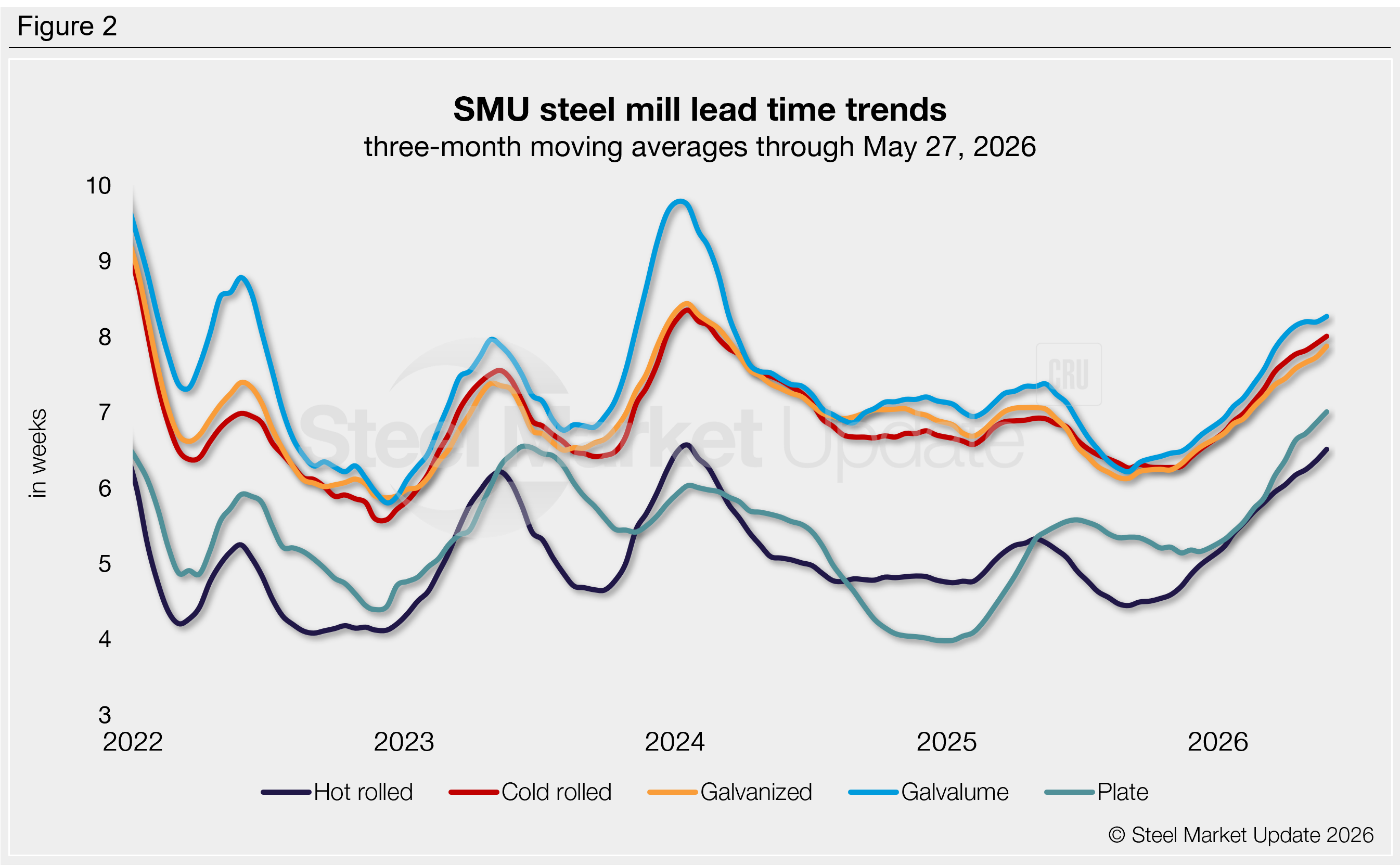

Trends

To better highlight trends, lead times can be calculated on a three-month moving average (3MMA) basis. All five of our sheet and plate 3MMAs extended further this week, as they have since late 2025 (Figure 2).

Sheet 3MMA lead times are almost two weeks longer than the two-year lows seen last September and roughly a week longer than they were this time last year. Our latest plate 3MMA is nearly two weeks longer than it was both six months and one year ago.

Average lead times by product across the past three months were: hot rolled at 6.5 weeks, cold rolled at 8.0 weeks, galvanized at 7.9 weeks, Galvalume at 8.3 weeks, and plate at 7.0 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Consult your mill rep for actual lead times. Premium members can view an interactive history of our steel mill lead times data on our website. If you’d like to participate in our surveys, contact smu@crugroup.com.