Analysis

June 4, 2026

Final Thoughts: SMU's June scrap survey

Written by Ethan Bernard

The June scrap market is still shaping up, and SMU’s scrap survey has arrived just in time to give you a glimpse of how respondents are viewing the market. We’ll give you a sneak peek at what they were seeing ahead of the June settle regarding pricing, demand, and the perennial questions around Trump and tariffs.

SMU’s Stephen Miller has written that the June market looks sideways so far, mostly in line with previous expectations.

That also matches what the vast majority of our survey respondents anticipated. In this month’s survey, 71% thought June tags on prime scrap would be flat, 24% expected they would be up, and the remaining 5% believed prices would go down.

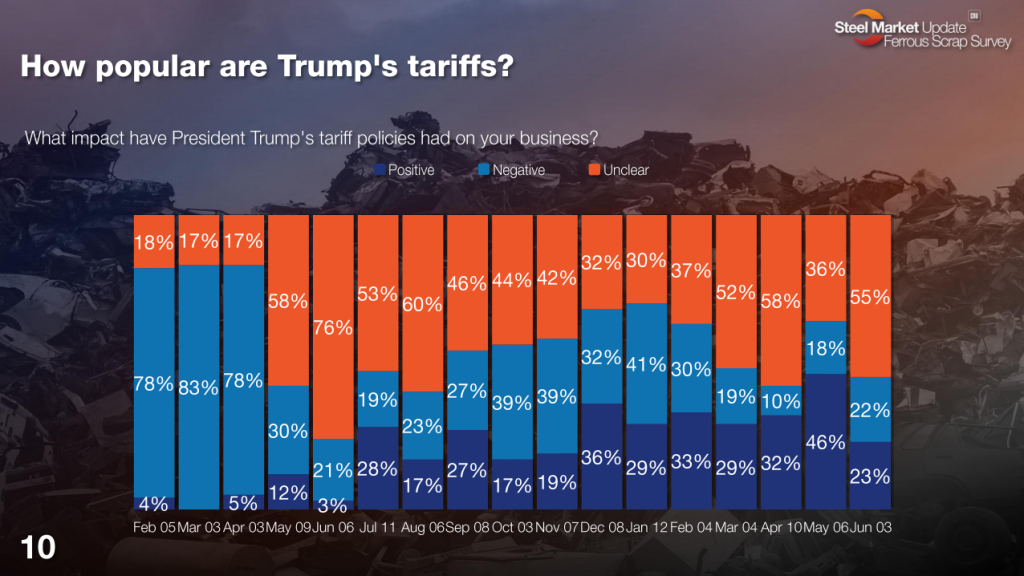

On the tariff front, one thing that has really changed since our previous survey two weeks earlier is the view on President Trump’s tariff regime.

We now see that 55% of survey respondents view the impact of the tariffs as unclear vs. 36% previously. Also of note, only 23% see the tariffs as having a negative impact on their business in this survey, down from 46%.

There has been a lot of action on the tariff front lately. Here is a quick sampling. Yesterday, SMU’s Laura Miller wrote about steel and aluminum being excluded from additional Section 301 tariffs (at least for now) because they are already subject to Section 232 duties.

A day earlier, she also wrote on the White House lowering S232 duties on ag and HVAC equipment.

And, personally, I wrote my last Final Thoughts on the USMCA review set to start in July, current meetings between the US and Mexico, as well as the situation with Canada.

Could so much tariff activity be causing more uncertainty in the market?

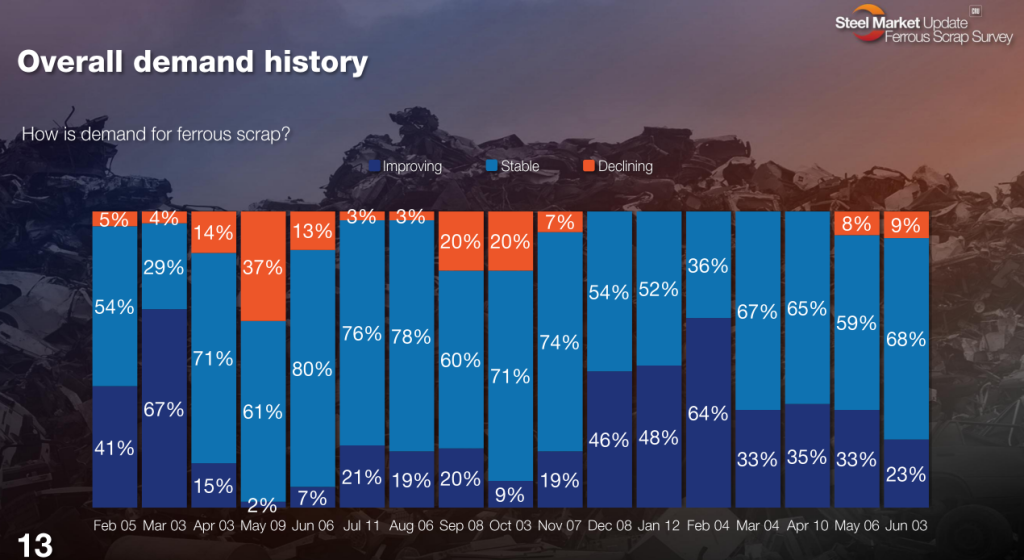

Another interesting data point comes from our question on ferrous scrap demand. The percentage of respondents saying demand was stable jumped to 68% vs. 59% previously. But this came at the expense of respondents reporting demand was improving, which fell to 23% from 33%.

And that’s just start of interesting data points the survey contains. (Full results are available to all premium members.)

So, while the full survey results come out on Friday, below is a preview – one that includes comments from respondents. See if their insights match yours. They just might provide you with a new perspective.

Want to share your thoughts? Contact david.schollaert@crugroup.com to be included in future market questionnaires.

What impact have President Trump’s tariff policies had on your business?

Here, a couple of participants noted the tariffs’ influence on pricing: “Artificially high steel prices” and “tariffs have pushed costing and pricing up.”

How is demand for ferrous scrap?

“Obsolete soft, prime firm.”

“The steel industry is doing well, and exports to Turkey are draining scrap from East Coast.”

“HRC has made the difference.”

Where do you think busheling prices will be in June?

“There is some pressure to push it down, but I don’t think it will happen.”

“Demand is stable and starting to be reduced due to the automotive slowdown.”

“Strength in prime scrap.”

“Demand is starting to slow vs. the amount of scrap inventory.”

Where do you think shred prices will be in June?

“Depends on the region. Some sideways and some areas down ( Pa./ Ohio / Mich. ).”

“Sideways pricing expected.”

“Pricing for lesser quality is weaker.”

Where do you think HMS prices will be in June?

“Should be flat.”

“Sideways pricing expected.”

“Plenty of supply, and it is an ignored domestic grade by flat roll mills.”

“Demand is slowing.”