Nucor increases HR spot price by $10/ton, again

Nucor increased its weekly hot-rolled coil spot list price by $10 per short ton (st) again on Monday, Dec. 15. This was its eighth increase in as many weeks, moving up $65/st over that span.

Nucor increased its weekly hot-rolled coil spot list price by $10 per short ton (st) again on Monday, Dec. 15. This was its eighth increase in as many weeks, moving up $65/st over that span.

After another eventful week in the steel market comes to a close, one of the most interesting developments has been timing.

Participants in the domestic coil market hope producer price increases indicate strong market conditions entering the new year.

Less than half of the steel buyers who responded to our market survey this week reported that domestic mills are willing to talk price on new spot orders

The pig iron market in Brazil has moved up since our last report for US-bound cargoes.

The price spread between hot-rolled coil and prime scrap has widened for the third consecutive month in December, based on SMU’s most recent pricing data.

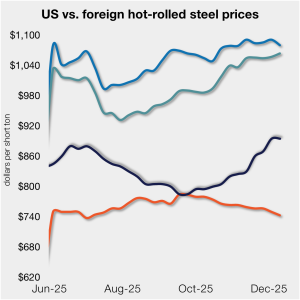

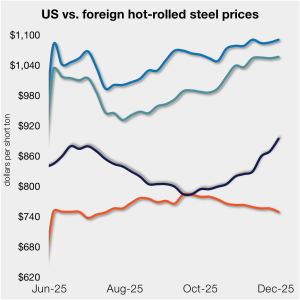

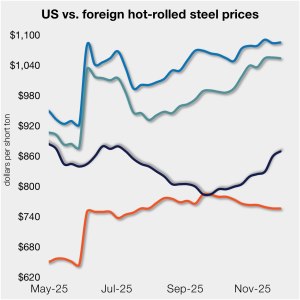

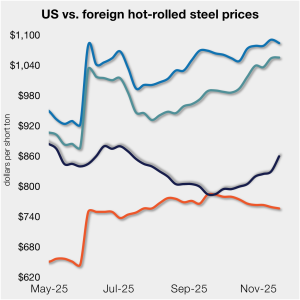

The price gap between stateside hot band and landed offshore product continues to narrow toward parity, now at its lowest level in five months.

Nucor has announced new base prices for galvanized steel products as of Wednesday, Dec. 10.

SMU’s sheet and plate prices took a breather this week, holding relatively steady at multi-month highs.

US ferrous scrap prices have picked up in December, sources told SMU.

Nucor increased its weekly hot-rolled coil spot list price by $10 per short ton (st) on Monday, Dec. 8.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

NLMK has revised their galvanized and galvanneal coating extras effective January 2026.

Sources expect the recent spot market price hikes on domestically produced plate products to be accepted by the market.

The price gap between stateside hot band and landed offshore product has inched closer to parity, now at its lowest level since the summer.

All of SMU’s sheet price indices rose this week, climbing to new multi-month highs. At the same time, our plate index held steady.

Oregon Steel Mills has joined other producers, announcing a price increase of at least $40 per short ton for steel plate.

Nucor increased its weekly hot-rolled coil spot list price by $5 per short ton (st) on Monday, Dec. 1. This was its sixth increase in as many weeks, moving up $45/st over that span.

The price gap between stateside hot band and landed offshore product tightened further this week, as the average price for domestic hot-rolled was $10/st higher w/w.

All five of SMU’s sheet and plate price indices increased this week for the second week in a row, with all products inching up to new multi-month highs. Prices are now up by $30-70/st compared to those seen four weeks ago.

SSAB Americas aims to increase prices on all its products by at least $40 per short ton (st).

Nucor plans to increase prices for steel plate by $30 per short ton (st). The move coincides with Charlotte, N.C.-based steelmaker opening its plate orderbook for January.

Nucor increased its weekly hot-rolled coil spot list price by $5 per short ton (st) on Monday, Nov. 24. This was its fifth increase in as many weeks.

Sources say domestic mill lead times and consumer spot prices have increased this week.

Most steelmaking raw material prices remained stable over the past month. Prices are mixed in comparison to this time last year.

The price gap between stateside hot band and landed offshore product shrank week over week (w/w).

SMU’s price indices increased across the board this week, reaching new multi-month highs.

Nucor has increased its consumer spot price (CSP) for hot-rolled (HR) coil for a fourth consecutive week. Now at $910 per short ton (st), up $15/st from last week.

Global sheet markets face divergent trajectories into year-end, with Asian (excl. India) markets under pressure from oversupply. This, while Western markets experience temporary support from supply constraints.

Contract talks for U.S. value-added aluminum products are reaching a critical stage, with billet, primary foundry alloys, and wire rod upcharges diverging as buyers and producers race to finalized 2026 pricing.