Final Thoughts

The US scrap market finds itself in a familiar position as we progress into the final quarter of the year.

The US scrap market finds itself in a familiar position as we progress into the final quarter of the year.

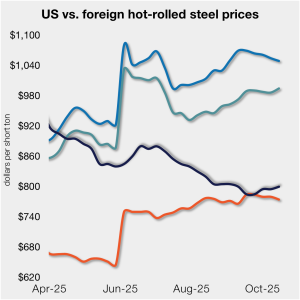

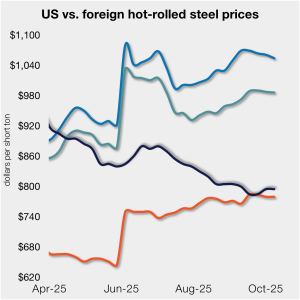

SMU’s average price for domestic hot-rolled (HR) coil was $800 per short ton (st) this week, up $5/st week on week (w/w). In offshore markets last week, prices were varied.

US scrap prices fell on busheling and shredded in October, while HMS remained flat, market sources told SMU.

Participants in the domestic plate market say spot prices appear to have hit the floor, and they continue to linger there. They say demand for steel remains thin, with plate products no exception.

Steel mill lead times ticked lower across most sheet and plate products this week, according to responses from SMU’s latest market check.

Mills are more willing to negotiate spot prices for both sheet and plate products, according to our latest market survey results.

September service center shipments and inventories report for sheet and plate

Musings on decarb, tariffs, and technology, and where it might be leading.

SMU’s HR price stands at $800/st on average, up $5/st from last week. The modest gain came as the low end of our range firmed, and despite the high end of our range declining slightly.

The World Steel Association (worldsteel) Short Range Outlook for global steel demand predicts that 2025’s steel demand will clock in at the same level as in 2024. In its October report, the Brussels-based association stated that this year’s steel demand will reach ~1,750 million metric tons (mt). The organization forecasts a 1.3% demand rebound in 2026, pushing […]

SMU has successfully completed an external review of all our prices. The review has concluded that they algin with principles set by the International Organization of Securities Commissions (IOSCO).

Nucor has left its consumer spot price for hot-rolled coil at $875 per short ton for the eighth straight week.

There are days when this feels like a “nothing ever happens” market. Don’t get me wrong. Plenty is happening in the world. It’s just that none of it seems to matter when it comes to sheet and plate prices.

More liberal access to the Northwest Passage could play into trade negotiations between Canada and the United States.

The boom in China’s direct steel exports has not stopped this year, even with a rise in protectionist measures globally. The increase is driven by...

Iron ore shipments from US Great Lakes ports fell sharply in September, per the latest from the Lake Carriers’ Association (LCA) of Westlake, Ohio.

Although total HVAC shipments fell in August, YTD volumes remain relatively strong. Nearly 15 million units were produced in the first eight months of the year, the fourth-highest rate in our 19-year data history.

Some sources also speculated that plate could see further price increases thanks to modest but steady demand, lower imports, mill maintenance outages, and end markets less immediately affected by tariff-related disruptions.

SMU’s average price for domestic hot-rolled (HR) coil was $795 per short ton (st) this week, sideways week on week (w/w). The move was different in offshore markets last week, as prices eased marginally.

Usually, I write about steel in this column because, well, we’re Steel Market Update. But before I get to steel, I want to give a shoutout to my colleagues at Aluminum Market Update (AMU) – SMU’s new sister publication.

Tariffs are ultimately to blame for stagnant demand in the hot-rolled coil market, domestic market sources tell SMU.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

Most mills sought a drop of $20-40 per gross ton (gt) in busheling prices and a $20/gt dip for shredded and HMS. Despite efforts to buy cheaper, the busheling price settled at down only $20/gt.

The European Commission proposes cutting its steel import quota by almost half, with volumes exceeding the limit facing 50% duties. The region’s steel industry welcomes the move, while other steel-producing nations fear the consequences. CRU published an insight before this announcement, noting that more restrictive trade policy could significantly raise the cost of marginal supply […]

If I could change something, it’d be this: Political news would get more boring. And news about steel prices and steel demand would get a little more exciting.

SMU’s sheet and plate prices see-sawed this week as hot-rolled (HR) coil prices held their ground while prices for galvanized product slipped.

Nucor is keeping hot-rolled (HR) coil prices unchanged again this week, according to its latest consumer spot price (CSP) notice issued on Monday, Oct. 6

SMU’s latest survey results indicate that steel market participants think sheet prices are at or near a bottom. But most also think there is limited upside once they inflect higher.

SMU’s Current Sentiment Index for scrap decreased this month, a move mirrored by our Future Sentiment Index, according to the latest data from our ferrous scrap survey.

Let’s take a quick tour of some key stories from SMU in the week of Sept. 29 - Oct. 3.