Final Thoughts

To say we’ve entered a “Brave New World” since Jan. 20 might be an exaggeration, but we’ve definitely entered a different one.

To say we’ve entered a “Brave New World” since Jan. 20 might be an exaggeration, but we’ve definitely entered a different one.

I think it’s fair to say that the last few weeks – and last week especially – have been among the most intense for any of us covering steel (or aluminum).

With a chronic trade deficit, the administration will continue to cite more tariffs as necessary. This is in error, as noted above. Yet the base of President Trump’s support does not see it that way. More tariffs are possible. But the only way to reduce the US trade deficit substantially is to close the gap between savings and investment in the United States.

A look at how SMU survey respondents are reacting to President Trump's recent actions on tariffs.

Automakers, construction, manufacturers raise concerns

Unions members on both sides of the US-Canada border are speaking out against President Trump’s tariffs on Canadian steel. They say the tariffs threaten to disrupt supply chains and subvert decades of economic cooperation. The United Steelworkers (USW) has more than 850,000 total members in North America, with 225,000 in Canada.

The problem is that the situation in Washington is so fluid that no one really knows what to expect

The ferrous scrap market in the US and Canada is trying to find its way through difficulties that could well determine its direction over the next several months.

While American steelmakers welcome the revival of the Section 232 tariffs on steel and aluminum imports, other nations' steel industries are calling for retaliation against President Trump's unilateral action of upping the levies on trading allies and removing all product exemptions.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

US steel prices set to jump after President Trump levies new tariffs.

A lot of the changes basically entail rolling back what I’ll call, for fun, Section 232 Lite. S232 Lite resulted from watering down what I’ll call OG S232 – the one first imposed in March 2018 - with exemptions and exclusions over the years. Now, OG Section 232, is back with its across-the-board 25% tariffs against everyone.

The February scrap market has settled higher on all grades SMU covers.

The new version of Section 232 goes into effect on 12:01 am ET on March 12, according to the executive order. The latest iteration of Section 232 removed quotas, exemptions, and other carve outs that had accumulated over years.

December 2024 marks the fourth month in a row that steel exports have declined, now at the lowest monthly rate recorded since December 2022.

President Donald Trump said he would announce 25% tariffs on all steel and aluminum imported to the US, according to Bloomberg. Trump said he would make an announcement about the matter on Monday. It was not clear when the tariffs might take effect.

An exciting first look at the results from SMU's first scrap survey.

Following the one-year low recorded in November, steel imports rose by 3% in December to 2.14 million short tons (st) according to final US Commerce Department data. January could be the highest month for steel imports witnessed in nearly three years.

The day-to-day bustle of these announcements should not obscure what they signal for other potential tariff measures in the near term and a revamped trade and economic policy in the long term.

If 2021 and 2022 was the party, 2024 is the morning after, one panelist said.

"Personally, I find it very hard to believe that we would be in a trade war with Mexico and Canada for more than a few months at any given time. I don't know how Mexico and Canada could survive that. That's a recession for them. That's a few points off GDP for us - my opinion.”

Facing weak demand and an “unsustainably low” pricing environment, GrafTech International posted another quarterly loss to close out 2024.

As Wolfe Research’s Timna Tanners put it in her opening talk at Tampa on Monday afternoon, we’re living in a world of “Trumplications” now. That probably means – at least in the short term – higher scrap costs, lower imports from countries hit with or threated tariffs, and higher steel prices. SMU data reflects that. Scrap went up in January. More than 75% of the respondents to our more recent survey expect scrap to go up again February, maybe by a lot. Lead times, meanwhile, have been ticking upward this month. It started with hot-rolled coil and plate earlier this month. Now we’re seeing coated lead times extending too.

AM/NS Calvert has begun commissioning its new electric-arc furnace, with plans to reach its full annual run rate of 1.65 million short tons a year from now.

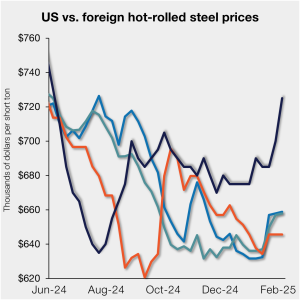

Hot-rolled (HR) coil prices moved up again in the US this week, while tags abroad were largely flat. The result: the margin US hot band holds over imports on a landed basis widened further.

The reprieve for Canadian and Mexican tariffs this week has left some uncertainty for the February scrap market, with some sources pointing towards a $20-per-gross-ton (gt) increase.

While Canada and Mexico bent the knee to push tariff implementation out another month, the US on Tuesday instituted an additional 10% tariff on Chinese goods.

We joked in our last Final Thoughts that Wiley trade attorney Tim Brightbill – one of the nation’s leading experts on trade law and policy – would probably be revising his presentation on Trump, trade policy, and tariffs for the Tampa Steel Conference. He did. And even after those last-minute revisions, he actually got trumped […]

The Commerce Department on Tuesday issued preliminary subsidy rates in the corrosion-resistant steel (CORE) trade case. The agency set minimal countervailing duty (CVD) rates for Brazil and Mexico, mostly high rates for Vietnam, and low rates for Canada, except for one privately held distributor. Commerce assigned that company, Nova Steel, and a handful of Vietnamese […]

Steel and aluminum have been identified as high priorities for trade